Presented to Parliament pursuant to Section 36 (1) of the Climate Change Act 2008. This report was laid before Parliament on 24 June 2026.

This statutory report provides a comprehensive overview of the UK Government’s progress to date in reducing emissions.

Footnotes have been removed from the online version of this report. Please download the PDF for the footnoted version of this report.

Acknowledgements

The Committee would like to thank:

The team that prepared this report and its analysis. This was led by Emma Pinchbeck, James Richardson, Emily Nurse, Eoin Devane, Esther Harris, and Sam Karslake and included Audra Anderson, Rose Armitage, Owen Bellamy, Rose Bevan-Smith, Ari Biggart, Sandra Bogelein, Marta Calore, Rachel Carr-Whitworth, Jools Clarke, Freddy Curtis, Stephen Dillon, Bianca de Farias Letti, Victoria de la Cruz, Joshua Deru, Caitlin Douglas, Kim Dowsett, Kieron Driscoll, Shane Fernando, Elizabeth Fuller, Jamie Gittings, Ruth Gregg, Rachel Hay, Robbie Herring, Gemma Holmes, Ariana Jessa, Steffi Johns, Luke Jones, Miriam Kennedy, Adam Khan, Grace Macready, Fatima Manji, Luke Maxfield, Moryse McInniss, Aaron McMahon, Matthew Meakins, Richard Millar, Frances Molesworth, Bea Natzler, Sarah Nelson, Amarath Ou, Chris Parker, Emma Patterson, Jessie Peramal, Karina Rodriguez Villafuerte, Simon Rayner, Andrew Romang, Maria Reboredo Prado, Miranda Schroder, Rachel Sewell, Olivia Shears, Blánaid Sheeran, Bryony Sheridan, Thomas Smith, Rachael Steller, James Tarlton, Seán Taylor, Indra Thillainathan, Emma Vause, Sophie Vipond, Scarlett Walker, Eveline White, Hannah Williams, Kirsty Wivell, Louis Worthington, Fergal Wraith.

Our expert advisor, Professor Rebecca Willis.

Executive summary

The UK Government is not moving fast enough to reduce greenhouse gas (GHG) emissions and to protect households and businesses from volatile fossil fuel prices. The war in Iran has led to the second global fossil fuel price shock in just four years. In this uncertain geopolitical context, many countries are responding with plans to provide secure, homegrown energy by rapidly reducing dependency on fossil fuels. To do this in the UK, the Government needs a more ambitious plan to electrify the UK. This requires continued progress towards low-carbon electricity and an accelerated roll-out of electric vehicles (EVs), heat pumps, and industrial electrification.

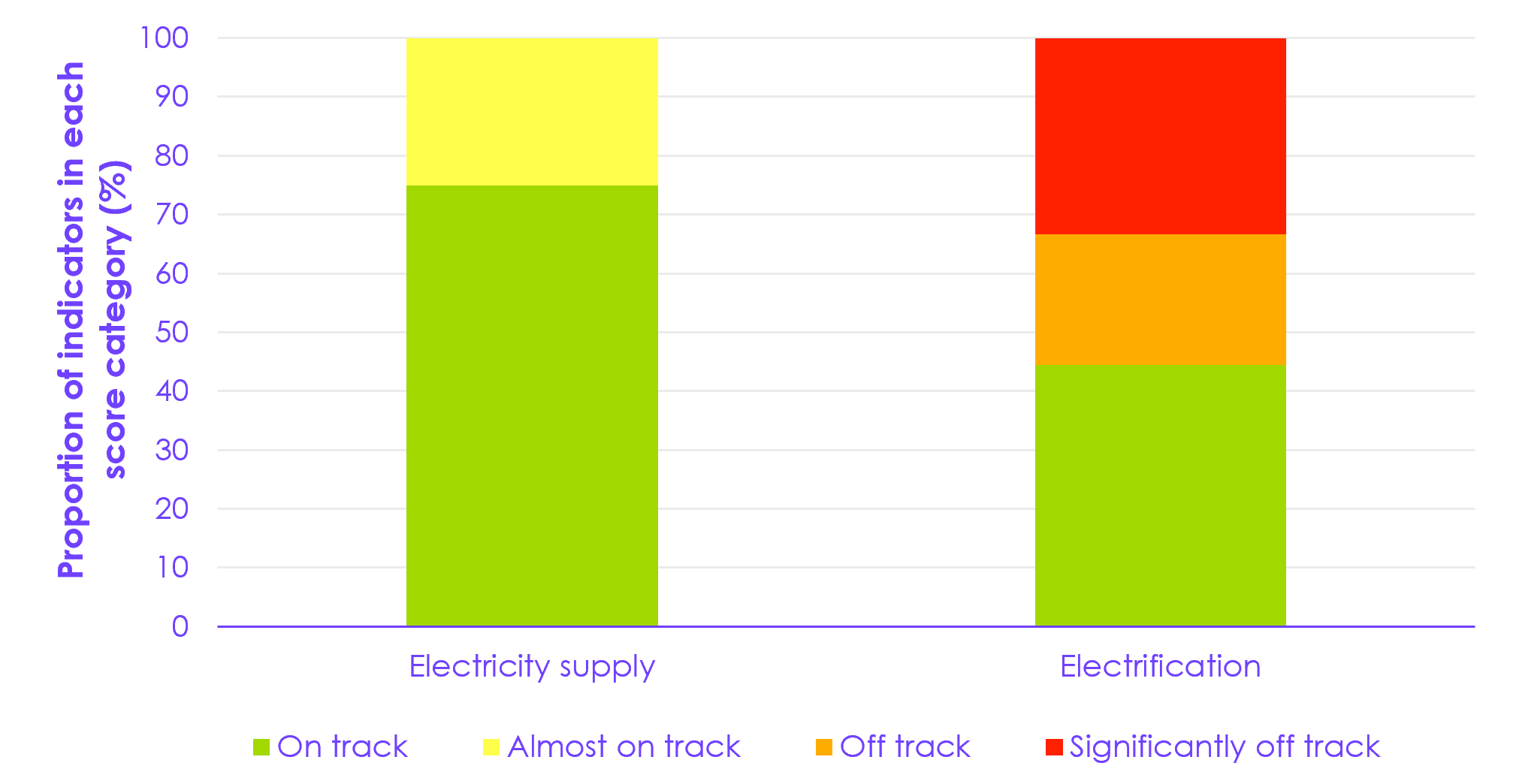

The UK remains among a leading group of countries demonstrating sustained emissions reduction. The Government has set out its proposed level for the Seventh Carbon Budget, in line with our advice – a feasible, ambitious level. There has been positive action on low-carbon electricity over the past year, with record amounts of renewable capacity procured in the latest Contracts for Difference allocation round. However, while there have been some steps taken to reduce the costs of electricity, the Government’s plan for electrification lacks ambition. Indicators for some electric technologies are showing worrying signs: while electric car sales are keeping pace with government plans, electric van sales remain off track and the growth in heat pump installations in existing homes slowed significantly last year.

In October 2025, the UK Government published its Carbon Budget and Growth Delivery Plan (CBGDP), setting out its policies and plans for meeting carbon budgets. This plan projects slower emissions reductions for surface transport and buildings compared to the previous government’s plan. This reflects both slow prior progress in the roll-out of some technologies, as well as areas of reduced policy ambition. For example, the decarbonisation of public sector buildings and reduced support for low-income homes to electrify heating and install insulation. There is now a significant gap between the plan’s projected emissions reductions and the UK’s 2030 Nationally Determined Contribution (NDC) under the Paris Agreement, a commitment to reduce emissions by at least 68% compared to 1990 levels. Increasing ambition and achieving the 2030 NDC would put the UK on track to achieve its future carbon budgets and Net Zero by 2050, and send a strong international signal of commitment to delivery.

The slow pace of electrification is putting the UK’s climate targets at risk and is a missed opportunity to enhance UK energy security in the face of rising threats, leaving the UK exposed to geopolitical shocks. 93% of the UK’s emissions are now outside the electricity supply sector and around three-quarters of a typical household’s driving and home energy bills are from the direct use of fossil fuels in cars and gas boilers. Following the recent increase in fossil fuel prices, bills have increased almost four times more for a typical household with a gas boiler and a petrol car, compared to a household with a heat pump and an EV. For a rural household with an oil boiler and a diesel car, the increase is 10 times more.

Accelerating EV sales and heat pump installations beyond government plans would help address these challenges. It would keep the 2030 NDC in reach, improve the UK’s air quality, ease inflationary pressures from fossil fuel shocks, and reduce costs for consumers, giving them more spending power elsewhere in the economy. The UK could save up to 80 million barrels of oil and 1.5 billion therms of gas in 2030, which would cost almost £8 billion at current oil and gas prices. Electrification is the most effective form of energy efficiency: by 2050, the efficiency of a more electrified energy system would reduce wasted energy by around half compared to today.

Progress in other sectors, including agriculture, land use, and aviation, has also been too slow. In addition, the Government’s plan to achieve the Sixth Carbon Budget relies on a rapid ramp-up in engineered removals after 2030 but lacks detail on how this will be achieved.

The rate of global warming is at a record high, and the UK is already experiencing the impacts. Heatwaves have become hotter, longer, and more frequent. In 2026, the highest May temperature on record in the UK was recorded in Greater London. Early 2026 was exceptionally wet in parts of the UK, with long unbroken spells of rain leading to widespread flooding. The UK can end its contribution to ongoing global climate change by reaching Net Zero emissions and have a resilient transition that simultaneously considers actions to adapt to rising temperatures.

Key actions for electrification

Rapid progress over the next year is essential to keep the 2030 NDC in reach, with the pace of emissions reduction needing to almost double. To achieve this, the Government needs a more ambitious plan for electrification. It must urgently remove barriers facing households and businesses to transition to efficient, low-carbon electric technologies. Key actions for electrification include:

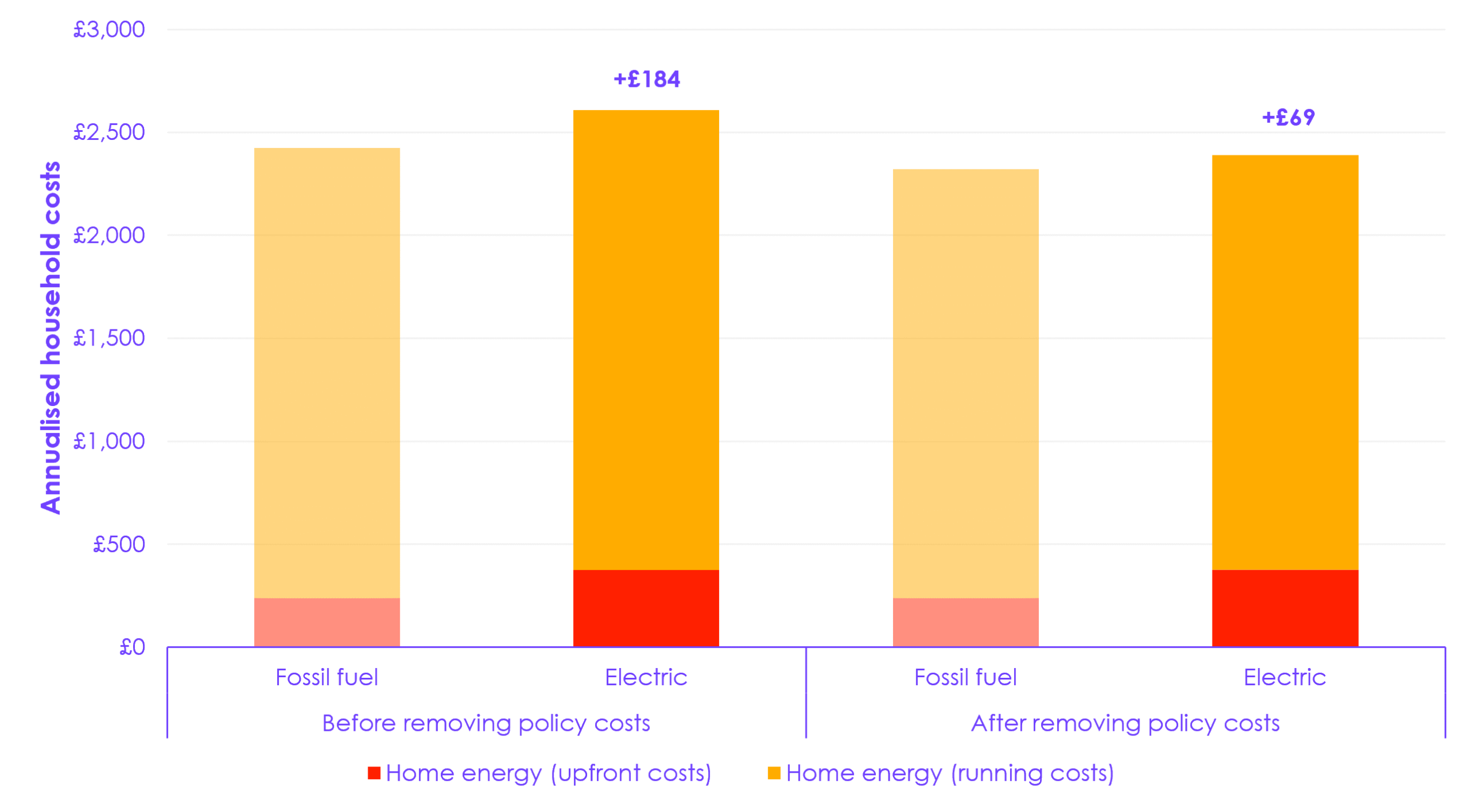

1. Make electricity cheaper. While progress has been made in the past year to remove some policy costs from electricity bills, this is not sufficient to incentivise many households and businesses to transition to low-carbon heating. Remaining policy costs should be removed from electricity bills for both households and non-residential users so that the greater efficiency of heat pumps compared to fossil fuel heating is reflected in lower bills. Lower bills would also improve the case for investing in the UK’s energy-intensive sectors.

2. Create the conditions for a more rapid transition to EVs. Propelled by the zero-emission vehicle (ZEV) mandate, the market continues to drive down the price of electric cars, allowing more households and businesses to benefit from the lower costs of EV ownership. With clear and consistent incentives and messaging, the adoption of electric cars can outpace current ambition, and the adoption of electric vans can catch-up. To flourish, the UK car industry needs to continue its pivot to the technologies of the 21st century. This requires the Government to stand firm behind the ZEV mandate and remove barriers to EV adoption. Crucial to this is increasing access to affordable charging, allowing the one-third of homes without access to off-street parking to benefit from lower running costs. It is also important to remove regulatory barriers and minimise any ‘hassle factor’ to consumers from the planned introduction of electric vehicle excise duty.

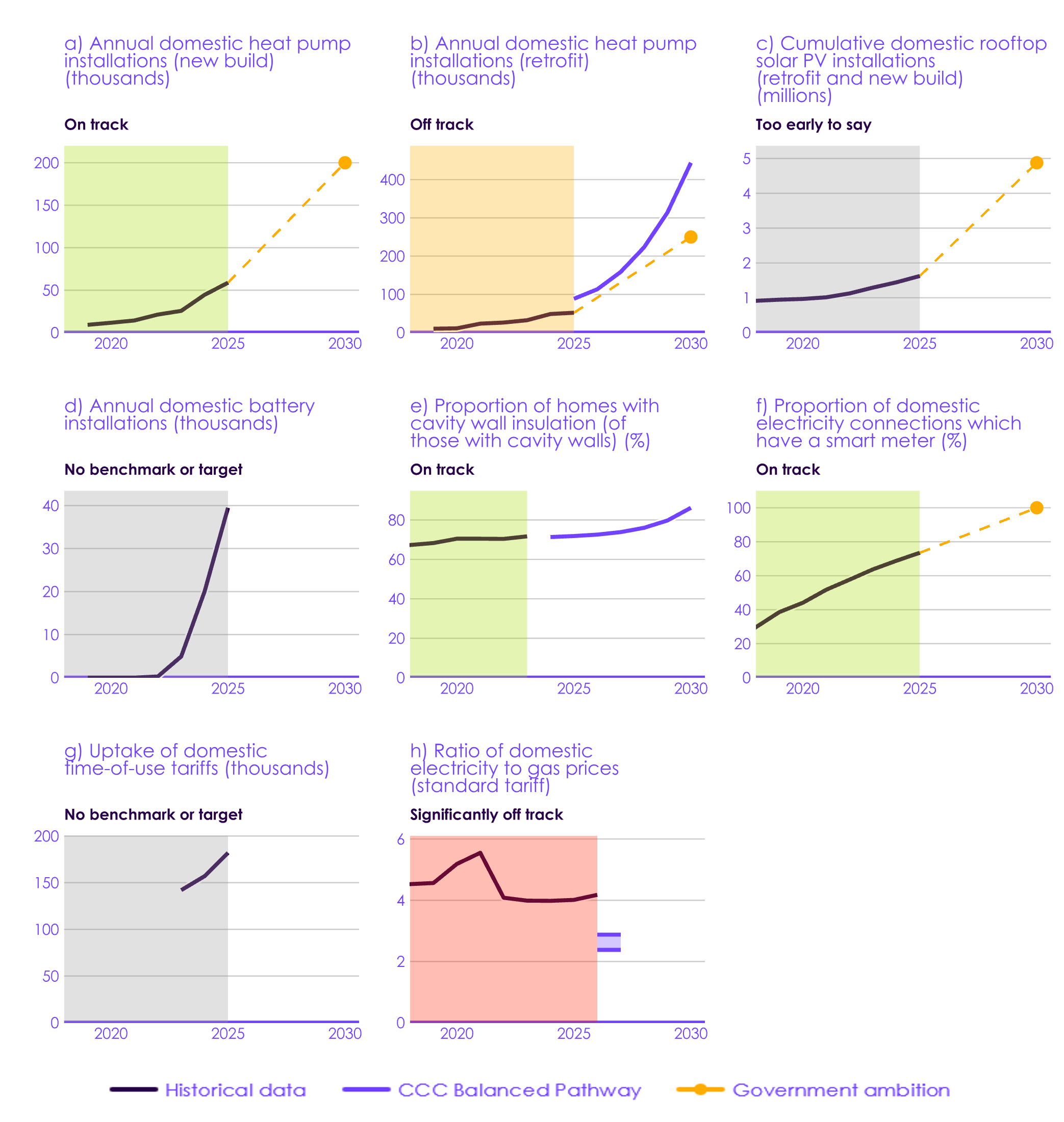

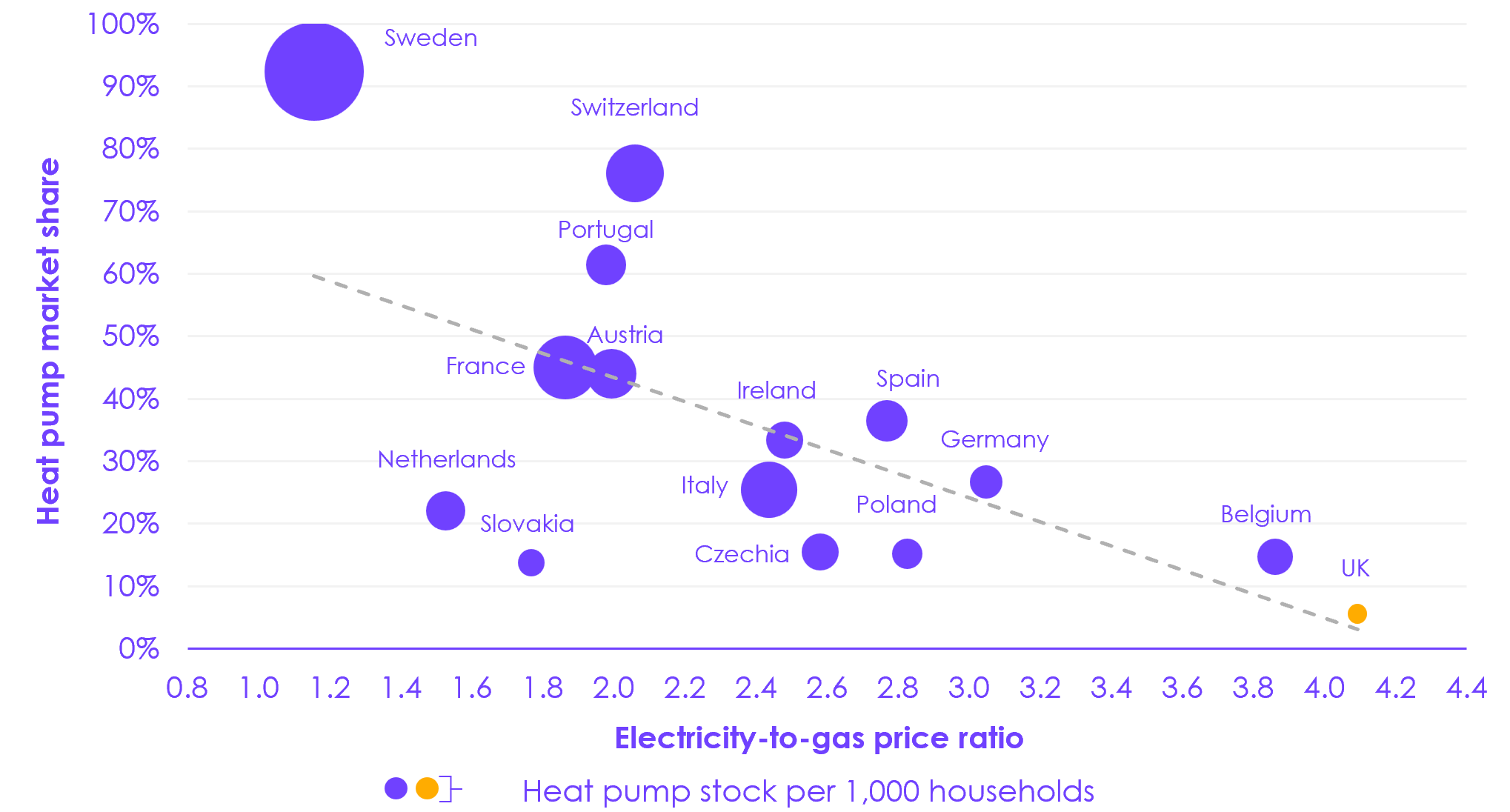

3. Accelerate the installation of heat pumps in buildings. The UK has one of the lowest market shares of heat pump installations in Europe (Figure 4). The Government must ensure installations accelerate in all segments of the market by:

- Urgently addressing the gap left by the closure of the Energy Company Obligation (ECO) scheme. In the last three years, this scheme accounted for around a third of retrofit heat pump installations in the UK, providing targeted support for low-income households. Without a sufficient replacement, installations could fall significantly this year.

- Removing any unnecessary barriers that make a heat pump harder to install than a gas boiler, so that low-carbon heating installations become the default choice by 2035. This could be done by: reducing regulatory barriers, addressing skills gaps, improving advice to households and businesses, and enabling market conditions which reduce installation costs.

- Introducing a comprehensive programme to decarbonise public sector buildings, following the closure of the Public Sector Decarbonisation Scheme. The Government should consider restricting the installation of fossil-fuel boilers in public buildings. Moving instead to low-carbon combined heating and cooling systems can both reduce fossil fuel dependency and protect vulnerable people from rising temperatures, as set out in the Climate Change Committee’s (CCC) Adaptation Committee report on A Well-Adapted UK, published earlier this year.

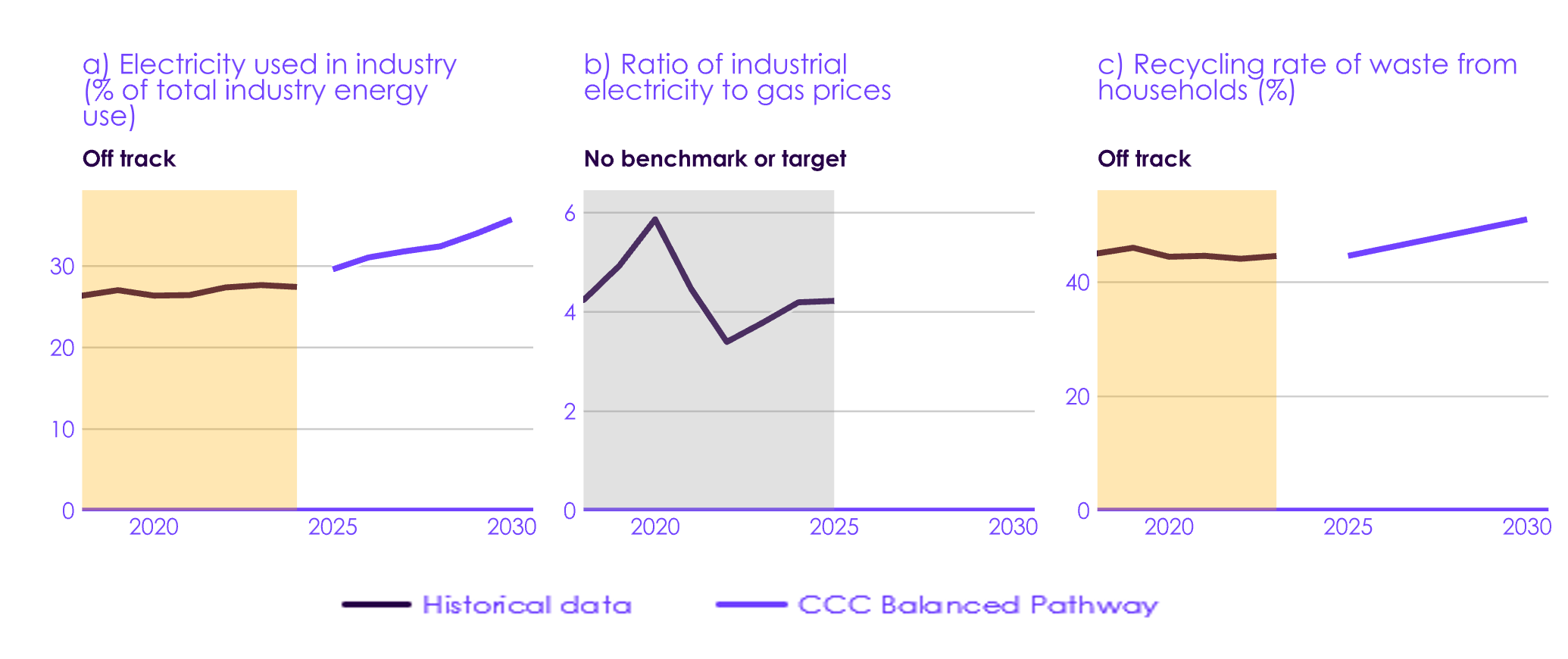

4. Deliver on industrial electrification. Exemptions to electricity network and policy costs will not be sufficient to incentivise industrial electrification on their own. The Government should now set out a plan to deliver its ambition for industrial electrification. This should confirm suitable use cases and establish the conditions necessary to make electrification the economically rational choice – addressing both capital and operating cost barriers.

Impacts of electrification on household energy costs

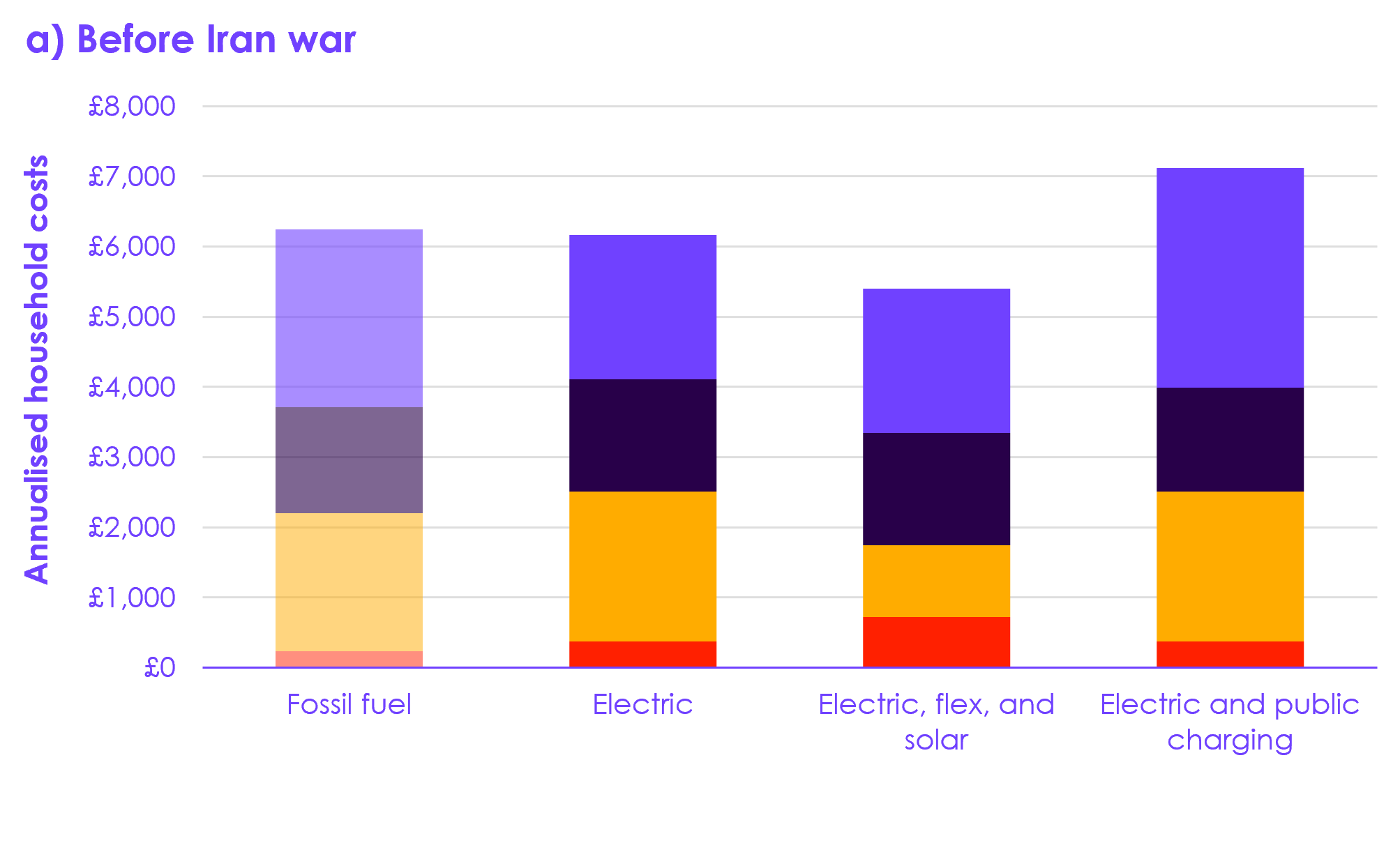

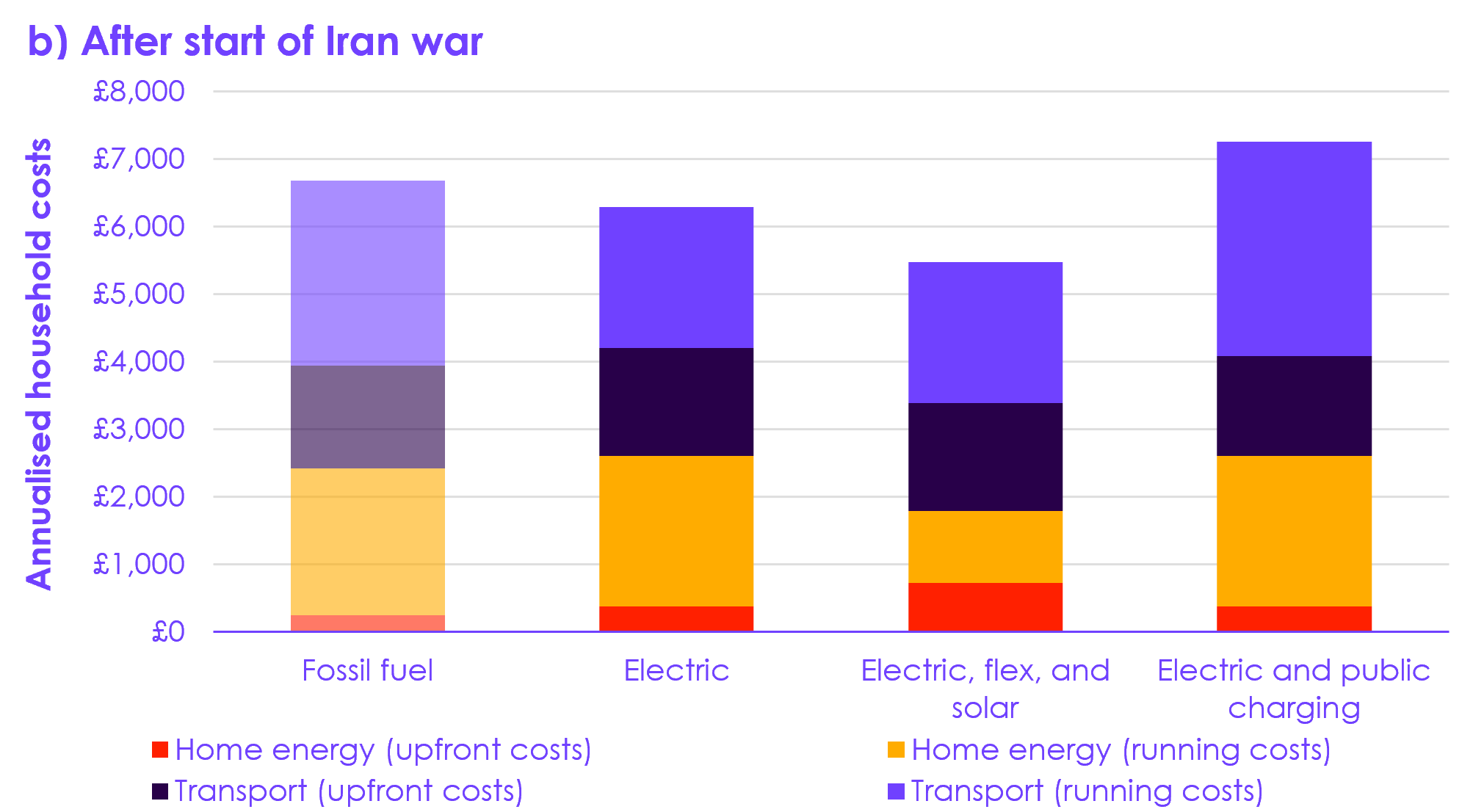

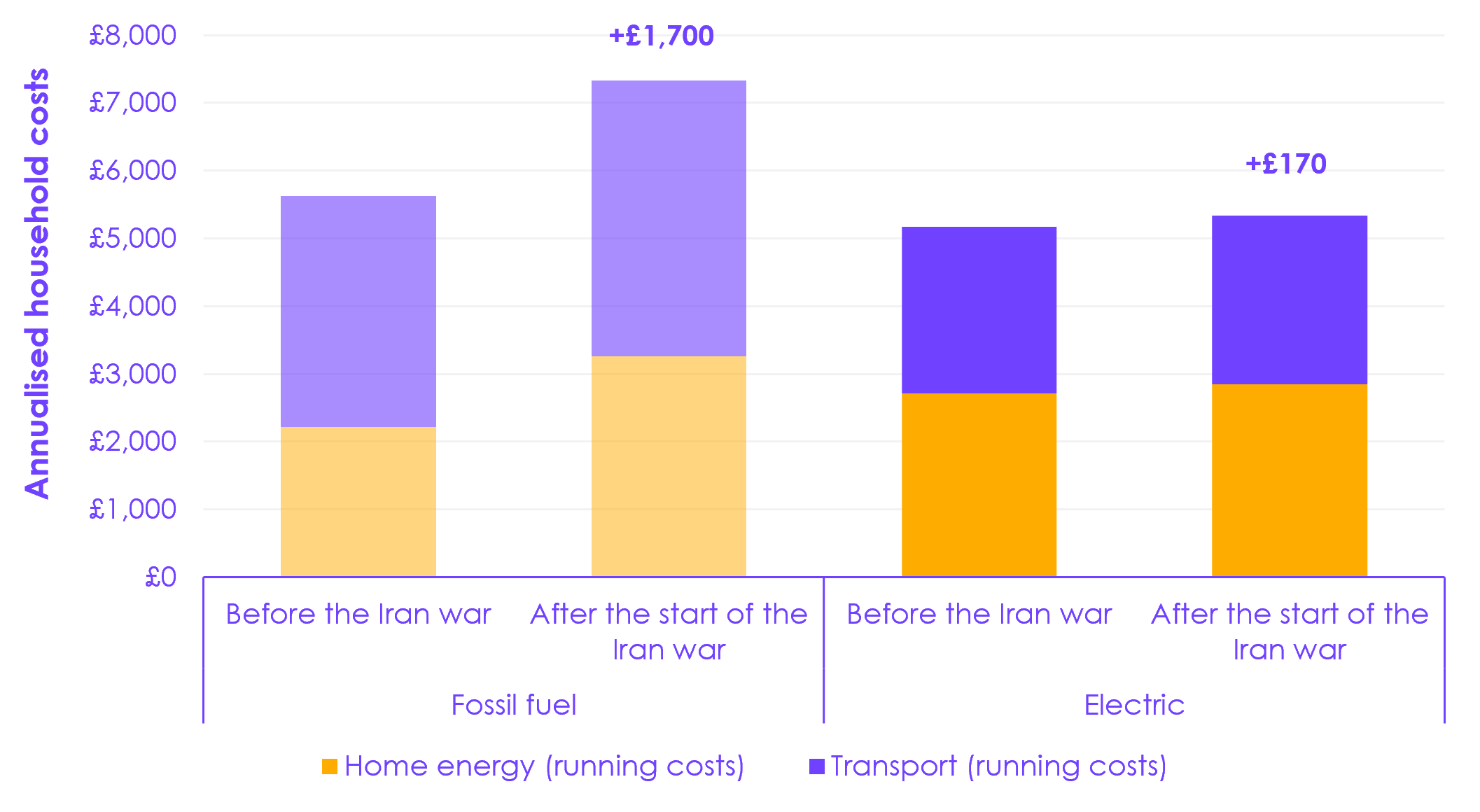

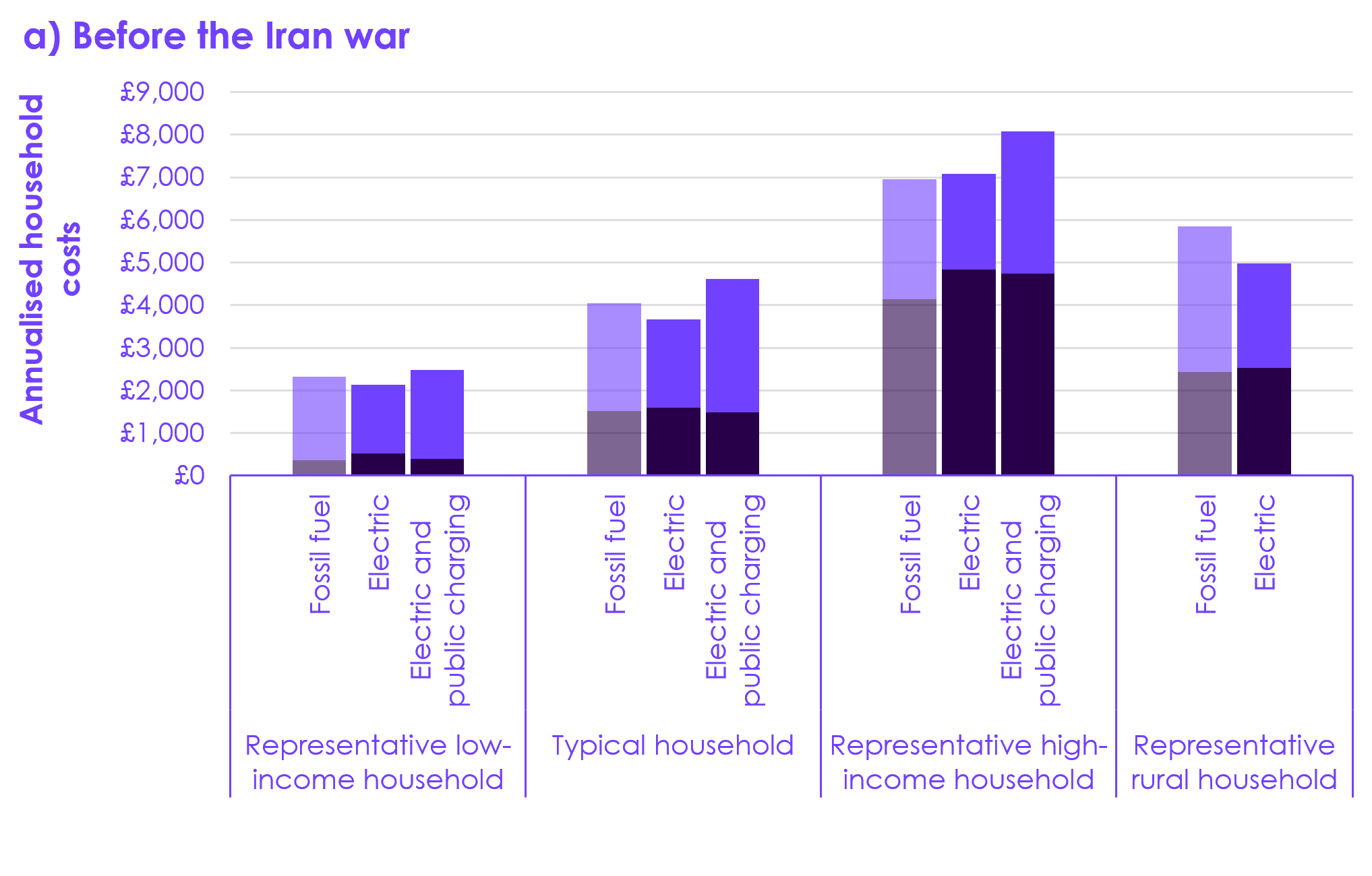

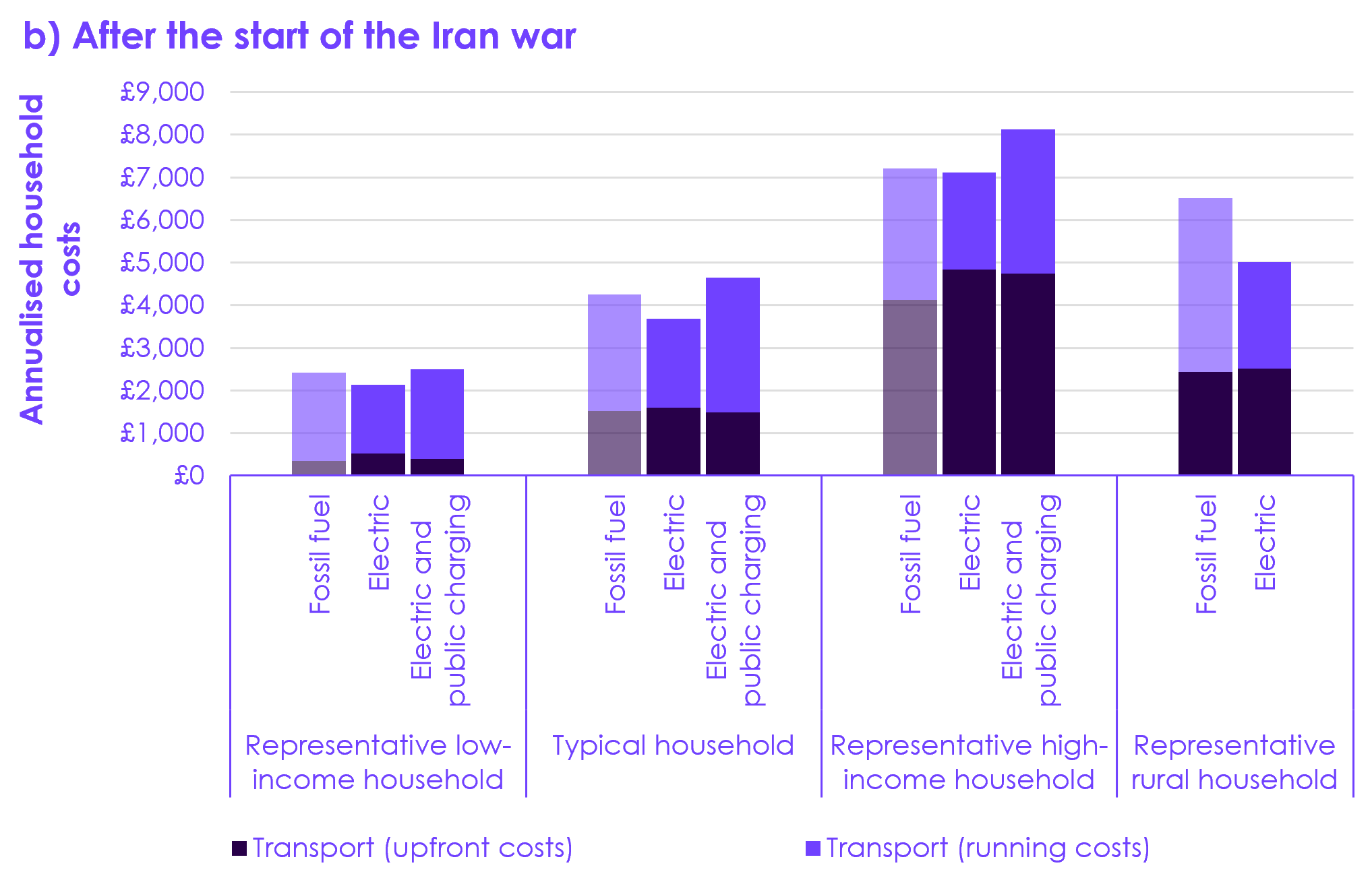

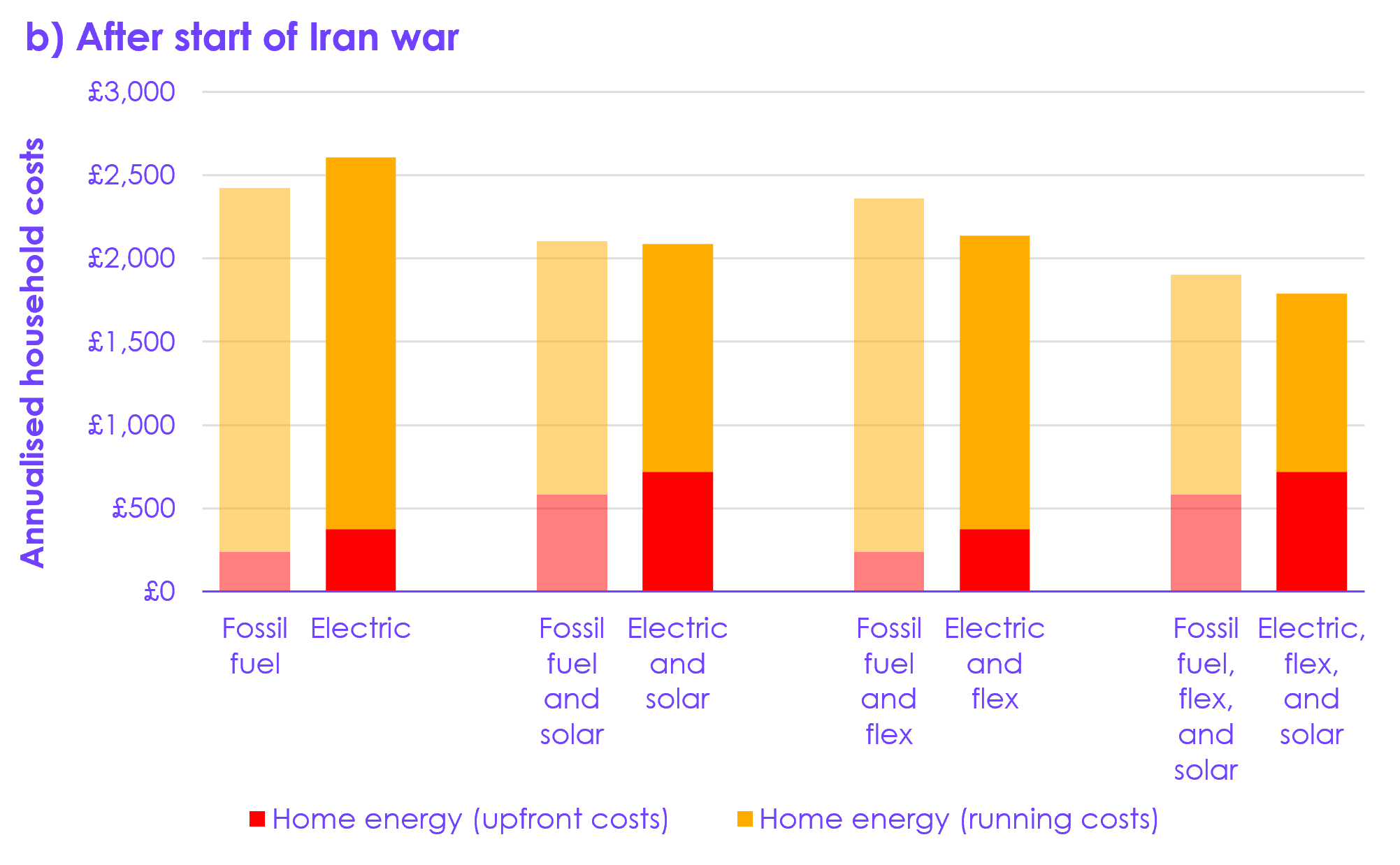

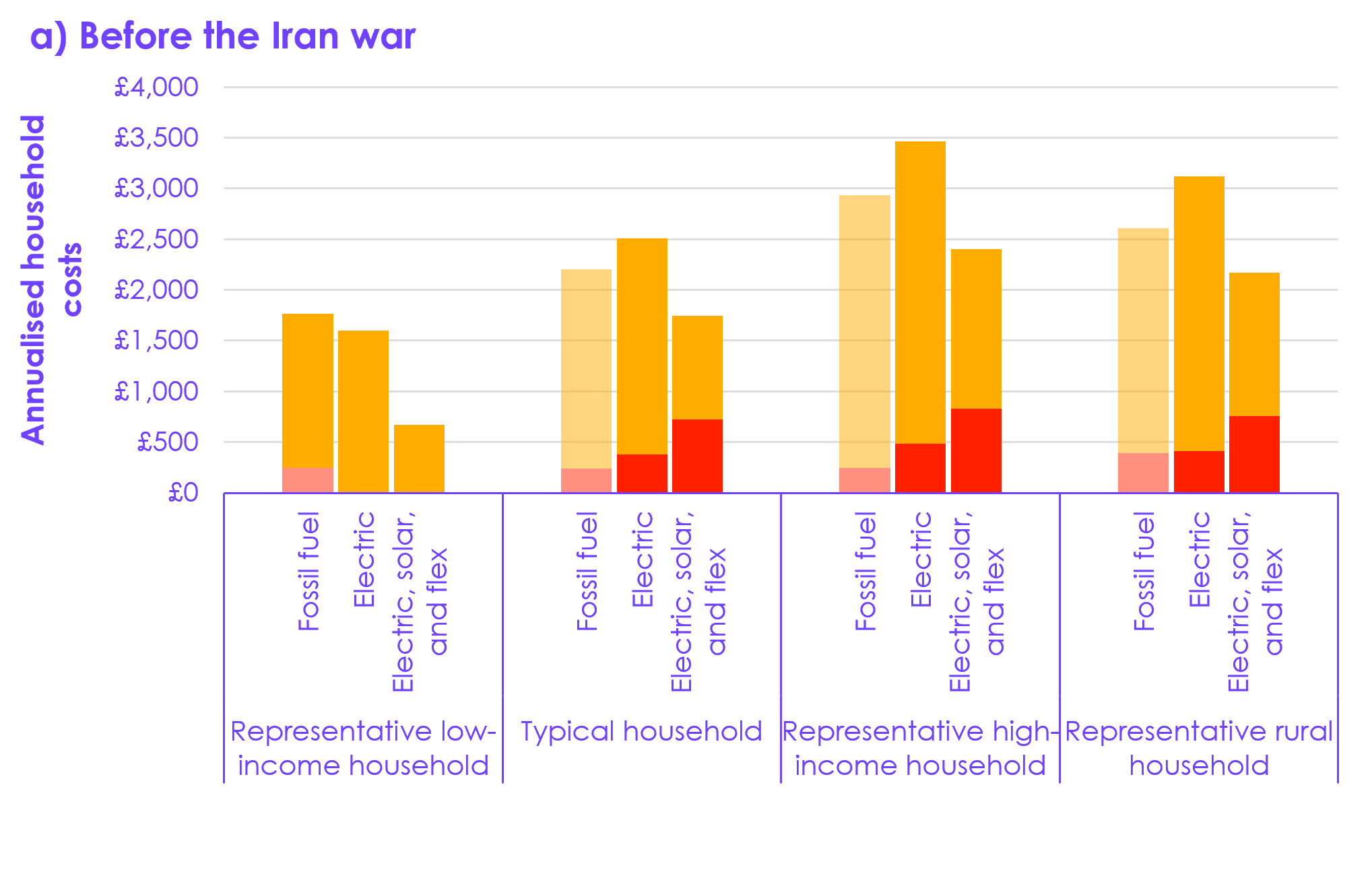

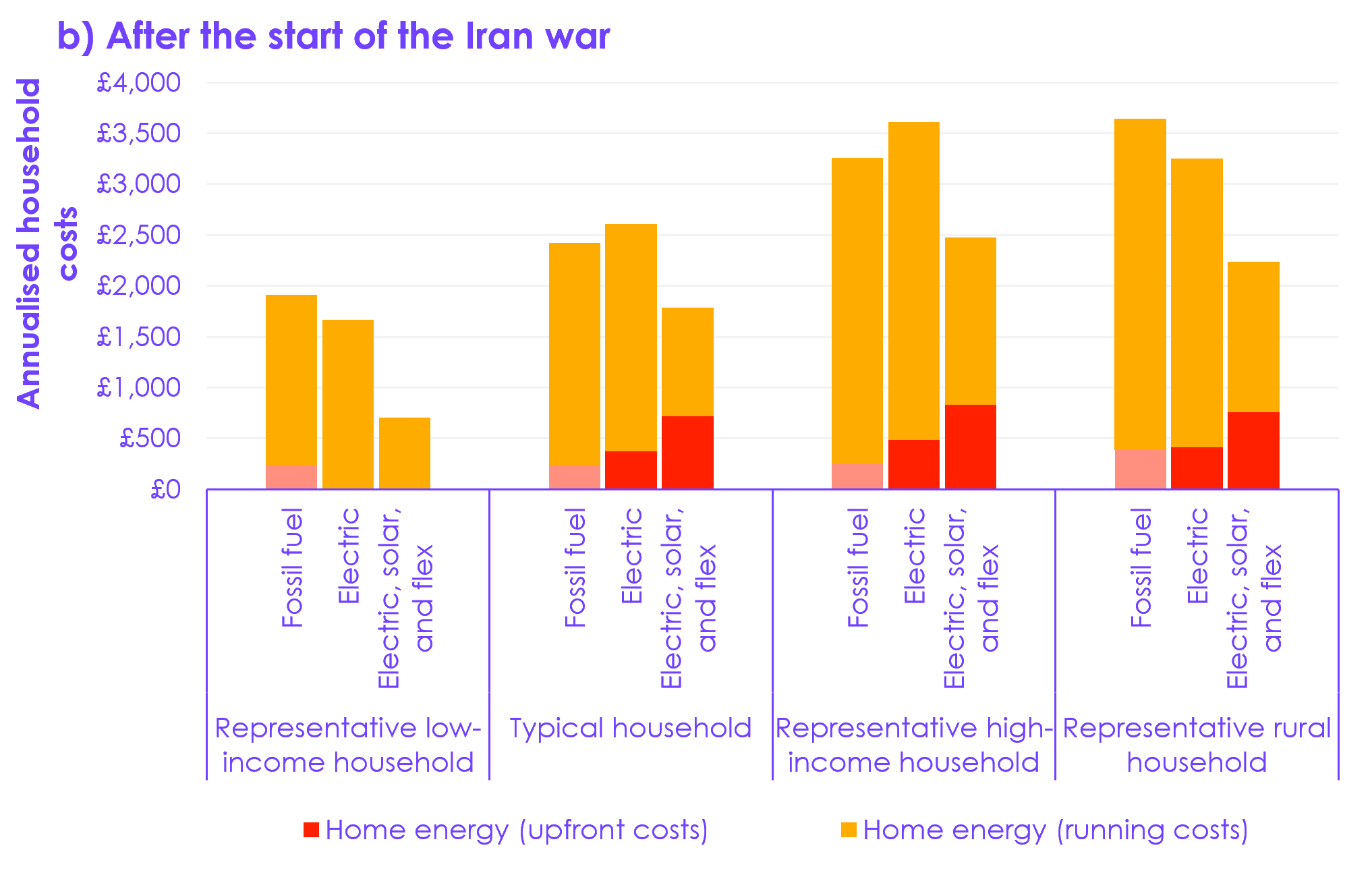

A typical UK household will see lower and less volatile bills overall if they have an EV and a heat pump, rather than a petrol car and a gas boiler, under current government policies (Figure 1). This is true for prices both before and since the start of the Iran war, with recent energy cost increases having strengthened this effect.

- Energy prices have risen since the start of the war. Given this, a typical household with a gas boiler and petrol car would save around £1,210 a year by installing solar panels and switching to a time-of-use tariff, a heat pump, and an EV. A rural household with an oil boiler and a diesel car could save around £1,880 a year, even without solar or time-of-use tariffs.

- The majority of savings come from the reduced running costs of electric cars. Most households would now save by switching to an EV, provided they are able to charge at home. However, high public charging costs mean this is not true for all households.

- The Warm Homes Plan increased government support for solar panels and heat pumps. With this support, installing solar panels, combined with time-of-use electricity tariffs available in the market, can make heat pumps cheaper than a gas boiler for a typical household.

- However, not all homes are suitable for solar panels or time-of-use tariffs, and many would not currently save from switching to a heat pump alone.

- Making electricity cheaper would enable many more households to save by switching to heat pumps, and would further reduce the UK’s exposure to volatile international gas markets.

- Installing low-cost insulation measures such as draught proofing and insulating hot water tanks can also help reduce household bills and emissions.

Historical progress in reducing emissions

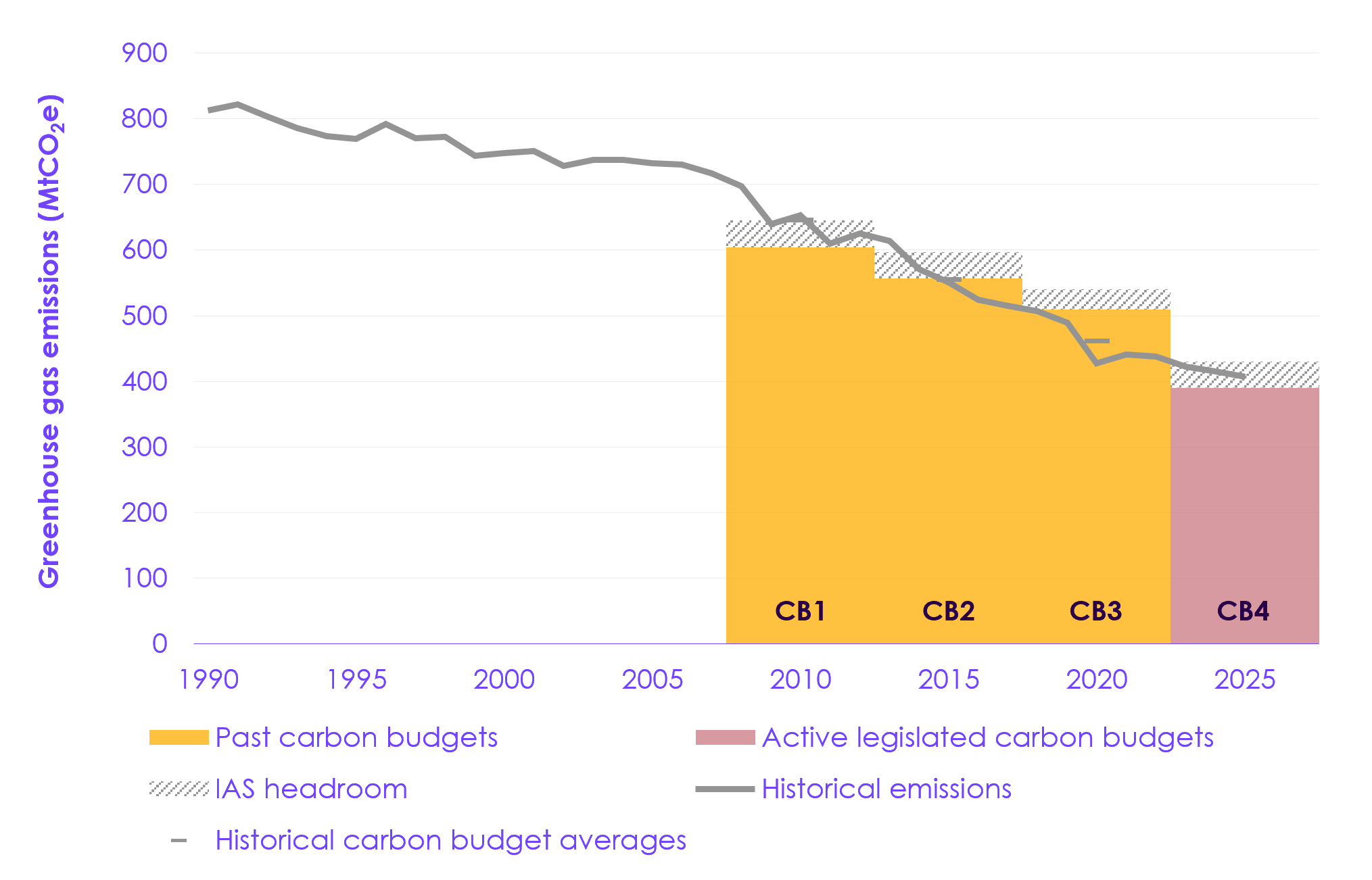

GHG emissions in the UK fell by 1.8% in 2025 compared to the year before, reaching 407 MtCO2e, according to provisional estimates. Levels are now 50% lower than those seen in 1990. The first three carbon budgets (2008 to 2022) were achieved and emissions are well on track to achieve the Fourth Carbon Budget (2023 to 2027), with emissions in 2025 already lower than the annual average required over the remainder of the carbon budget period.

- There has been a long-term trend of emissions reduction in electricity supply, which has historically driven progress in reducing the UK’s emissions overall. The electricity supply sector is responsible for almost half of the emissions reduction since 2008 and has seen continuous progress in reducing both coal- and gas-powered generation, while renewable generation has increased. However, electricity supply emissions did not fall in 2025. While emissions from coal fell to zero that year, gas generation rose slightly, driven by a combination of factors including a fall in net imports of electricity and nuclear outages.

- Emissions in surface transport increased by 2.7% in 2025, according to provisional estimates. The incremental progress in the roll-out of EVs from year-to-year is likely to have been offset by other factors, such as increased vehicle-kilometres. However, the impact of EVs is apparent in longer-term trends – despite car-kilometres having almost returned to 2019 levels, car emissions are 12% lower than in 2019. Around half of this reduction is likely due to the uptake of EVs. As the UK’s highest emitting sector, it is essential to see these savings grow and begin to reduce emissions year-on-year, by accelerating the sale of EVs.

- Emissions in industry fell in 2025, largely due to the closure of the blast furnaces at Port Talbot steelworks in the second half of 2024. Construction has commenced to replace them with an electric arc furnace, supported by a £500 million government grant. However, there has been limited progress on wider industrial electrification.

- Emissions also fell in fuel supply and buildings – the latter despite colder winter months in 2025 than the year before. This could be from high energy prices continuing to reduce energy demand. The number of heat pumps currently being installed is not yet enough to have a significant effect on emissions.

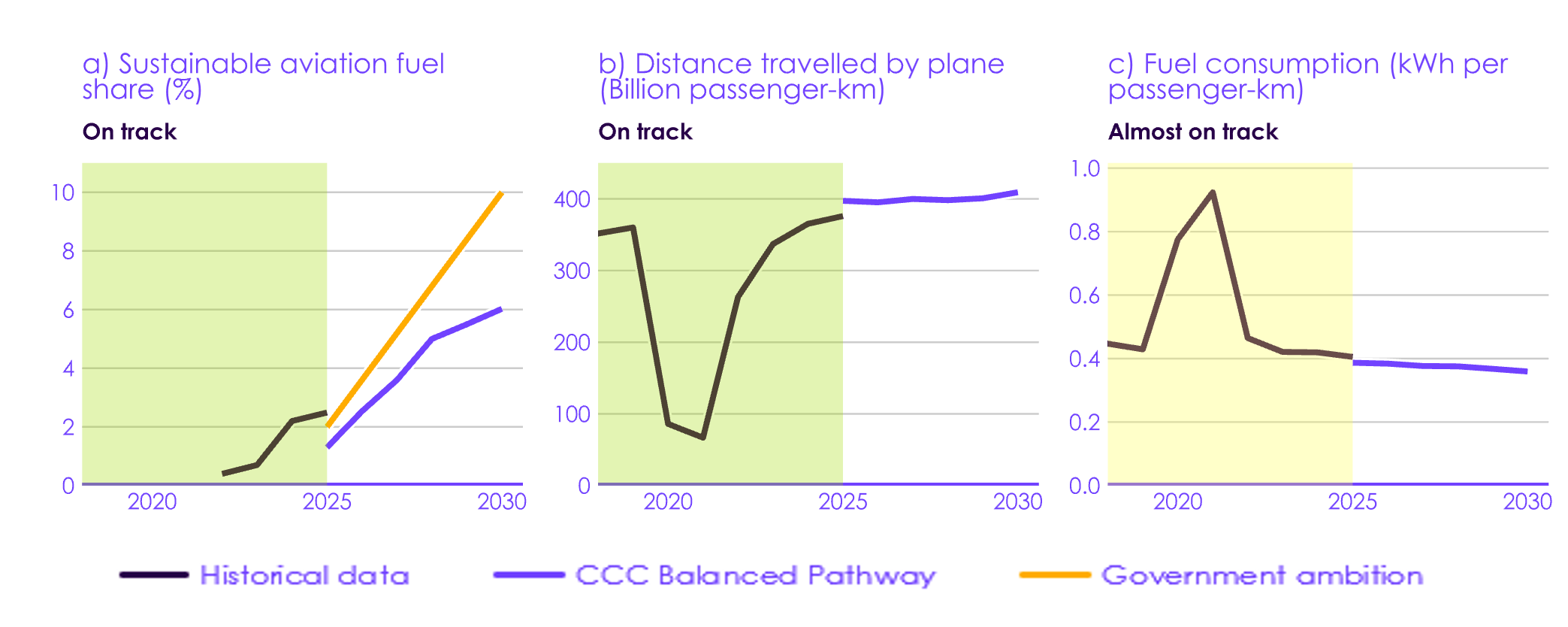

- Emissions in aviation fell slightly, by 0.5%, in 2025, despite a 3% increase in passenger-kilometres. This is likely due to efficiency improvements from recent changes to the aircraft fleet and a small contribution from sustainable aviation fuel (SAF) uptake.

- Emissions in agriculture and land use have not fallen significantly in recent years. While reductions in livestock numbers led to a reduction in methane emissions between 2022 and 2024, this was offset by an increase in CO2 emissions in these sectors. This was in part driven by a smaller forestry sink due to an aging woodland profile and removal of trees for habitat restoration priorities.

The UK Government’s Carbon Budget and Growth Delivery Plan

The UK Government’s Carbon Budget and Growth Delivery Plan (CBGDP) sets out its policies and plans to meet the Fourth Carbon Budget (2023 to 2027), Fifth Carbon Budget (2028 to 2032), and Sixth Carbon Budget (2033 to 2037). The CBGDP supersedes the previous government’s 2023 Carbon Budget Delivery Plan (CBDP).

- Emissions in the CBGDP reduce more slowly in the surface transport and buildings sectors compared to the CBDP, and the CBGDP pathway falls short of meeting the 2030 NDC – while the UK Government states that it “is committed to delivering [this target]”.

- The 2030 NDC is the first of the UK’s targets in line with Net Zero and achieving it would put the UK on track to achieving the Sixth Carbon Budget. The Fourth and Fifth Carbon Budgets were set before the UK had a Net Zero target and will need to be overachieved.

- The success of the Paris Agreement relies on countries making best efforts to achieve their NDC targets. The UK has a reputation for international leadership which has helped drive progress in tackling climate change at the global level. Having set an ambitious target for 2030, it would send a strong signal to deliver on it.

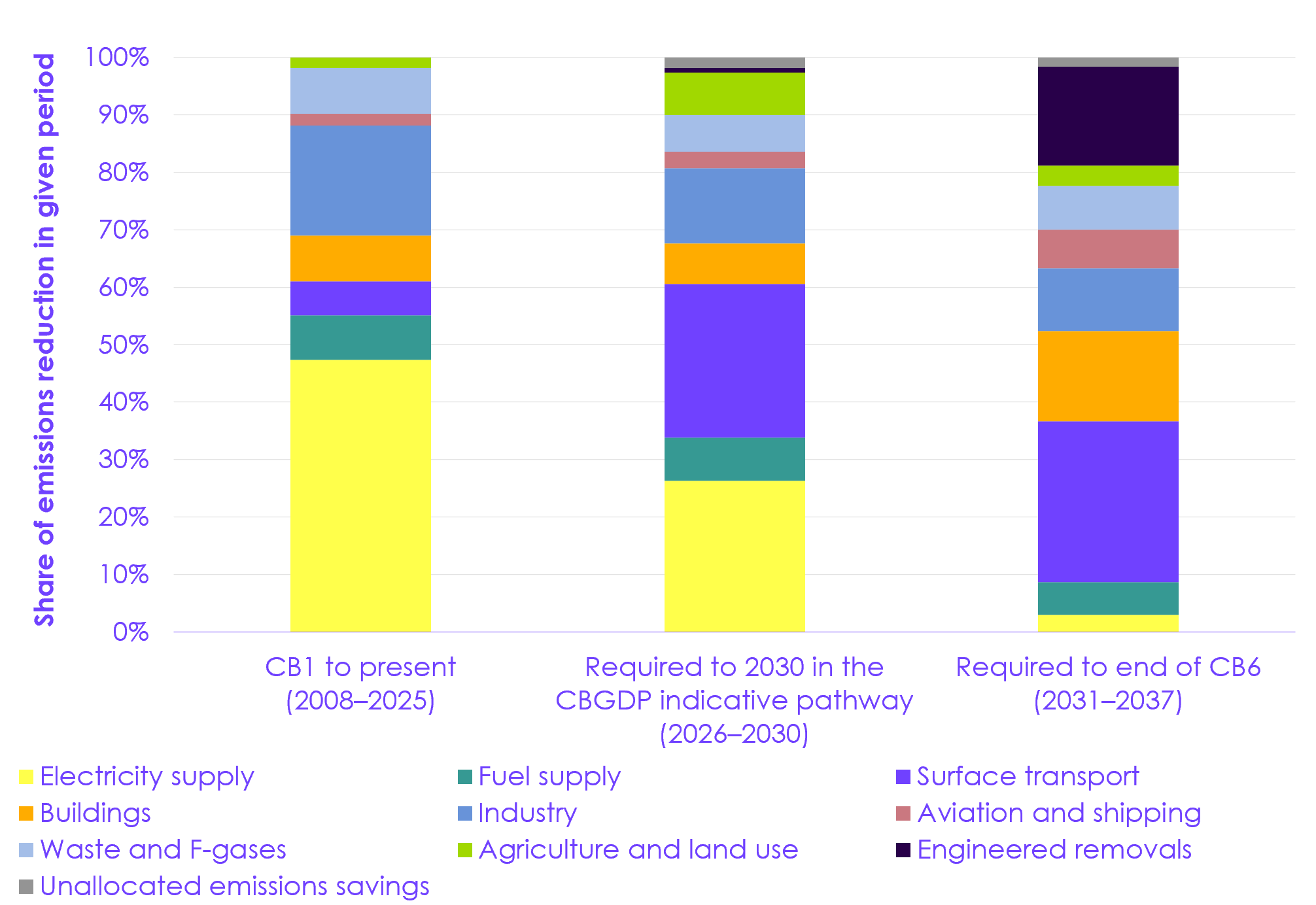

While nearly half of the emissions reductions seen to date have been in electricity supply, the CBGDP makes clear that action now needs to broaden across a wider range of sectors (Figure 2).

- The Government’s pathway relies predominantly on electrification and further expansion of low-carbon electricity supply to meet the carbon budgets.

- Around half of the emissions reductions in the Government’s pathway to 2030 are in the surface transport, buildings, and industry sectors. Uptake of EVs, heat pumps, and other electric technologies will be the key driver of this change. There is potential for the Government to go faster and keep the 2030 NDC in reach.

- The Government’s pathway relies on a rapid ramp-up in engineered removals to meet the Sixth Carbon Budget, with removals contributing 17% of emissions reductions over the period 2031 to 2037. But the plan lacks detail on how this will be achieved. Given the risk with this approach, a clear strategy for how this scale-up will be delivered and how progress will be monitored is needed. This should also be linked with contingency plans.

The Government should have a more ambitious plan to accelerate electrification. This would keep the 2030 NDC within reach, increase delivery confidence for the Sixth Carbon Budget, enhance energy security, and allow households and businesses to benefit from more stable energy prices.

- With new EVs nearing price parity with equivalent petrol cars, and having reached it in some segments of the market, there is a particular opportunity to deliver a more rapid transition to electric driving.

- The CBGDP pathway for heat pump installations is unambitious compared to the market growth rates that have been seen in other European countries. With the right mechanisms and market signals in place, there is scope for heat pump deployment to go faster in both residential and non-residential buildings.

- The Government could also consider more steps to encourage modal shift and low-cost insulation measures in buildings, which would reduce emissions and demand for fossil fuels.

Assessment of delivery and policy progress

We have assessed the credibility of the Government’s policies and plans to deliver the emissions reductions set out in the CBGDP. When doing this, we consider progress on a range of delivery indicators, assessing whether the combined actions of governments and markets are delivering the changes needed.

There has been some positive progress over the past year – especially in low-carbon electricity deployment, continued growth in EV sales, increases in peatland restoration rates, and the publication of key government strategies such as the Warm Homes Plan, the Land Use Framework for England, the Clean Energy Jobs Plan, and the Energising Britain public participation strategy.

- The UK is halfway through the Fourth Carbon Budget (2023 to 2027) and is well on its way to achieving it. This shows good progress from both the current and previous governments. There are also credible policies in place to achieve the Fifth Carbon Budget (2028 to 2032).

- However, these budgets were set before the UK had a Net Zero target and achieving them does not set the country on the appropriate path to achieve the 2030 NDC, the Sixth Carbon Budget, or Net Zero emissions by 2050. These budgets must therefore be over-achieved.

- For the 2030 NDC and Sixth Carbon Budget (2033 to 2037), progress has been too slow, with insufficient focus on electrification and limited progress in other sectors. The Government’s plan carries significant risks in some sectors and does not achieve the 2030 target.

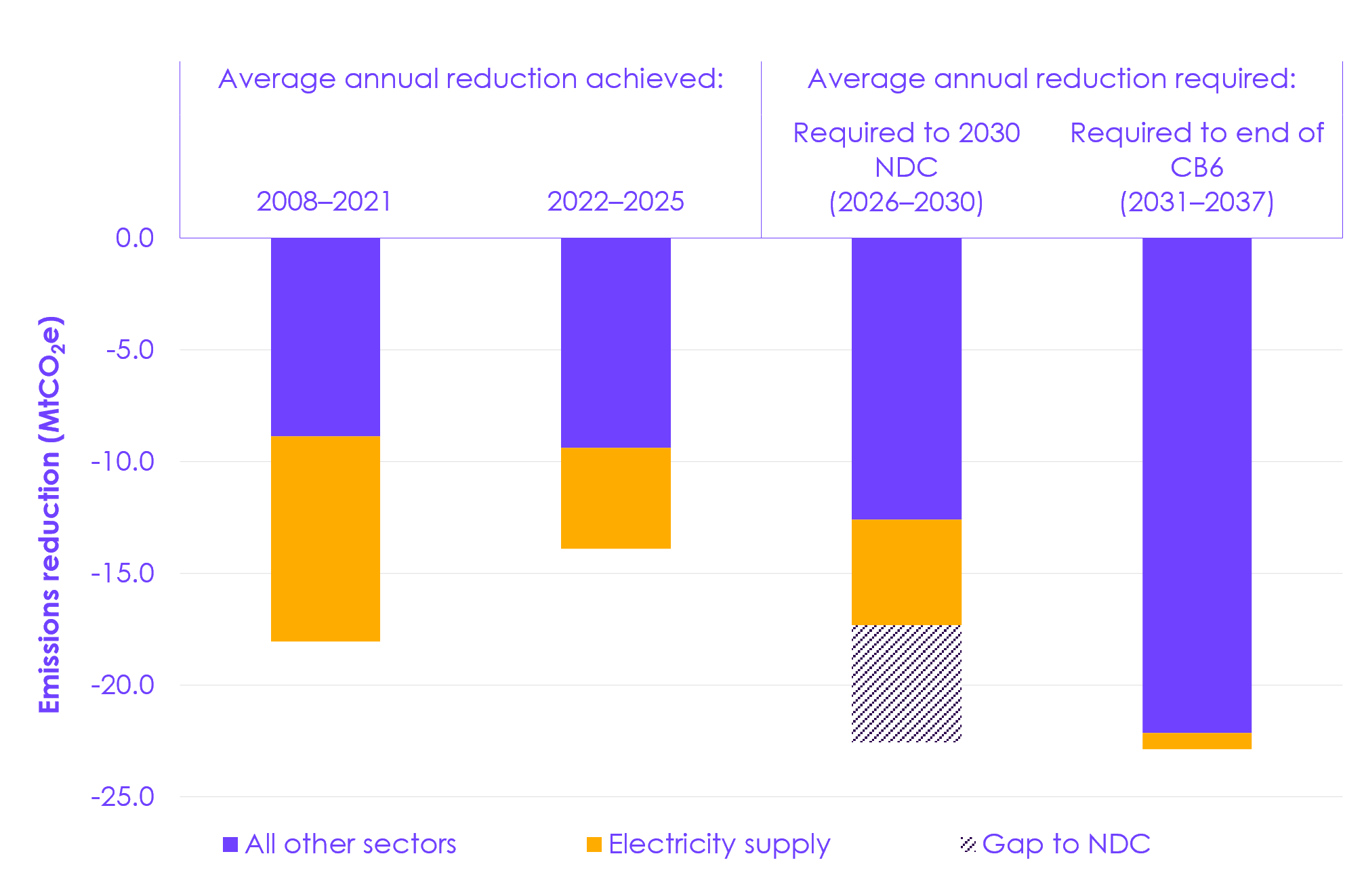

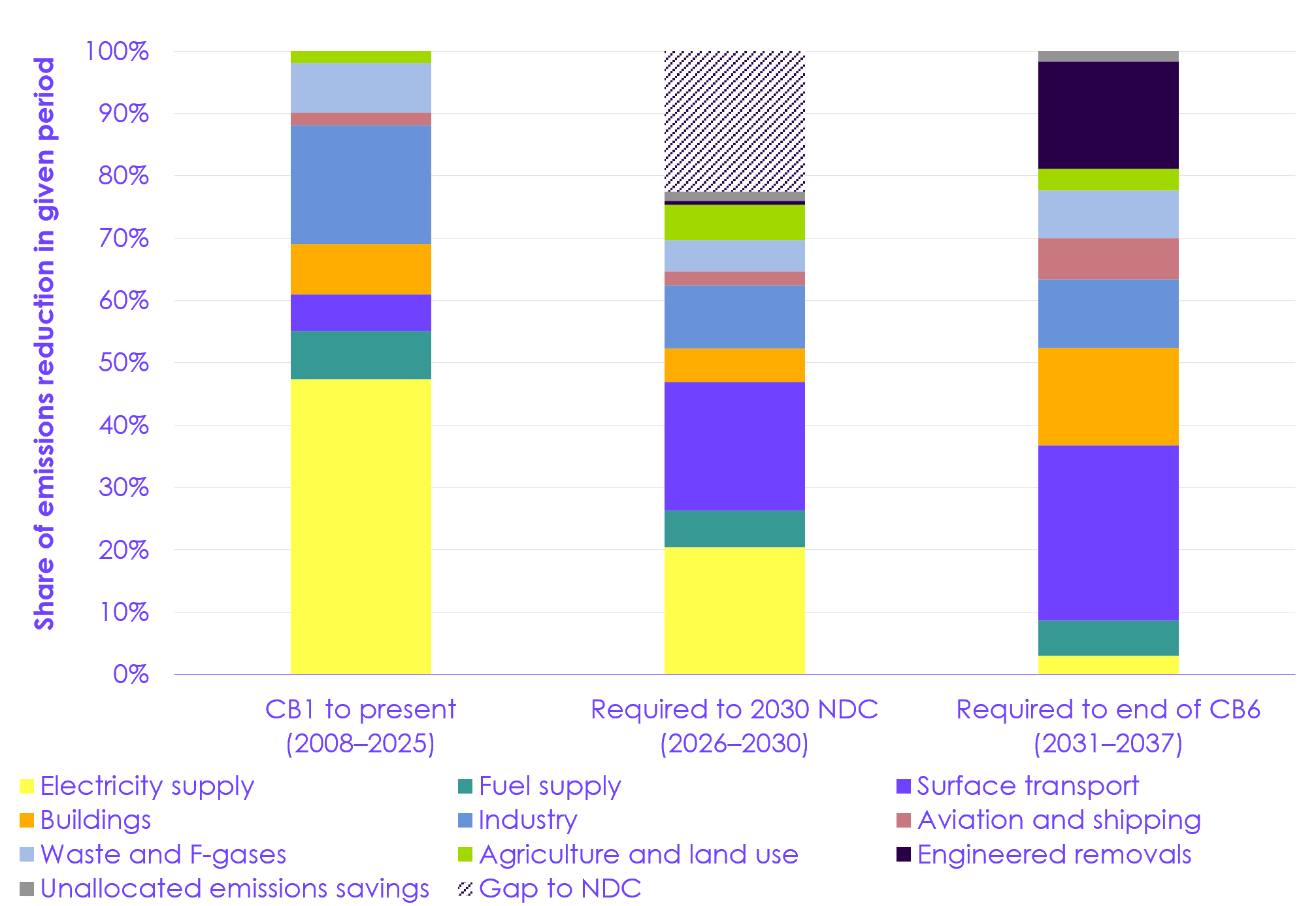

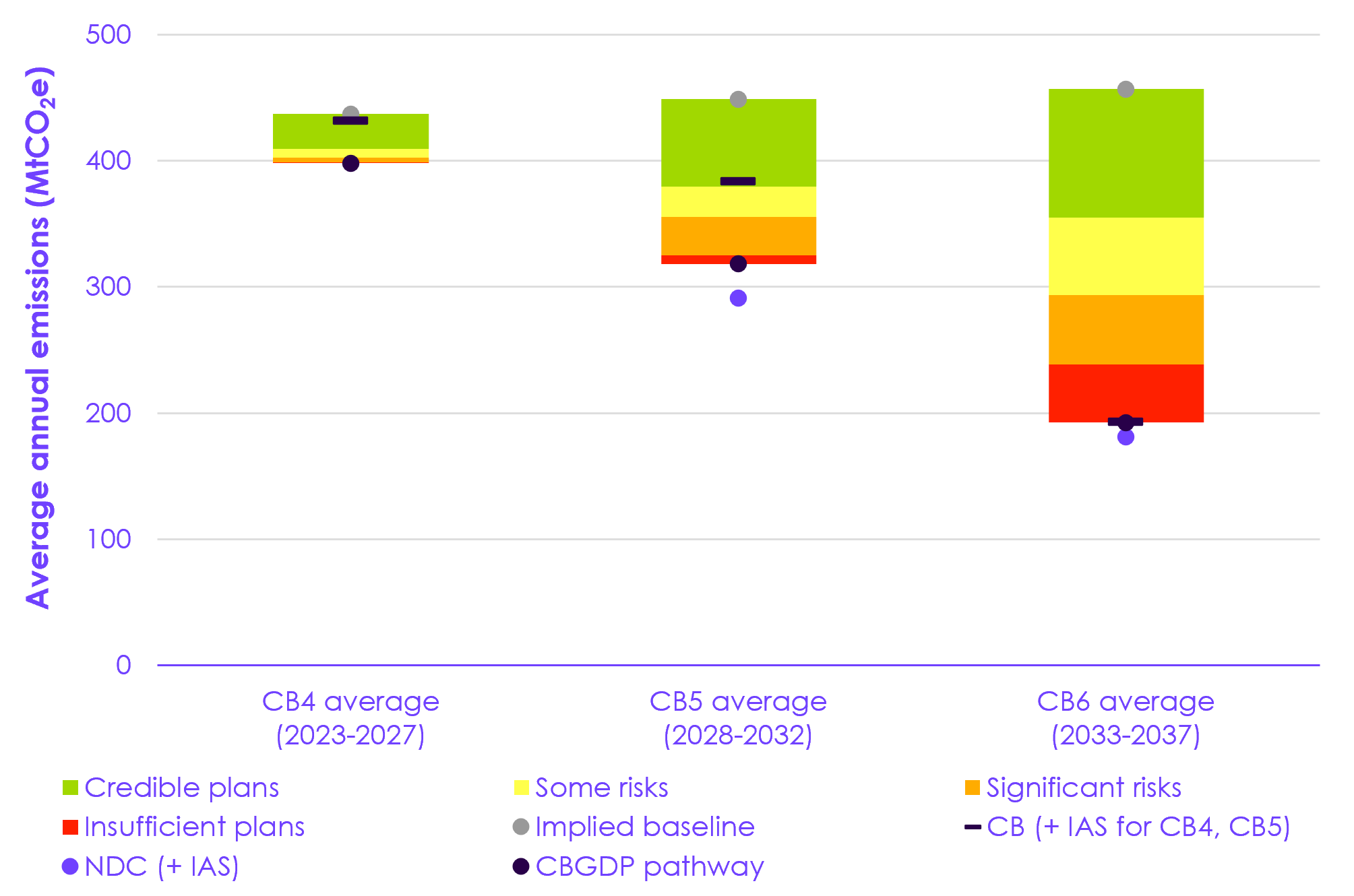

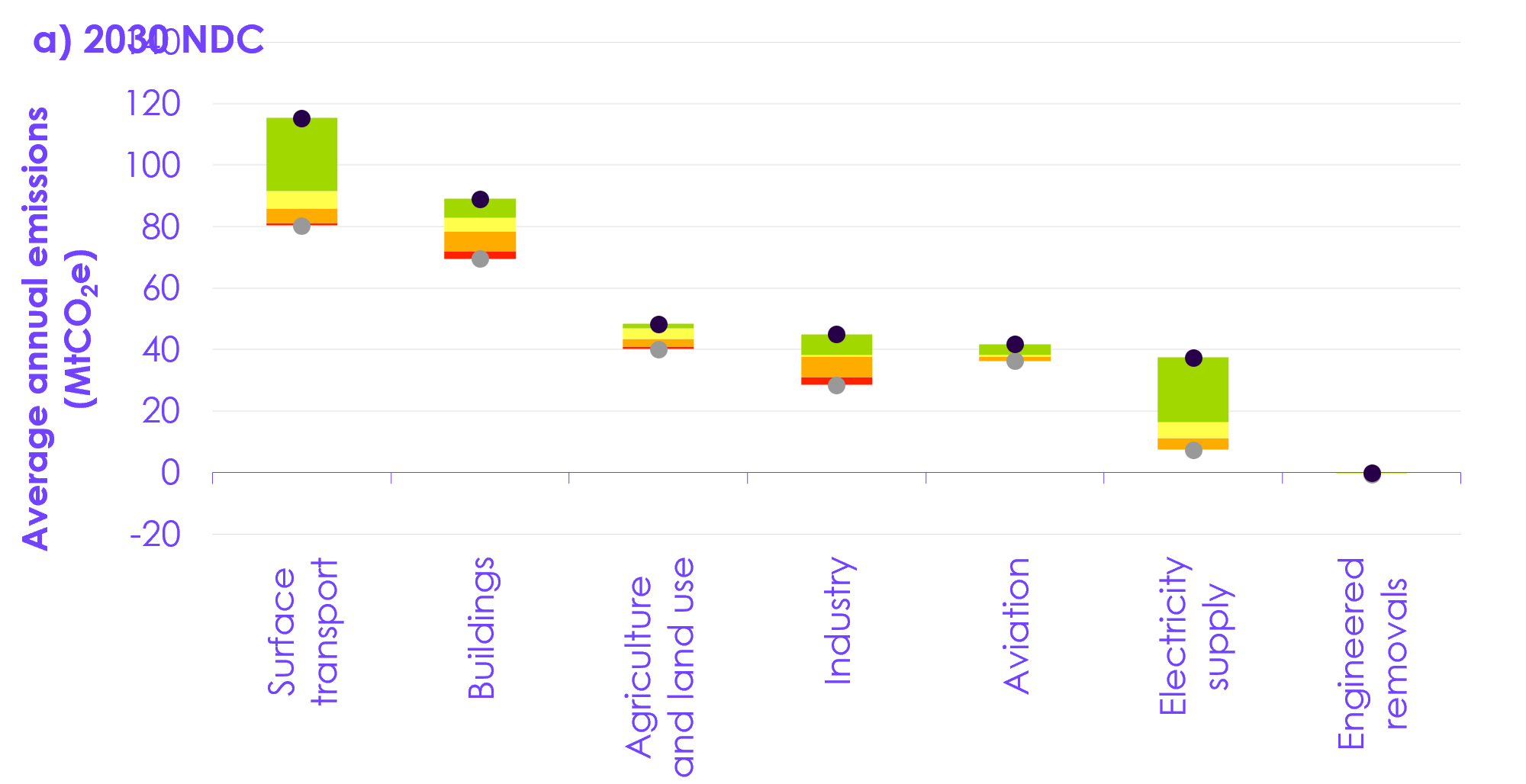

Meeting the 2030 NDC would require emission to fall to 291 MtCO2e by 2030. In our assessment, we find that credible plans or plans with only some risks would be sufficient to reduce emissions to 356 MtCO2e by 2030, which is equivalent to a 60% reduction on 1990 levels when international aviation and shipping emissions are excluded (as they are in the 68% reduction required to achieve the 2030 NDC). This is around an 11 MtCO2e improvement compared to our assessment last year. Among these, the proportion covered by credible plans has also increased since last year’s assessment (Figure 3).[1] This leaves a shortfall of 64 MtCO2e of further emissions reductions required to achieve the 2030 NDC, which we assess as being covered by plans with significant risks, insufficient plans, or which are not covered in the Government’s pathway.

- Credible plans exist for 44% of the required emissions reductions. The majority of credible plans relate to emissions savings from the continued roll-out of renewable electricity generation and EVs. There are also contributions from low-carbon heating in new builds and heat pump installations funded under the Boiler Upgrade Scheme, electrification of steel production at Port Talbot, and a proportion of SAF uptake covered by the SAF mandate.

- There are some risks attached to 15% of the required emissions reductions. Key policies and proposals with some risks include policies to decarbonise heavy goods vehicles, the delivery of additional renewable generation beyond that contracted, peatland restoration, and reducing waste in landfill. There are also some risks around the Government’s reliance on cascade effects, for example, where a household switching to an EV may be more likely to get a heat pump.

- There are significant risks attached to 19% of the required emissions reductions. This includes policies relating to low-carbon heating in homes beyond existing grant schemes, the decarbonisation of steel production at Scunthorpe steelworks, second- and third- generation SAF supply, and agriculture policies. It also includes the CBGDP’s reliance on wider factors relating to technological optimisation to bring down emissions.

- Insufficient plans exist for 4% of the required emissions reductions. This includes low-carbon heating in public and commercial buildings and in low-income homes, following the closure of the ECO scheme. It also includes a significant proportion of the electrification of industry.

- The remaining 17% of the required emissions reductions are not covered by the CBGDP policies and plans. This reflects the fact that the CBGDP pathway does not achieve the 2030 NDC. The Government will need to bring forward additional policies and plans to make up this gap, for example increased ambition in the roll-out of EVs and heat pumps.

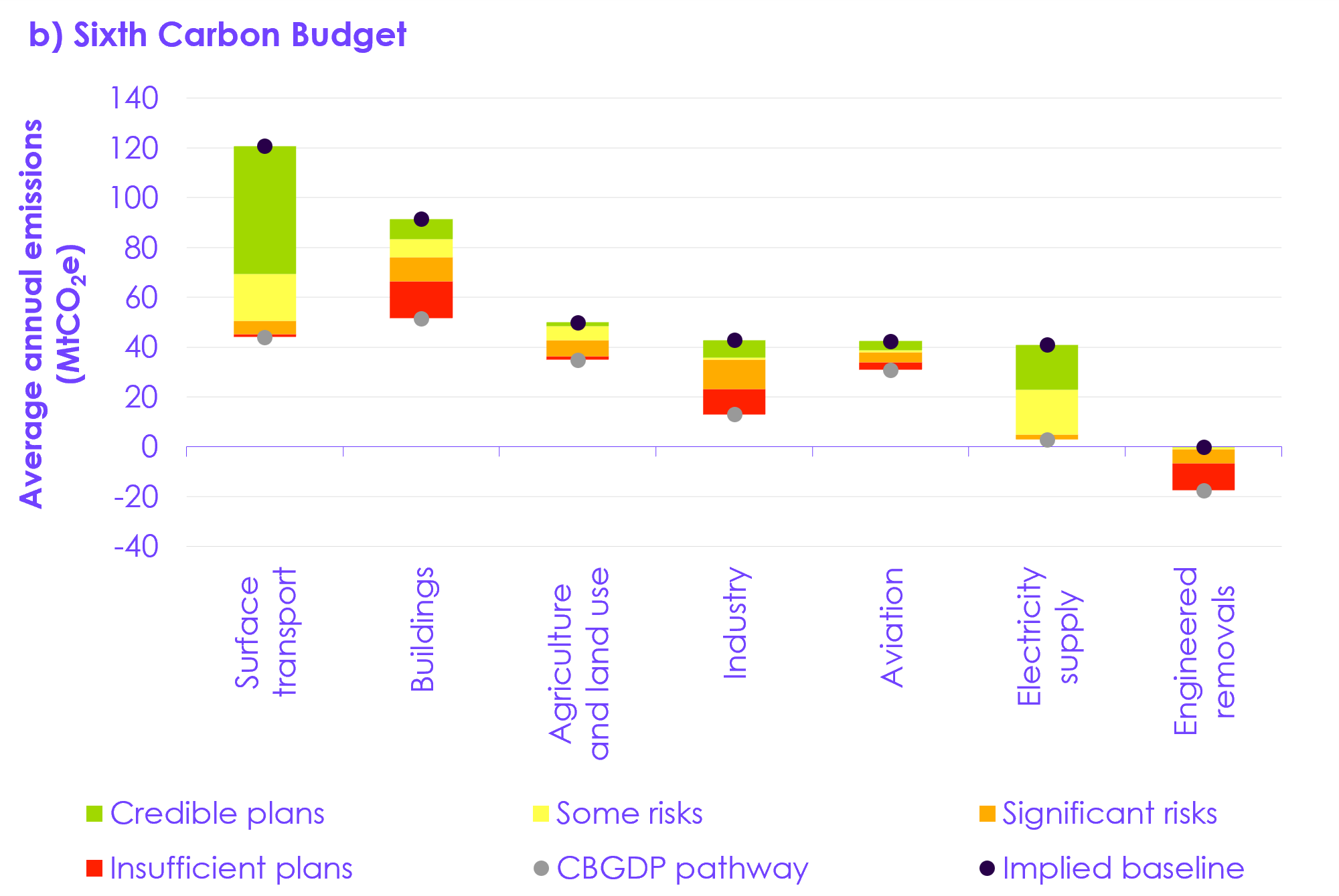

Our assessment is similar for the Sixth Carbon Budget, with around three-fifths of the required emissions reduction covered by credible plans or plans with some risks attached. This represents a slight improvement compared to our assessment last year.

- Unlike for the 2030 NDC, the pathway does achieve the Sixth Carbon Budget. But this is largely achieved through additional measures where we have assessed there to be significant risks or insufficient plans. This means that the proportion of emissions reductions covered by insufficient plans increases significantly to 17% over the Sixth Carbon Budget period. This is partly due to the steep ramp-up in engineered removals in the 2030s, without detail on how to deliver it, and the reliance on international carbon credits to offset international aviation emissions. There are also increasing contributions in industry and buildings.

Progress in key sectors

While the UK continues to make substantial positive progress in decarbonising electricity supply, progress is more mixed in electrifying the three key end-use sectors – surface transport, buildings, and industry. However, in each of these areas, market developments and progress seen either in the UK or internationally give us confidence that progress can be made quickly. Progress is also mixed in the other key sectors of agriculture and land use and aviation. Delivery of engineered removals is a high risk to achieving the carbon budgets.

Surface transport

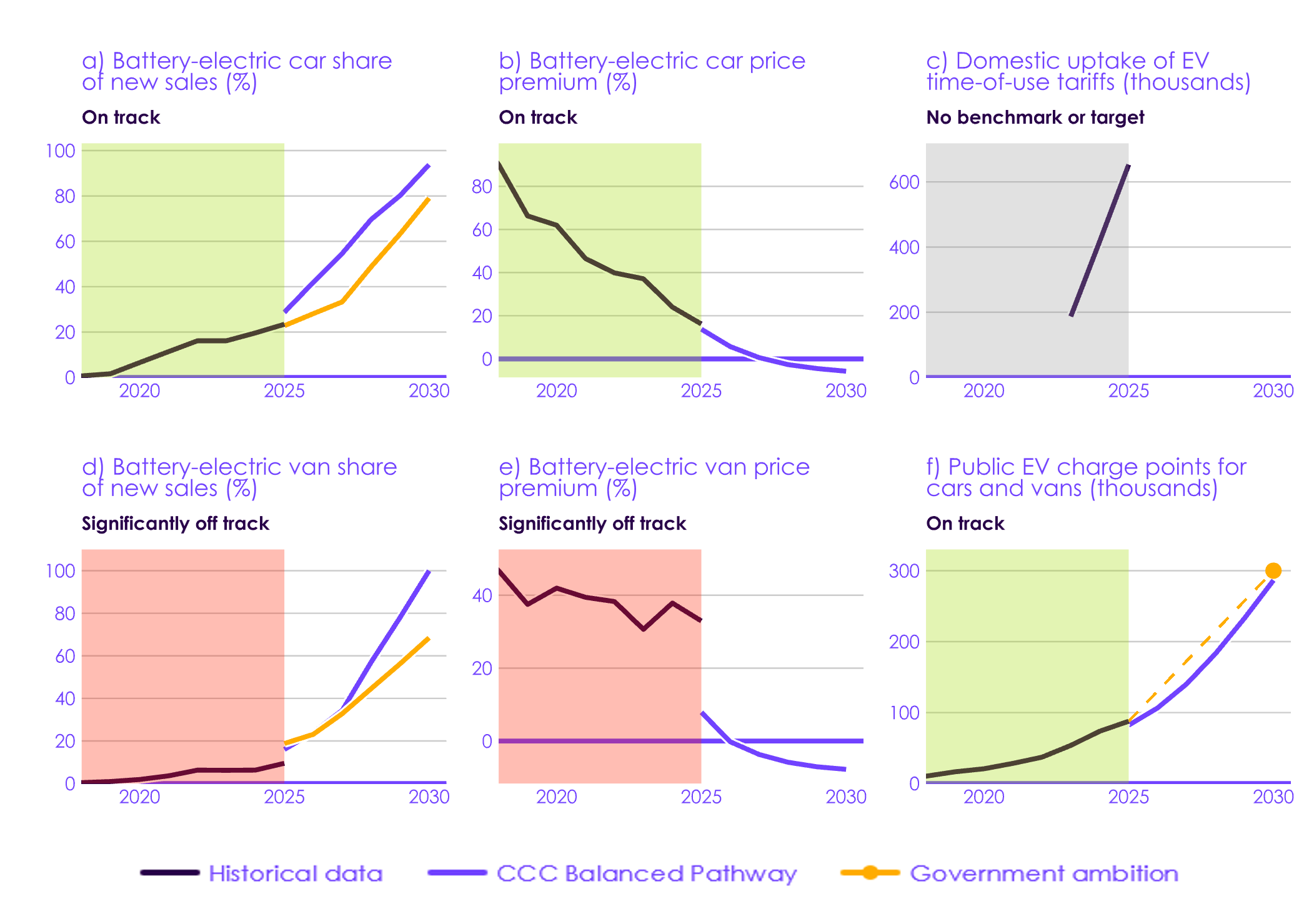

Surface transport remains the UK’s highest emitting sector, and while EV sales are continuing to grow, an acceleration is needed. The ZEV mandate plays a key role in underpinning and reinforcing market developments towards large-scale uptake of EVs and enabling investment in supporting infrastructure. Despite some weakening of incentives, it continues to be effective at increasing the choice and affordability of electric cars on the market, without any manufacturer penalties being incurred. It is essential that this year’s review of the mandate does not lead to further concessions. Doing so would severely undermine prospects of achieving the UK’s 2030 NDC, exacerbate the UK’s dependence on imported oil, and leave more households paying the higher costs of petrol or diesel cars.

- Electric cars: nearly one in four new car sales were EVs in 2025 and the number of EVs on the road increased by 41% in the year to April 2026 – surpassing 2 million for the first time. Sales will need to accelerate fast in the coming years for the UK to get on track to achieve its 2030 NDC. This is possible provided the Government stands firm.

- Underpinned by reducing costs in global supply chains, increasing competition, and the ZEV mandate, the price of EVs continues to fall. The average purchase price premium of an electric car relative to a petrol equivalent reached 16% in 2025, down from 24% the year before. Price parity has been met in certain car segments.

- To support the market continuing to grow, the Government has introduced the Electric Car Grant, providing a discount for qualifying car models under £37,000, and launched the ‘Get that electric feeling’ public engagement campaign, communicating accurate information on the benefits of EVs.

- The Government announced a new three pence per mile tax on EVs effective from April 2028. This is around half the effective rate of tax paid by petrol cars through fuel duty and will not change the fact that – for households which are able to charge at home – EVs offer significant running cost savings. However, this potentially introduces an additional administrative burden and confuses signals to consumers on the benefits of EV ownership. It is essential that this new tax is implemented in a straightforward manner without creating significant additional hassle for consumers.

- Several policy decisions in the past year retain incentives for plug-in hybrids (PHEVs) based on emissions factors which underestimate real-world emissions. These have coincided with PHEVs gaining an increased market share. Providing incentives for emissions savings that PHEVs do not deliver distorts the market and risks eating into the demand for EVs.

- Electric vans: while sales of electric vans grew by more than one-third year-on-year to reach 9.5% of the market in 2025, this remains below the ZEV mandate headline target. Technology development is helping to reduce barriers to electric van adoption, but further action on regulatory reforms and increased charging access is also needed.

- Charge points: there has been continued growth in the number of public charge points, which increased by 19% in 2025 to reach 88,000. The biggest increase has been in ultra-rapid devices and charge points located along the strategic road network. However, public charging costs remain high. The Government plans to allow cross-pavement charging gullies under permitted development rights to widen access to home charging. The Government has also committed to review the cost of public charging – this review must identify further ways to reduce costs for those who rely on local public charge points for their everyday charging.

Buildings

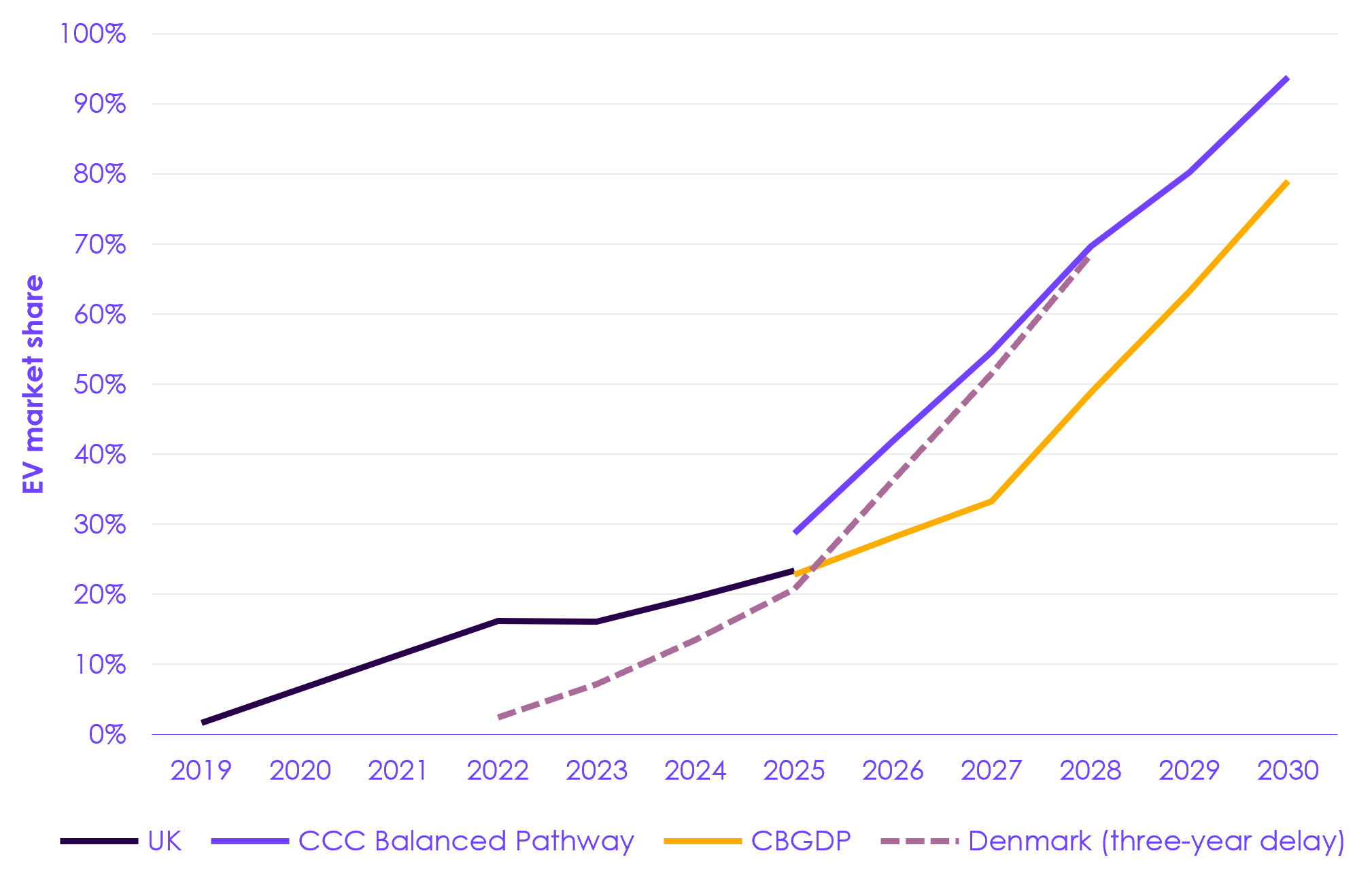

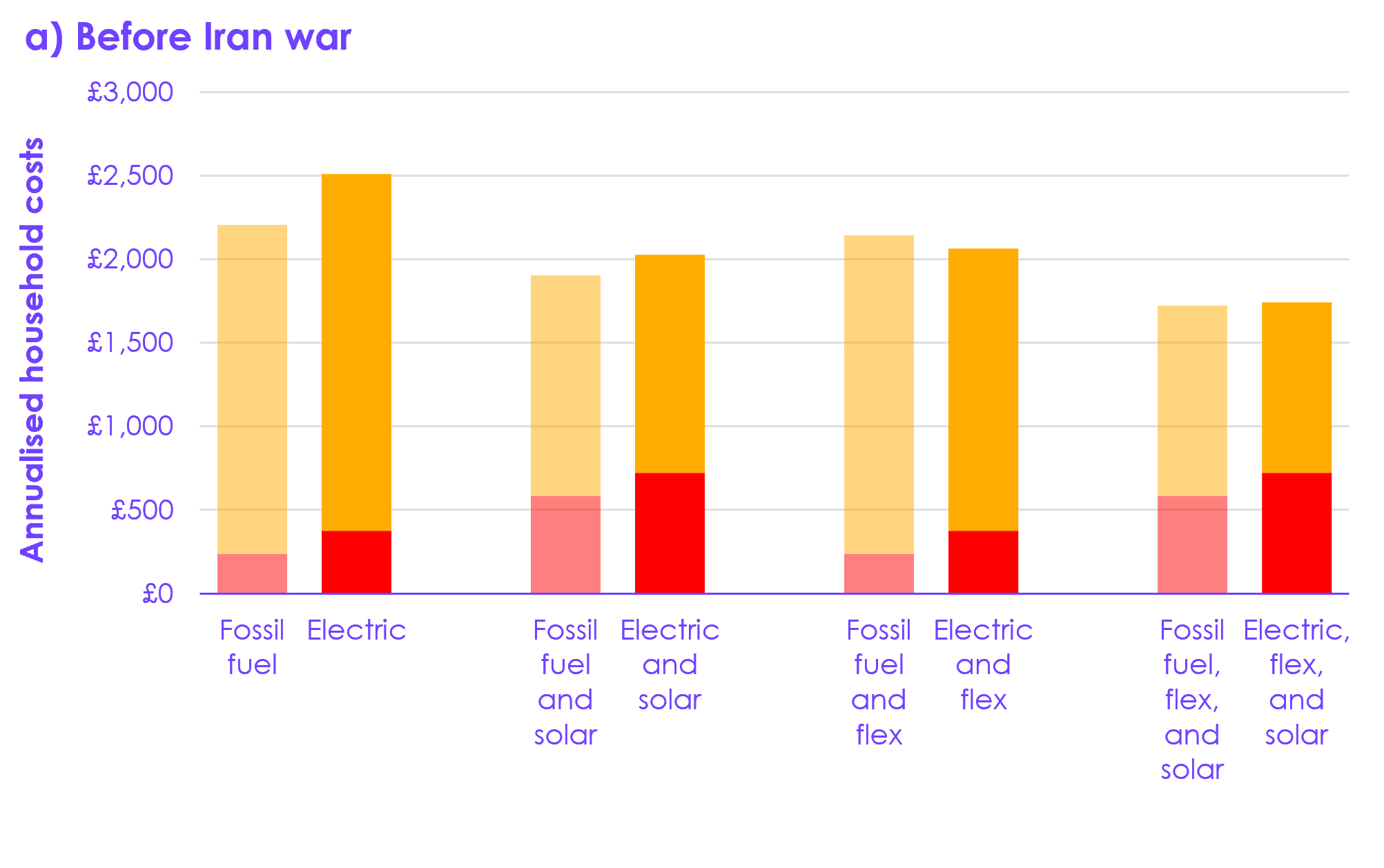

Currently, fewer than 2% of homes are heated with a heat pump in the UK. This is among the lowest in Europe. A low ratio of electricity-to-gas prices is a key enabler supporting households and businesses to switch to heat pumps in many countries (Figure 4).

There has been some positive progress for buildings with the publication of the Warm Homes Plan and the Future Homes Standard. However, plans are insufficient for the scale-up of low-carbon heating installations in existing homes required over the next decade, and growth slowed last year. There remain significant gaps in the market, particularly in public and commercial buildings and in low-income homes following the closure of the ECO scheme.

- Low-carbon heating in existing homes: around 52,000 heat pumps were installed in existing homes in 2025, an increase of 7% compared to 2024. This is a significant slow-down in growth compared to the 56% growth seen the year before.

- The Warm Homes Plan aims for 450,000 heat pump installations per year by 2030, of which around 250,000 are expected to be retrofit. Installation rates will need to be higher than this to deliver the emissions reductions in the CBGDP. While the annual growth rate required to deliver this is significantly higher than that seen in 2025, growth rates seen in other European markets, and in the UK between 2023 and 2024, suggest that higher numbers of installations could be achievable.

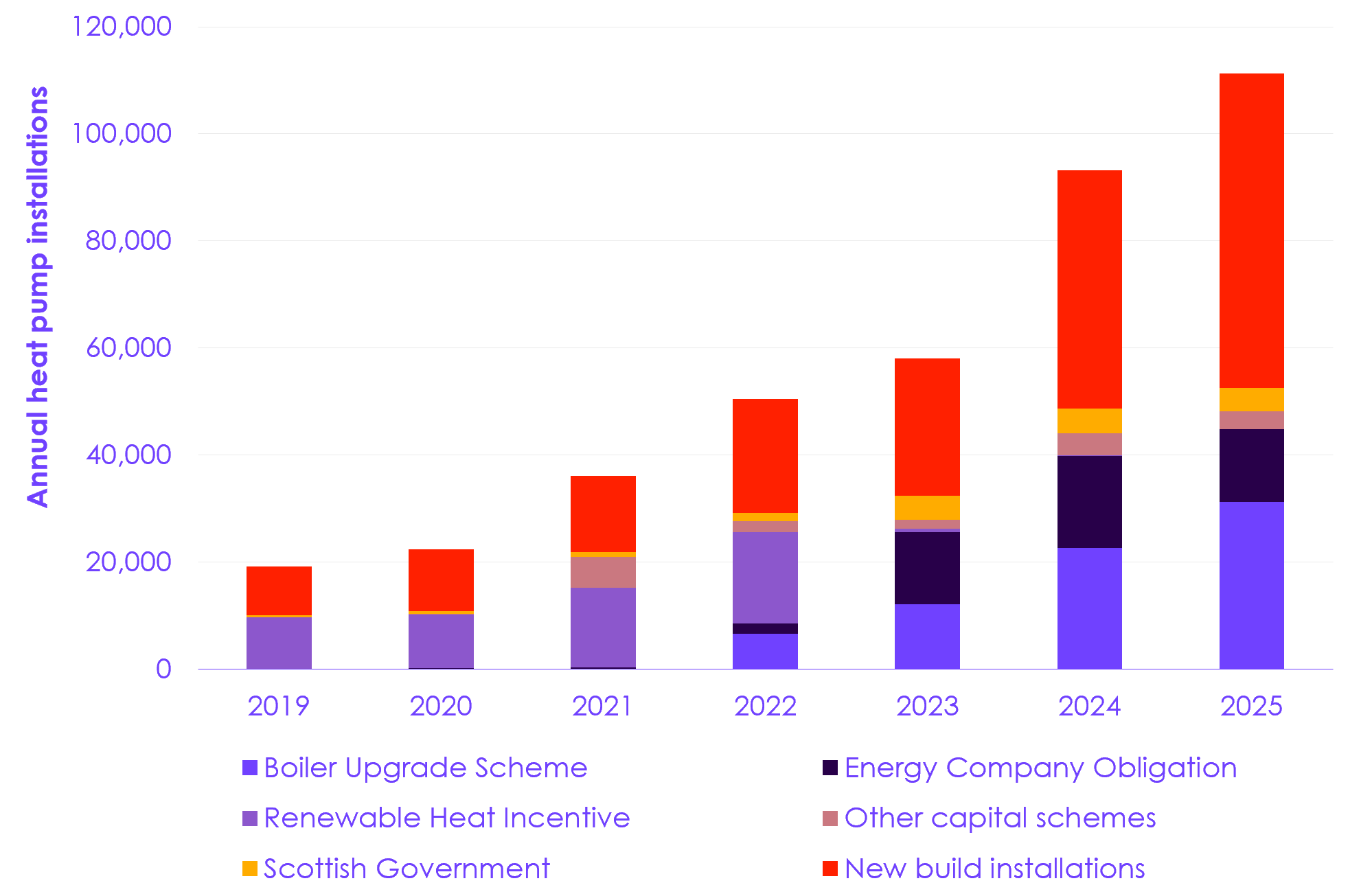

- The Government has closed the ECO scheme, which delivered around one-third of retrofit heat pump installations over the past three years. The slower overall growth in 2025 was driven by a reduction in installations under ECO. While the Warm Homes Plan has committed overall funding of £1 billion per year to support upgrading the homes of low-income households, this is a significant decrease in investment, and the Government is yet to set out details of how this funding will be spent.

- Despite progress in removing some policy costs from electricity bills in the 2025 Budget, the ratio of electricity to gas prices for households remains a major barrier to heat pump uptake. The Warm Homes Plan laid out a vision to promote installation of rooftop solar and batteries alongside a heat pump, as well as uptake of time-of-use energy tariffs, to reduce running costs. While this approach will strengthen incentives for many households by enabling them to access cheaper power, it will not be suitable for all premises. Other key barriers – including upfront costs and non-financial barriers – also remain significant and must be addressed to enable faster heat pump uptake.

- Low-carbon heating in new buildings: in March 2026, the Government announced that regulations have been put in place to implement the Future Homes Standard and Future Buildings Standard. This requires all new buildings in England and Wales to be constructed with low-carbon heating, with regulations coming into force in 2027, subject to a 12-month transition period. Despite delays, this is a positive step forward that will soon ensure that no new buildings are being constructed with fossil fuel heating systems.

- Low-carbon heating in existing public and commercial buildings: the Government has announced the closure of the Public Sector Decarbonisation Scheme, which means that there is now no dedicated funding for the decarbonisation of the public estate. In addition, there has been no action to address the electricity-to-gas price ratio for non-residential users, and no plans have been put in place for incentivising decarbonisation in commercial buildings.

Industry

There has been good progress in specific areas of industry, but the route to electrification of industrial heat remains unclear for large parts of the market. The Government has set the intention to make electrification the economically rational choice for a wider range of businesses – it urgently needs a plan to deliver on this ambition for competitive, electrified industries. This requires clarity on which industrial use cases electrification is deemed suitable for, and an assessment of the commercial conditions needed to deliver those.

- Industrial electrification: while work to electrify the Port Talbot steelworks is underway, there is no evidence of progress on widespread electrification of industrial heat.

- High electricity prices relative to gas remain a major barrier, with industrial electricity-to-gas price ratios still above 4:1 for many large users. Schemes such as the Supercharger programme reduce this ratio to just above 2:1 for around 500 energy-intensive businesses, with broader reforms for a larger number of manufacturers expected to reduce ratios to around 3.5:1 by 2027. However, it is unclear whether this will be sufficient to drive electrification at scale.

- Carbon capture and storage (CCS): positive steps include £9.4 billion of funding allocated for CCS at the 2025 Spending Review, final investment decision being reached for the first CO2 capture facility at a UK manufacturing site, and the construction of CO2 transport and storage infrastructure starting at both Track-1 clusters. However, uncertainty remains beyond these initial projects.

Electricity supply

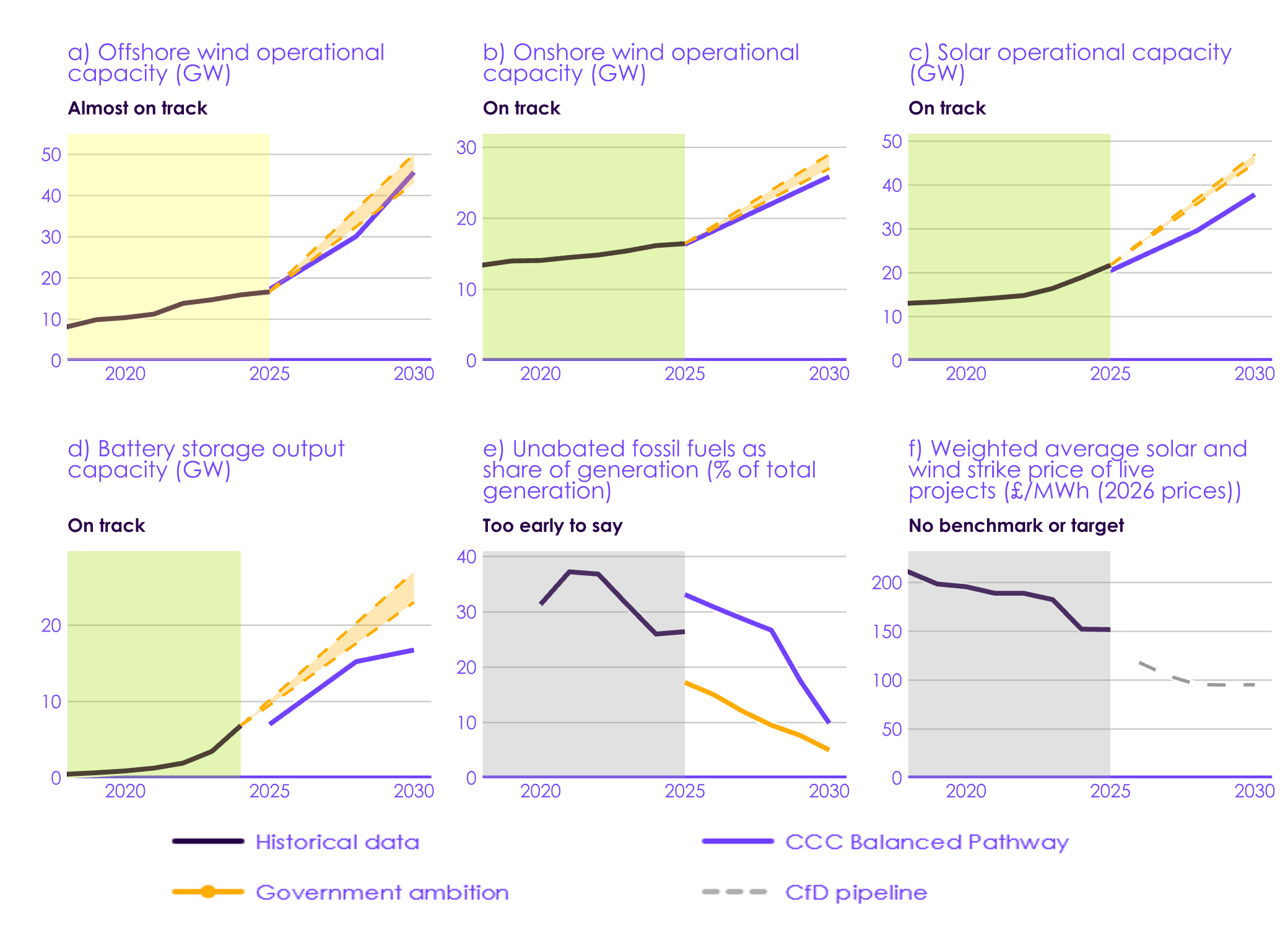

There has been positive progress in the electricity supply sector over the past year, with record amounts of renewable generation contracted. Important steps have been taken to remove planning barriers and reform the grid connections process. The UK is firmly on a path to a very low-carbon electricity system by the start of the Sixth Carbon Budget period. However, there are policy risks to decarbonising electricity supply rapidly enough to achieve the 2030 NDC. These include ensuring sufficient renewable capacity and timely and cost-effective transmission network build. Effective use of system flexibility (including through the successful implementation of Market-wide Half Hourly Settlement reform) is critical for efficient markets and networks, and has potential to offer some contingency against delays.

- Offshore wind: in 2025, 0.7 GW of new offshore wind capacity was added, bringing total UK capacity to 16.6 GW. The existing pipeline of contracted projects, including the record 8.4 GW contracted in the Contracts for Difference Allocation Round Seven (AR7), is expected to see this capacity more than double to around 37 GW. Further additions will be needed to achieve the Government’s stretching goals for offshore wind. If delivery times cannot be shortened to meet these goals, additional generation capacity from other technologies will need to accelerate to help make up for the shortfall in low-carbon generation required to achieve the Government’s targets.

- Onshore wind: 0.3 GW of new onshore wind capacity was added in 2025, bringing total UK capacity to 16.4 GW. Average annual deployment of between 2.1–2.5 GW will be required up to the end of the decade to meet the Government’s ambition.

- Solar PV: 2.8 GW of solar PV capacity was added in 2025, bringing the total to 21.7 GW. This was the highest annual solar PV deployment since 2015 and represented the third successive year of strong growth. Average annual deployment will need to increase to around 5 GW up to the end of the decade to achieve the Government’s ambition. There is a strong pipeline of upcoming large-scale solar projects, with 4.9 GW contracted in AR7.

- The Government’s ambition to triple the number of homes with rooftop solar panels by 2030 would represent a significant step change in small-scale deployment. If realised, this would contribute around 50% of the total cumulative deployment needed to meet its ambitions for overall solar PV capacity in 2030.

- Network and storage infrastructure: expanding and modernising electricity networks, ensuring they are resilient to future climate change, and deploying storage are key to electricity supply decarbonisation and wider electrification. Progress has been made, including new funding settlements for transmission networks and reforms to the connections queue, alongside a record 2 GW of new grid-connected battery storage estimated as being installed in 2025. The National Electricity System Operator needs to make faster progress in optimising the utilisation of the cheapest and cleanest available resources.

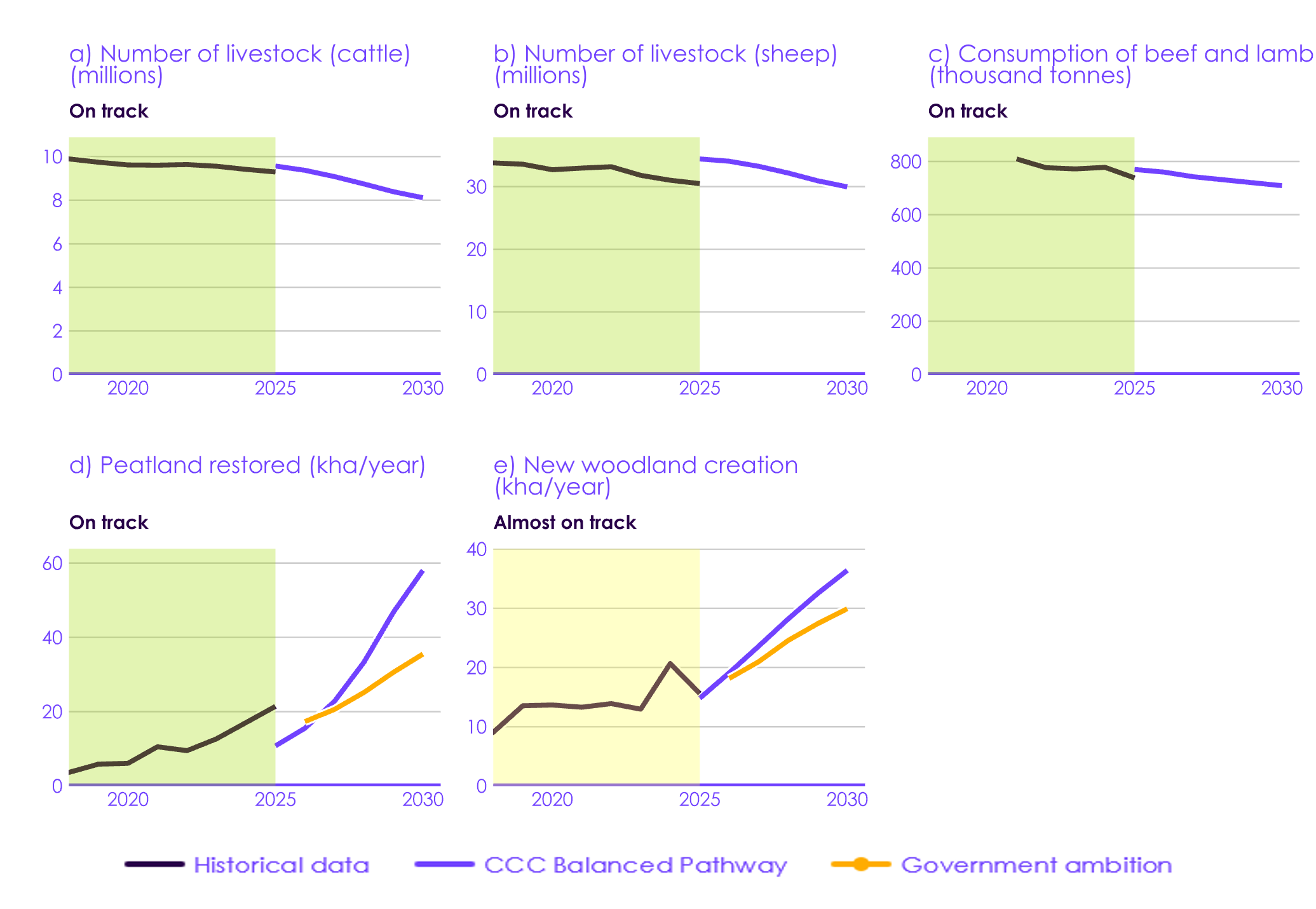

Agriculture and land use

There has been some progress in key indicators for agriculture and land use, with several trends moving in the right direction. Further action will be needed to sustain delivery and close remaining gaps, building on the land use frameworks which now exist in England, Scotland, and Wales. Further action must also be mindful of the changing climate to ensure that measures can deliver for climate adaptation as well as mitigation.

- Livestock numbers and agricultural emissions: cattle and sheep numbers fell by 1% and 2% respectively in 2025, continuing a longer-term trend and reaching their lowest levels since 1990.

- Household beef and lamb purchases fell by 5% in 2025, with a longer-term reduction of 9% since 2021, likely driven by high beef and lamb prices and cost-of-living pressures.

- The Sustainable Farming Incentive in England is to be reopened in June 2026, and the 25-year Farming Roadmap is expected to be published this year. Along with various other new funding streams, these present an opportunity to incentivise farmers to diversify actions needed for emissions reduction, while producing food in a sustainable and resilient manner.

- Peatland restoration: there has been strong progress in restoring peatlands, with around 21,400 hectares restored in 2025. This is a 26% increase on the previous year and roughly three times the level in 2020. All UK nations currently have grant funding for peatland restoration in place until at least 2027.

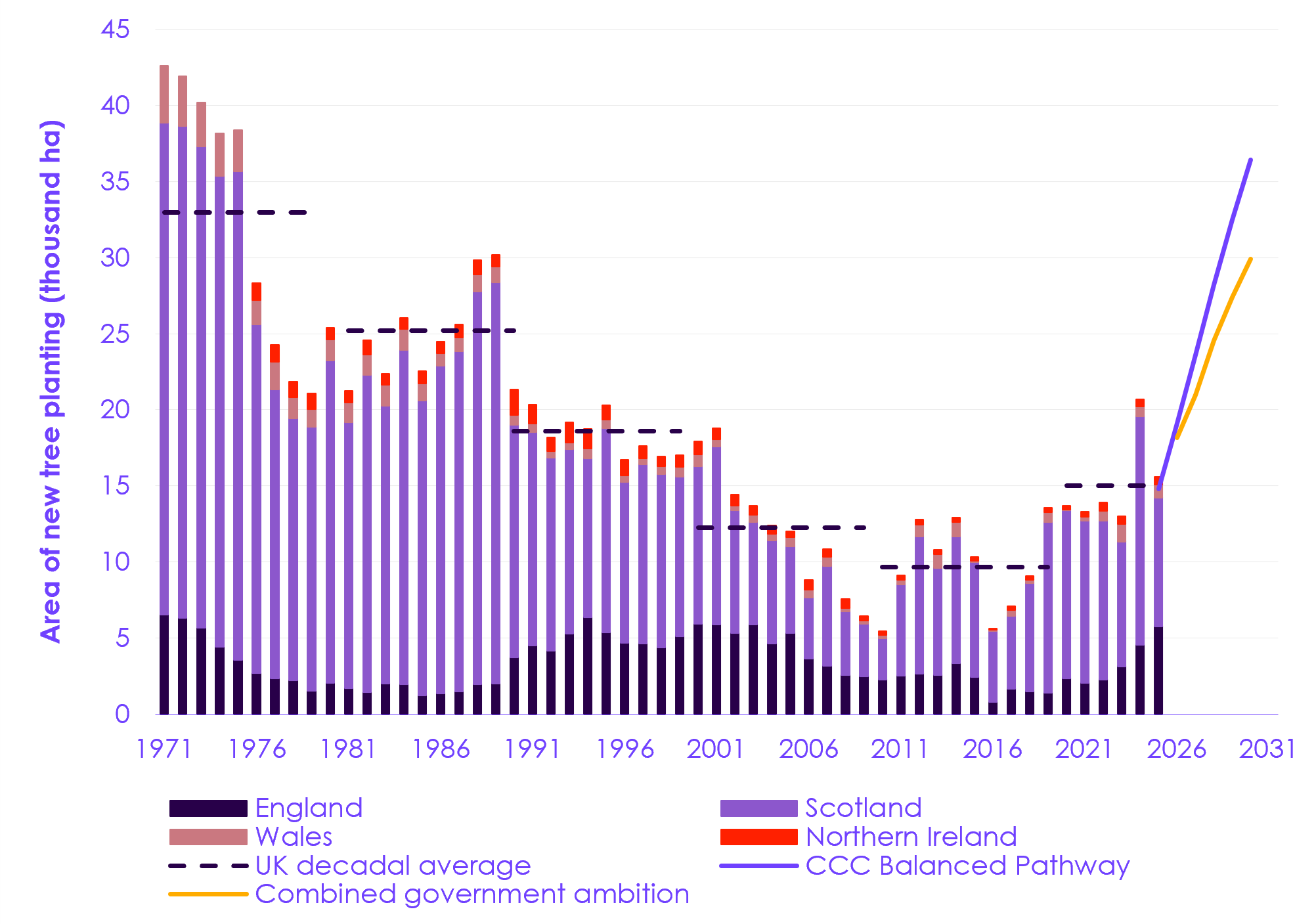

- Woodland creation: progress on woodland creation is more mixed, with planting rates falling by 25% in 2024/25, following a significant increase the year before. This reduction was driven by funding cuts in Scotland, which continues to lead in the establishment of new woodlands for the UK, planting more than half of the total in 2024/25. Planting rates have increased in England, and a new plan setting out Defra’s approach to woodland creation is expected this year.

Aviation

There has been mixed progress in reducing emissions from aviation. Policy development has strengthened confidence in the delivery of SAF, but the inclusion of international credits in the Government’s plan to meet the Sixth Carbon Budget puts the sector’s emissions reductions at increased risk. Further action will be needed to ensure that international aviation emissions reduce in line with the CBGDP, and contingency plans should be developed to mitigate the risks the sector faces, including on demand management.

- Emissions and demand: it is positive that the high emissions growth rate observed between 2022 and 2024 has slowed down, with emissions decreasing slightly in 2025 despite a 3% increase in passenger-kilometres. However, it is too early to say whether aviation emissions will grow, plateau, or decrease in the future.

- Sustainable aviation fuel: achievement of the SAF mandate in 2025 and implementation of the Sustainable Aviation Fuel Act (2026), which will enable a SAF revenue certainty mechanism, represent positive progress towards ensuring SAF incentivisation and delivery. However, significant challenges remain around scaling up supply, particularly for second-generation biofuels and third-generation power-to-liquid fuels, which must begin to contribute from 2027 and 2028 respectively.

- Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) credits: the Government’s pathway includes the use of international carbon credits under CORSIA to achieve emissions targets in the Sixth Carbon Budget period for the first time. This introduces significant risk, including uncertainty over the availability and quality of high-integrity credits.

Engineered removals

The Government’s CBGDP pathway relies on a steep scale-up of engineered removals in the Sixth Carbon Budget period. There has been progress through the finalisation of the Greenhouse Gas Removals Business Model, confirmation of plans to integrate engineered removals into the UK Emissions Trading Scheme, and the first engineered removals project reaching final investment decision. The independent Whitehead Review also set out recommendations to accelerate deployment. However, considerable risks remain, including a lack of clarity on long-term funding. Given the high reliance on engineered removals in the Government’s plan, it is essential that the Government develops a strategy for how these will be delivered and how progress will be monitored, with sufficient contingency plans put in place for any shortfall.

Conclusion

The UK can hit its upcoming emissions reduction targets, and remain on track for Net Zero, while simultaneously increasing energy security and protecting households and businesses from volatile energy prices – but only with urgent further policy action. With a significant gap between the Government’s plan and the 2030 NDC, the coming year is absolutely crucial for the next phase of the transition. If sufficient progress on electrification is not made in the next year, the 2030 NDC may become out of reach and there would be significant risks for both the Sixth Carbon Budget and reaching Net Zero by 2050.

The rest of this report is set out in five chapters:

- Progress in reducing UK emissions.

- The Carbon Budget and Growth Delivery Plan.

- Indicators of current delivery progress.

- Assessment of policy progress.

- Household costs and savings.

We list our priority recommendations to the UK Government, the Northern Ireland Executive, and the Welsh Government in Annex 1.[2] We set out our policy assessment criteria in Annex 2.

Chapter 1: Progress in reducing UK emissions

In this chapter, we review emissions data based on final 2024 data and provisional 2025 data and look at drivers for trends. We also review the international context for UK action.

Our key messages are:

- UK greenhouse gas (GHG) emissions: emissions were 407 MtCO2e in 2025, including the UK’s share of international aviation and shipping (IAS).

- Emissions are now 50% below 1990 levels. There has been a long-term trend of emissions reductions in electricity supply, which has historically driven progress.

- It is now highly likely that the Fourth Carbon Budget (2023 to 2027) will be achieved. Over 2026 and 2027, average annual emissions excluding IAS must be below 413 MtCO2e to achieve the Fourth Carbon Budget; emissions in 2025 were 11% lower than this.

- Change from 2024 to 2025: emissions fell by 1.8% (7.3 MtCO2e) compared to 2024, marking the eleventh consecutive year of reductions, not counting the COVID-19 pandemic years.

- Despite driving progress historically, electricity supply emissions did not fall in 2025. While emissions from coal fell to zero, gas generation rose slightly – driven by a combination of factors, including a fall in net imports of electricity and nuclear outages.

- Emissions in surface transport increased by 2.7% in 2025 according to provisional estimates. The incremental progress in the roll-out of electric vehicles (EVs) from year-to-year is likely to have been offset by other factors such as increased vehicle-kilometres. However, the impact of EVs is apparent in longer-term trends – despite car-kilometres having almost returned to 2019 levels, car emissions are 12% lower than in 2019. Around half of this reduction is likely due to the uptake of EVs.

- Economy wide, emissions continued to fall due to reductions in industry (a large part of which was the closure of the blast furnaces ahead of electrification at Port Talbot), fuel supply, and buildings, despite colder winter months than the year before.

- Emissions in Scotland, Wales, and Northern Ireland: emissions fell in Scotland and Wales but were mostly unchanged in Northern Ireland in 2024. Reductions in Wales were significant, due to the closure of the Port Talbot blast furnaces ahead of electrification.

- Climate change in the UK: the rate of global warming is now at a record high, and the UK is already experiencing the impacts. Heatwaves have become hotter, longer, and more frequent. Early 2026 was exceptionally wet in parts of the UK, with long unbroken spells of rain leading to widespread flooding. In its report on A Well-Adapted UK, the Climate Change Committee’s (CCC) Adaptation Committee offers advice on potential solutions to address these risks.

- International progress: in a volatile geopolitical context, the UK remains among a leading group of countries demonstrating sustained decarbonisation ambition and delivery. Alongside the UK, many economies, including the European Union (EU), India, Japan, the Philippines, and Turkey, are responding to the Iran war with plans which will accelerate the transition away from fossil fuels.

1.1 UK territorial emissions

1.1.1 Overall UK emissions

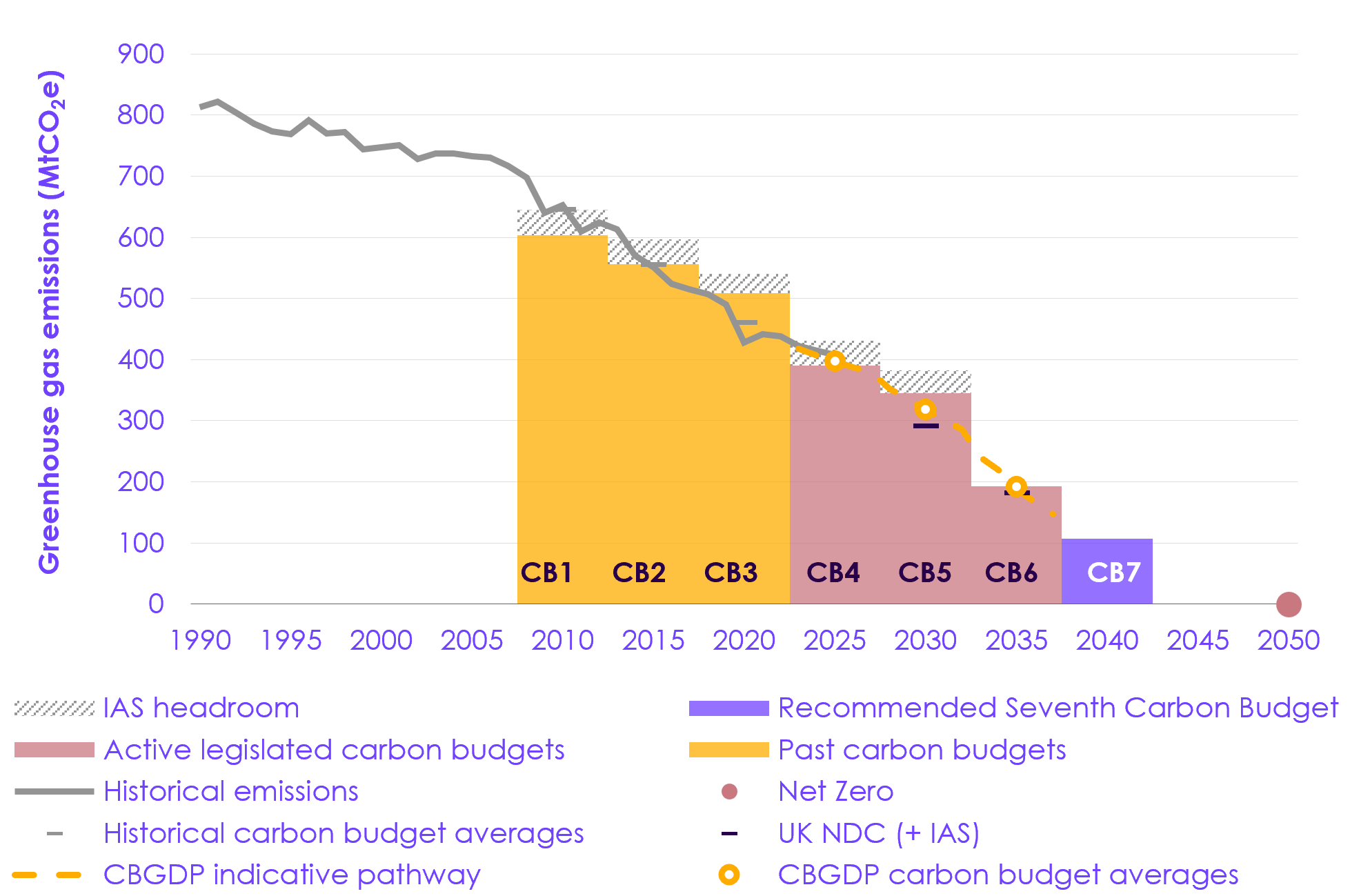

Total greenhouse gas emissions in the UK have been falling steadily since 1990 (Figure 1.1). Including its share of emissions from international aviation and shipping (IAS), which will count towards the Sixth Carbon Budget and later carbon budgets following legislation being laid in Parliament in 2026, the UK is now halfway to Net Zero emissions (see Table 1.1).

The UK has achieved its first three carbon budgets, and emissions reductions are on track to achieve the Fourth Carbon Budget. Progress in policy towards later carbon budgets, which are entirely in the future, is discussed in Chapter 4.

Final emissions in 2024

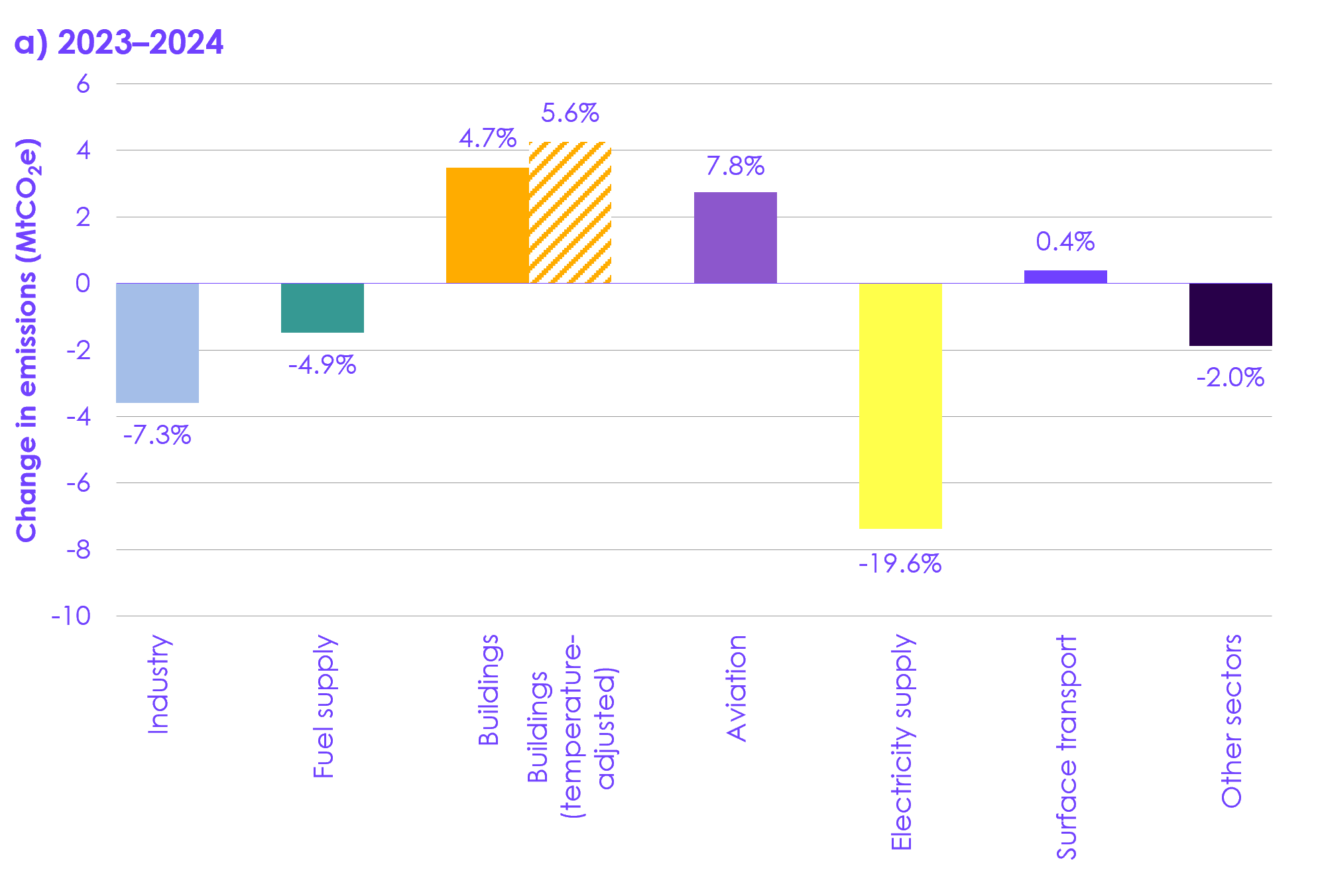

Final emissions for 2024 were 415 MtCO2e including IAS, which is 49% below 1990 levels.[3];[4] This is a 7.7 MtCO2e (-1.8%) change from 2023.

The change between 2023 and 2024 was driven by the electricity supply and industry sectors (Figure 1.2a).

- Electricity supply showed the largest sectoral emissions reduction, accounting for a decrease of 7.4 MtCO2e (19.6%). This was driven primarily by a 14.4 TWh reduction in gas generation year-on-year, as well as a 1.7 TWh reduction in coal generation.

- Industry accounted for a decrease of 3.6 MtCO2e (7.3%). This was predominantly due to the temporary closure of Port Talbot steelworks, while an electric arc furnace is being built for low-carbon steelmaking.

- These reductions were partly offset by increases in other sectors, such as buildings, whose emissions increased by 3.5 MtCO2e (4.7%), and aviation, whose emissions increased by 2.7 MtCO2e (7.8%).

Provisional emissions in 2025

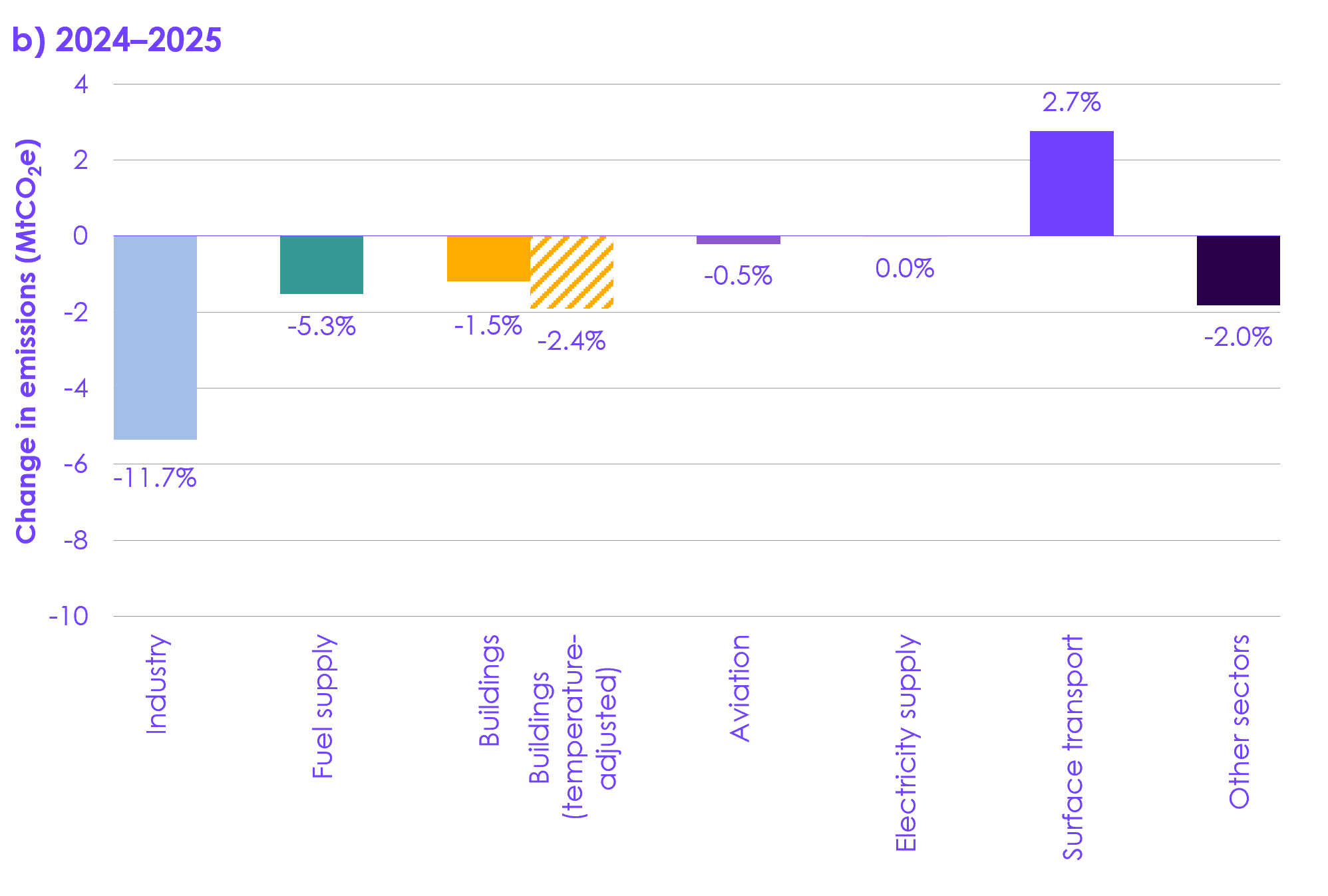

Provisional emissions for 2025 were 407 MtCO2e, including IAS, which is 50% lower than 1990.[5] This is a 7.3 MtCO2e (-1.8%) change from 2024. Excluding IAS, emissions were 366.6 MtCO2e, which is 54% lower than 1990. This is a 6.8 MtCO2e (-1.8%) change from 2024.

The main driver of the reduction between 2024 and 2025 was a 5.4 MtCO2e (12%) fall in emissions in the industry sector, with significant contributions from fuel supply and buildings, the latter being despite colder winter months in 2025 than the year before (Figure 1.2b). In contrast, emissions in surface transport increased by 2.8 MtCO2e (2.7%) in 2025. The drivers of these changes are given in the following sections.

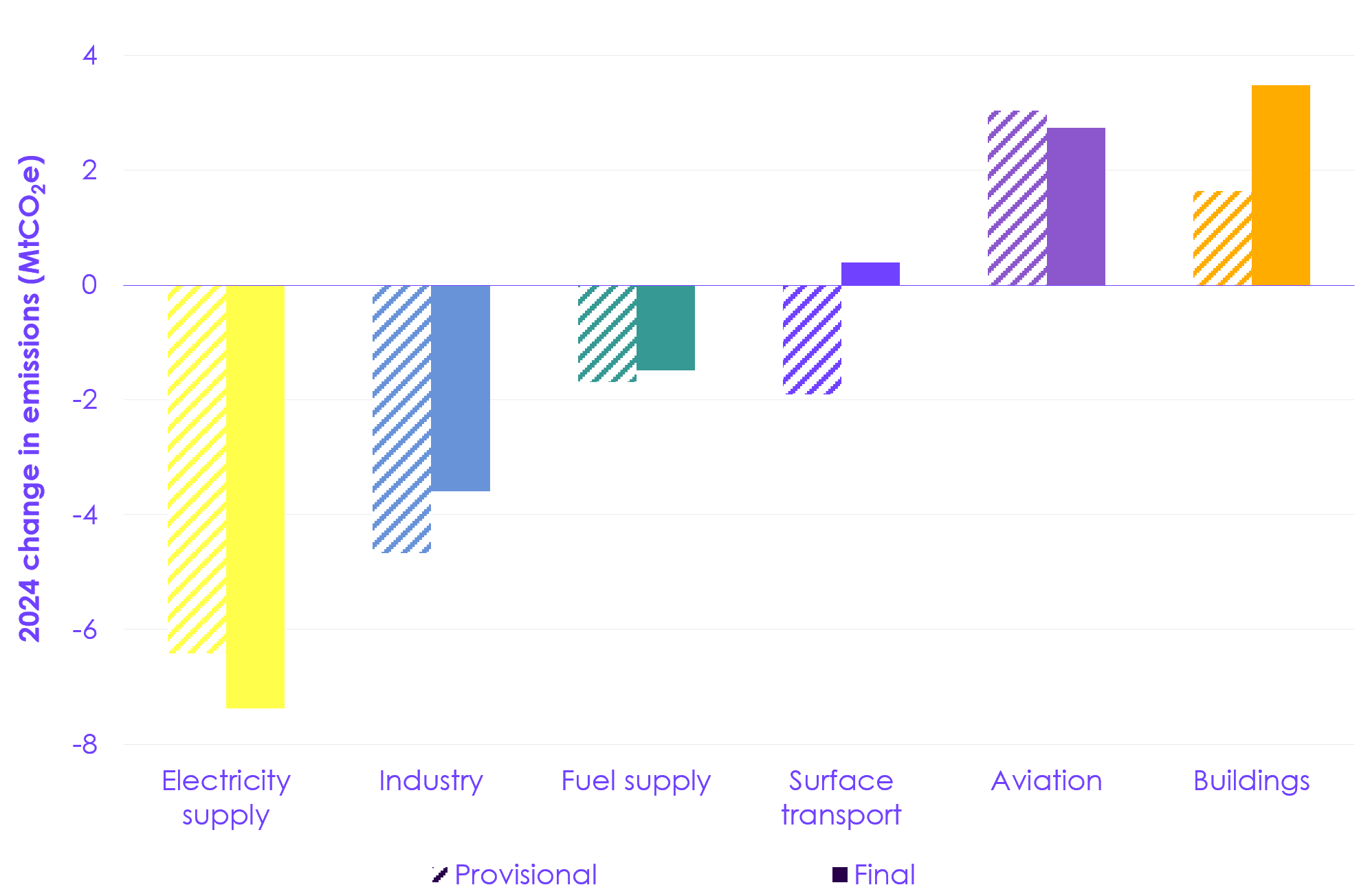

Total provisional emissions estimates have varied from final estimates by up to 2% in recent years (although the differences are generally much less than this). This has a small impact on our findings on overall emissions but can affect conclusions on year-to-year changes. Figure 1.3 shows the changes in emissions between 2023 and 2024 for key sectors, according to the provisional and final emissions estimates.

Emissions over the Fourth Carbon Budget period

It is now highly likely that the Fourth Carbon Budget will be achieved. The Fourth Carbon Budget is 1,950 MtCO2e, of which 1,124 MtCO2e has been used up in 2023 to 2025. This leaves an average annual amount of 413 MtCO2e for the remaining two years. Provisional 2025 emissions (excluding IAS, as the Fourth Carbon Budget excludes IAS) are already 11% lower than this.

| Table 1.1 UK territorial emissions and emissions changes for selected periods |

|||

|---|---|---|---|

| Period | Including IAS | Excluding IAS | |

| Emissions (MtCO2e) | 1990 | 815 | 793 |

| 2008 | 697 | 653 | |

| 2023 | 422 | 384 | |

| 2024 | 415 | 373 | |

| 2025 | 407 | 367 | |

| Reduction in emissions (MtCO2e, %) | 1990–2025 | 408 (50%) | 427 (54%) |

| 2008–2025 | 290 (42%) | 286 (44%) | |

| 2023–2024 | 7.7 (1.8%) | 11 (2.7%) | |

| 2024–2025 | 7.3 (1.8%) | 6.8 (1.8%) | |

| Annual average reduction (MtCO2e, %) | 1990–2025 | 13 (2.0%) | 12 (2.2%) |

| 2008–2025 | 17 (3.1%) | 17 (3.3%) | |

| Source: Department for Energy Security and Net Zero (DESNZ) (2026) Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; CCC analysis. Notes: ‘IAS’ refers to the UK’s share of emissions from international aviation and shipping. |

|||

| Figure 1.1 The UK’s historical emissions and targets |

Description: UK emissions have halved since 1990, and the UK achieved its first three carbon budgets. Source: Department for Energy Security and Net Zero (DESNZ) (2026) Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024. Notes: (1) Emissions from international aviation and shipping (IAS) are included in historical emissions. (2) ‘CB’ refers to the UK’s carbon budget. ‘CB1’ refers to the First Carbon Budget; subsequent numbers refer to subsequent carbon budgets. |

| Figure 1.2 Changes in UK emissions across key sectors |

Description: The main reductions in emissions in 2025 were in industry (by 12%) and buildings (by 1.5%). However, emissions from surface transport increased (by 2.7%). Description: The main reductions in emissions in 2025 were in industry (by 12%) and buildings (by 1.5%). However, emissions from surface transport increased (by 2.7%).Source: DESNZ (2026)Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; CCC analysis. Notes: The columns in these charts show the MtCO2e change between years for each sector. The labels present these as the corresponding year-on-year percentage change. |

| Figure 1.3 Provisional and final changes in emissions between 2023 and 2024 for key sectors |

Description: Provisional emissions are uncertain and are subject to change across all sectors. Source: DESNZ (2026) Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; DESNZ (2025) Provisional UK greenhouse gas emissions statistics: 2024; CCC analysis. Notes: Provisional emissions estimates are calculated based on latest quarterly energy statistics to give an early indication of emissions estimates for the most recent year. Because there is limited data available on a quarterly basis for emissions not related to energy use, provisional estimates of other emissions are based on a simplified approach. With more data available, more accurate estimates are possible in the final statistics. |

1.1.2 Sectoral emissions trends

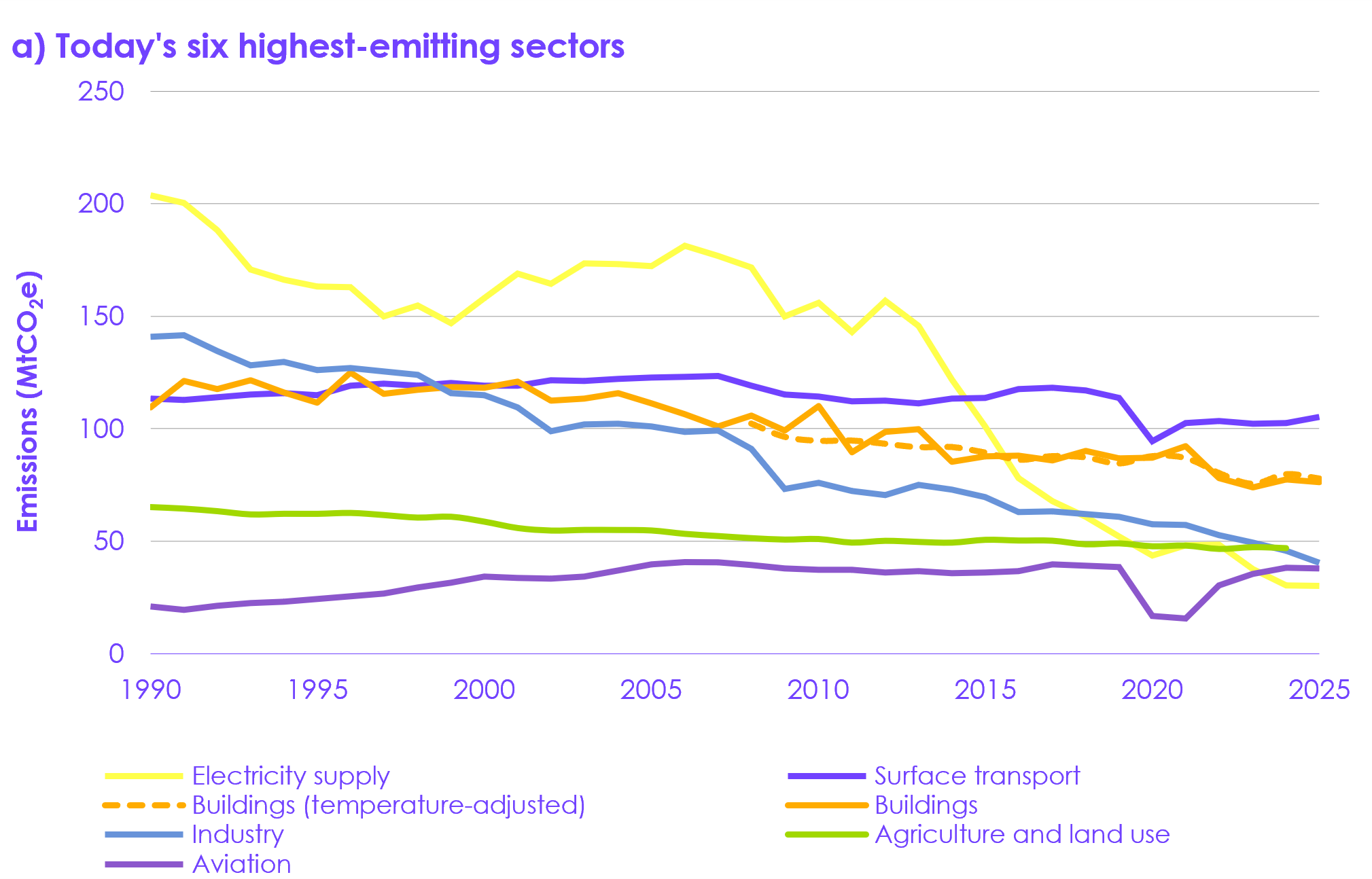

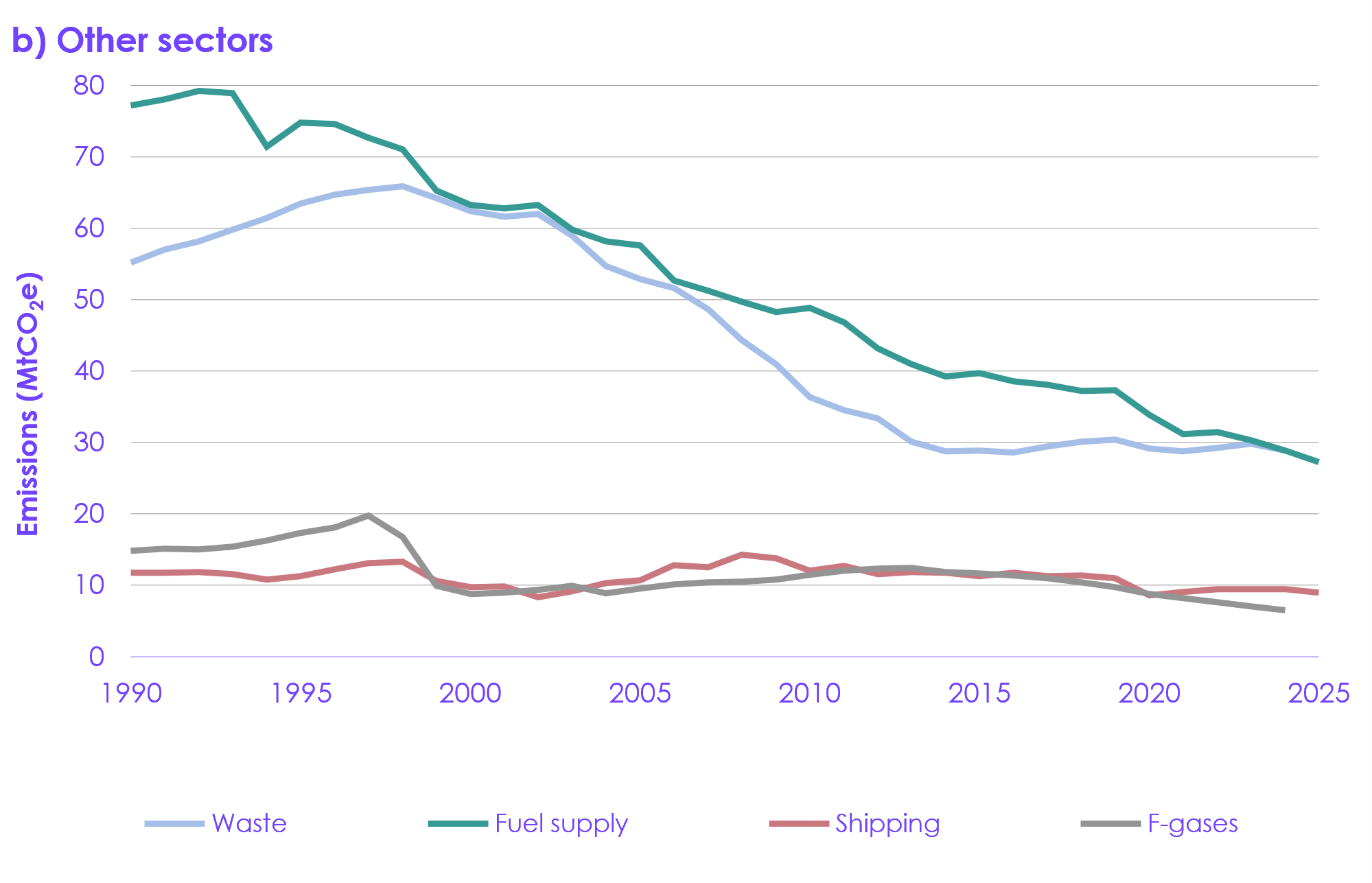

In this section, we discuss recent and longer-term trends in emissions, and the main factors driving these, in key sectors (Figure 1.4). Reductions in emissions since 1990 have been predominantly driven by the electricity supply, industry, fuel supply, and waste sectors. The subset of sectors discussed in more detail below are the most significant for understanding recent overall changes in emissions.

| Figure 1.4 UK emissions by sector since 1990 |

Description: Reductions in emissions since 1990 have been predominantly driven by the electricity supply, industry, fuel supply, and waste sectors. Source: DESNZ (2026) Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; CCC analysis. Notes: (1) The land use sector is a combination of positive sources of emissions and negative sinks of emissions. (2) Agriculture, waste, F-gases, and land use emissions are only shown up to 2024 because the provisional 2025 estimates for these sectors are mostly derived from projections rather than real-world data. |

Surface transport

Surface transport emissions increased by 2.8 MtCO2e (2.7%) in 2025 compared to 2024 levels, reflecting higher total demand for petrol and diesel. While emissions increased in 2025, emissions in the sector are now 12% lower than 2008 levels and 7.3% lower than 2019 levels despite total vehicle-kilometres (km) reaching pre-pandemic levels.

- Surface transport emissions rose since 2024 despite growing EV sales. Growing car- and van-km have increased emissions. This is supported by data showing an increase in demand for petrol and diesel.

- While there is some uncertainty around the provisional emissions data, it appears as though the continued growth in EV adoption has not yet led to an overall reduction in emissions in the surface transport sector compared to 2024. Differences of up to 2.1 MtCO2e have been seen between provisional and final surface transport emissions in recent years, which can affect conclusions on year-on-year emissions changes. For example, according to 2024 provisional data, surface transport emissions fell compared to 2023, but the final data showed them to have risen slightly (Figure 1.3).

- We expect the additional sales of EV cars and vans each year to be reducing emissions by about 0.9 MtCO2e year-on-year currently. This remains within the margin of error between provisional and final emissions data until EV uptake accelerates.

- Total vehicle-km for all vehicle types have reached 2019 levels for the first time since the pandemic due to rising van-km, yet provisional emissions for 2025 were 7.3% lower than 2019.

- Provisional 2025 emissions for cars alone were 12% lower than 2019 levels, despite car-km being 0.2% below 2019 levels. We estimate that the uptake of EVs is likely responsible for around half of this reduction in emissions.

- With sales growing year-on-year, the number of EVs in the fleet is increasing quickly (see Section 3.2.2). As a result, we expect the emissions reductions from EVs to increase quickly in future years.

Buildings

Emissions from the buildings sector fell by 1.2 MtCO2e in 2025. This represents a reduction of 1.3% for non-residential and 1.6% for residential buildings compared to 2024. This was despite the winter months of 2025 being colder overall than in 2024. Emissions in the sector are now 28% lower than 2008 levels. When accounting for the impact of temperature, emissions from the buildings sector fell by 1.9 MtCO2e (2.4%).

- Lower temperature-adjusted emissions (for example, accounting for colder winter months), suggests that factors other than weather were driving this reduction. For example, higher energy prices reducing energy demand by making heating less affordable. While this has caused emissions to fall it does not indicate progress on decarbonising home heating.

- Heat pump deployment is not yet fast enough to meaningfully reduce emissions. Around 50,000 heat pump retrofits were installed per year in 2024 and 2025. However, these would only deliver around an additional 0.1 MtCO2e of emissions savings in 2025.

- Emissions in non-residential buildings fell at a similar rate across both commercial and public sector buildings.

Without further actions to decarbonise buildings it is likely that emissions will rebound if energy prices fall or weather conditions revert to average, as despite having colder winter months than 2024, 2025 was a warmer than average year.

Agriculture and land use

Emissions from agriculture fell by 0.4 MtCO2e to 46.5 MtCO2e in 2024 compared to the previous year. Land use emissions remained the same during this period, remaining a net source of emissions of 0.3 MtCO2e in 2024.[6]

Between 2008 and 2022, total GHG emissions from agriculture fell by 8%, largely driven by a fall in CO2 emissions. Methane emissions contributed less to the reduction in this period with cattle and sheep numbers falling by 1%. Between 2022 and 2024, a steeper 6% reduction in livestock numbers saw methane emissions fall by 4%. However, a significant increase in CO2 emissions led to a small net increase of 0.2% in total GHG emissions from agriculture during this period.

Emissions from land use have fallen by 0.6 MtCO2e since 2008. Emissions declined between 2008 and 2015, becoming a net sink until 2022. Since then, emissions have risen, driven by a smaller forestry sink due to an aging woodland profile and removal of trees for habitat restoration priorities.

Industry

Emissions from the industry sector fell by 5.4 MtCO2e in 2025 compared to the previous year and were a key source of overall reductions between 2024 and 2025. Emissions in the sector are now 56% lower than 2008 levels.

- Emissions fell 3.2 MtCO2e in the iron and steel sector, due to the closure of the blast furnaces at Port Talbot steelworks in late 2024. The site is decarbonising via electrification, and construction has begun on an electric arc furnace which is due to be operational by late 2027.[7] This is positive progress towards the electrification of industry. Overall, the temporary closure of Port Talbot is responsible for almost two-thirds of the emissions reduction in industry between 2023 and 2025.

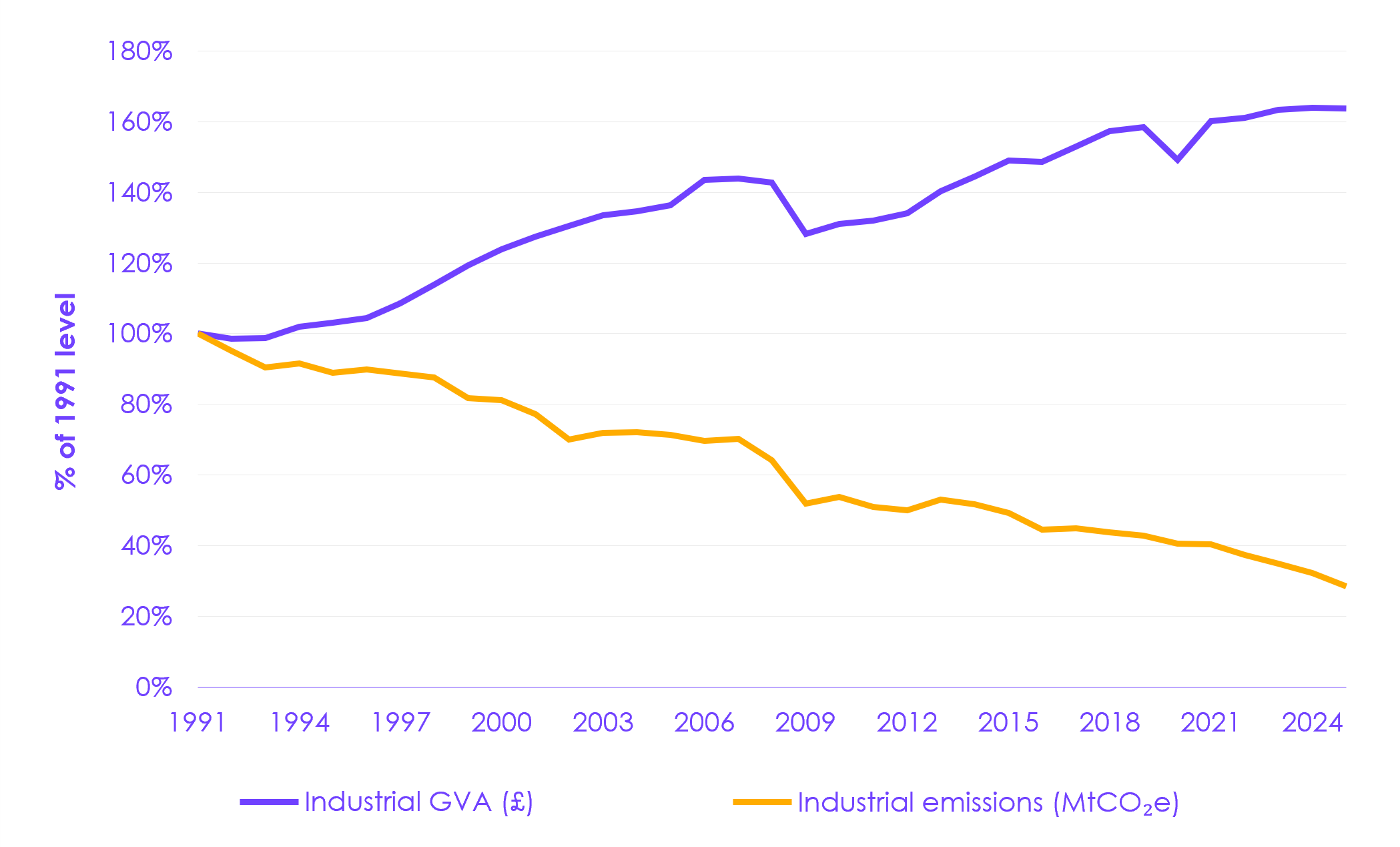

- The rest of the reduction in industrial emissions partly relates to falling output from energy-intensive industry. This is broadly consistent with a longer-term trend reflecting a structural shift in UK manufacturing. Since the 1990s, the output of emissions-intensive materials has fallen and the sector has shifted to producing less carbon-intensive but higher-value industrial products (Figure 1.5).

- Many factors (including production costs, reduced demand, and growth in developing economies) have contributed to this long-term structural shift in manufacturing. The trend is common across many developed economies and predates climate policy.

- This trend has accelerated in recent years. The gross value added (GVA) of the most energy-intensive manufacturing sectors fell a combined 6% between 2024 and 2025, and several emissions intensive manufacturing sites in the UK closed permanently in 2025. Recent closures include Ineos’ ethanol plant in Grangemouth, SABIC’s ethylene cracker in Teesside and Electric Glass’ fibreglass plant in Wigan.[8];[9];[10];[11] Since 2021, the pressures on energy-intensive industry have increased due to exposure to high gas prices and resulting higher electricity prices.

- Following Russia’s invasion of Ukraine, industrial gas prices in the UK and Europe tripled between 2020 and 2022, before settling at just over double the 2020 price.[12] This fed through to electricity prices, due to the role of gas in setting the price of electricity, with the UK particularly exposed. Facing significantly higher production costs, highly traded, energy-intensive industries, particularly chemicals, have seen a number of closures across Europe.[13] The Iran war is likely to result in similar energy price shocks, further exacerbating these pressures. In the longer term, industrial electrification, combined with the shift to a renewables-based electricity system will reduce this exposure to fossil fuel price shocks.[14]

| Figure 1.5 The change in UK industrial emissions and GVA since 1991 |

Description: Emissions in the industry sector have declined since the 1990s, whilst gross value added (GVA) has grown over the same period. Source: DESNZ (2026) Provisional UK greenhouse gas emissions statistics 2025; DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; Office for National Statistics (2025) GDP output approach – low-level aggregates; CCC analysis. Notes: GVA is calculated using a GDP output approach, in chained volume measure. The industry sector includes manufacturing and construction. |

Aviation

Emissions in the aviation sector decreased by 0.5% in 2025 compared to 2024, reaching 37.9 MtCO2e. This is a 1.4 MtCO2e (3.6%) decrease compared to 2008.

- Emissions in 2025 decreased slightly compared to 2024 despite a 3% increase in passenger-km. This is likely due to efficiency improvements from recent changes to the aircraft fleet and a small contribution from sustainable aviation fuel (SAF) uptake (see Section 3.2.6).

- Between 2008 and 2019, aviation emissions were broadly flat, ranging between 36.0–39.7 MtCO2e, they declined sharply in 2020 due to the COVID-19 pandemic, and returned to pre-COVID-19 levels in 2024. It is positive that the high annual emissions growth rate observed between 2022 and 2024 has slowed, but it is too early to say whether future aviation emissions will grow, plateau, or decrease.

- International flights account for most of aviation’s total emissions (95% in 2025). International passenger-km have increased 36% since 2008, whereas domestic passenger-km decreased by 20%.

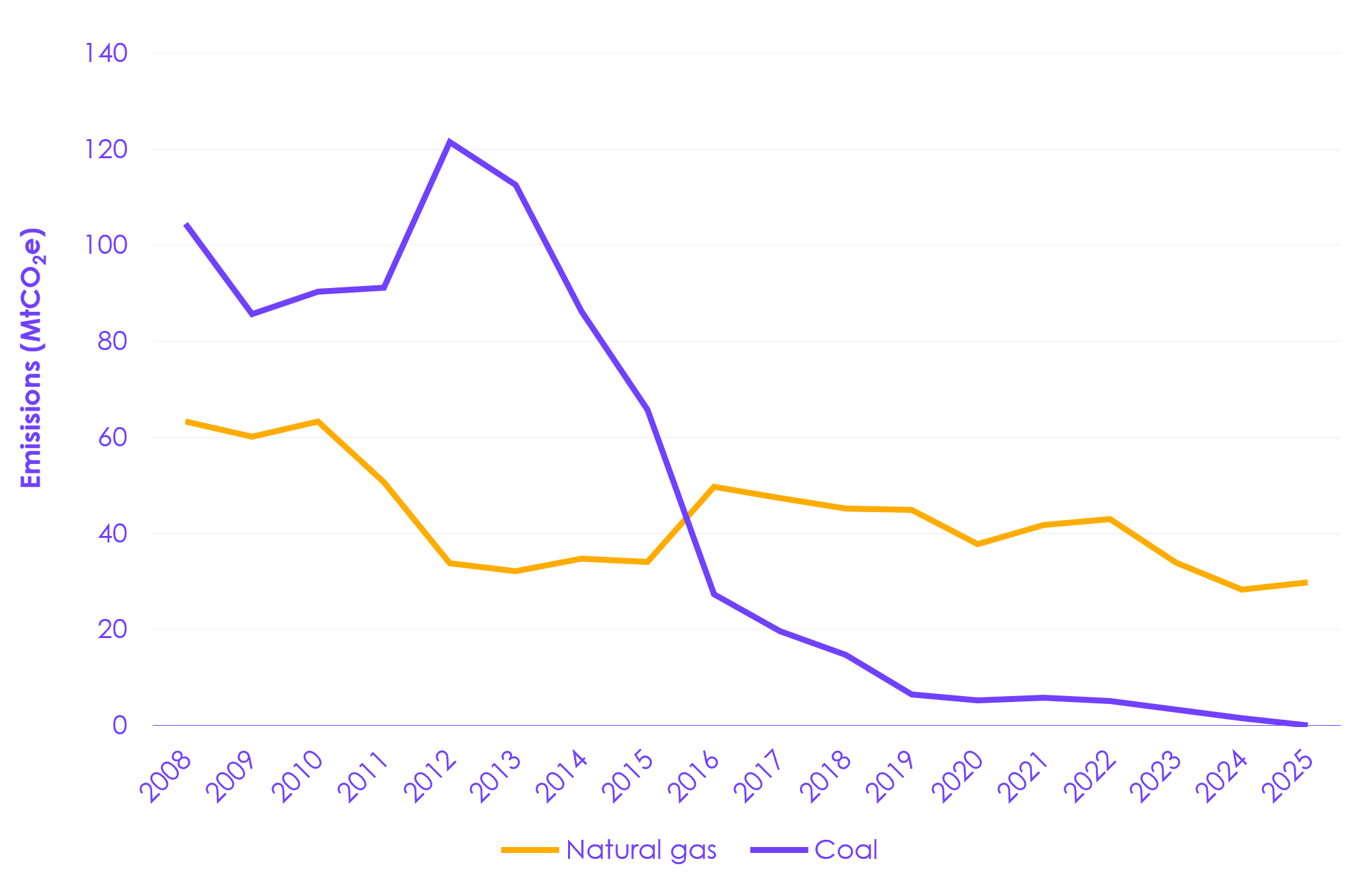

Electricity supply

The long-term trend in electricity supply emissions has been strongly downward, caused by the phase-out of coal generation and a substantial reduction in gas generation. Emissions in the sector are now 82% lower than 2008 levels, with emissions from gas now less than half 2008 levels and emissions from coal now zero (Figure 1.6). Emissions from coal fell to zero due to the closure of Ratcliffe-on-Soar (which was the UK’s last remaining coal fired power station) in September 2024.

Emissions in this sector did not fall in 2025. This was due to a 5% (4.1 TWh) increase in unabated gas generation year-on-year, which offset the reduction in emissions from coal generation. The increase in gas generation was likely due to a combination of factors:

- A 12% reduction in nuclear generation due to operational challenges at several reactors, particularly at Hartlepool.[15] Nuclear generation fell from 41 TWh in 2024 to 36 TWh in 2025.

- An 11% fall in net imports of electricity via interconnectors, from 33 TWh in 2024 to 30 TWh in 2025. While gross imports were broadly flat, there was an increase in gross exports. This was due, in part, to the opening of the new Greenlink Interconnector (which connects Wales with the Republic of Ireland) in January 2025.

- Underutilisation of wind capacity due to transmission network constraints. There was 9.4 TWh of wind curtailment in Great Britain in the 2024/25 financial year, an increase of 77% on the previous year. The proportion of potential annual wind generation that was curtailed rose from 8% to 13%.[16] Network constraints arise due to a combination of lack of network capacity at key transmission boundaries and operational unavailability during maintenance, asset replacement and reinforcement works. Unabated gas generation currently often replaces constrained wind. The deployment and utilisation of storage and flexibility technologies (including efficient dispatch decisions by the system operator) can help fix this problem, in addition to building out physical networks (see Section 4.3.7).

- Wind capacity additions in 2025 (1 GW) were also lower than the recent historical average (1.9 GW) observed between 2021 and 2024. This was in part due to delays to the Dogger Bank offshore wind farm, which was awarded CfD contracts totalling 3.6 GW in Allocation Round 3 for delivery in 2023/24 and 2024/25, but is not complete as of May 2026. Solar capacity additions were strong in 2025 relative to recent years (see Section 3.2.7).

| Figure 1.6 Decline in emissions from coal and natural gas generation in the electricity supply sector since the Climate Change Act (2008) |

Description: Emissions from coal and natural gas generation in the electricity supply sector have declined substantially since 2008. Emissions from coal generation fell to zero in 2025, while emissions from natural gas generation rose slightly. Description: Emissions from coal and natural gas generation in the electricity supply sector have declined substantially since 2008. Emissions from coal generation fell to zero in 2025, while emissions from natural gas generation rose slightly. Source: DESNZ (2026) Provisional UK greenhouse gas emissions national statistics 2025. Notes: Data shown are annual emissions for gaseous fuels and coal in the electricity supply sector. |

Fuel supply

Emissions from the fuel supply sector fell by 1.5 MtCO2e in 2025, in line with recent annual trends and continuing the significant historical decline seen over the last three decades. Emissions in the sector are now 45.0% lower than 2008 levels:

- The key drivers of emissions reductions between 2024 and 2025 were a fall in emissions from oil refining of 0.9 MtCO2e, largely due to the closure of Grangemouth and Prax Lindsey refineries in 2025, and a reduction in emissions from oil and gas platforms of 0.5 MtCO2e. Much of the reduction in production emissions from oil and gas is due to the closure of oil and gas fields as they reach end of life – the North Sea Transition Authority’s (NSTA) 2025 Emissions Monitoring Report projected an emissions reduction in offshore fields of 0.6 MtCO2e in 2025 due to production ending, in their business-as-usual scenario.[17]

- This is a continuation of a longer-term trend in fossil fuel supply production emissions. Much of the 22.4 MtCO2e reduction since 2008 has been driven by declining emissions from oil and gas production, which fell by 10.4 MtCO2e (58.4%) since 2008 and by 75.3% since their peak in 2000. The decline in oil and gas production is expected to continue as oil and gas reserves in the mature North Sea basin are increasingly depleted – the NSTA project a further decline in combined oil and gas production of 93.2% by 2050.[18]

1.1.3 Emissions from imports

The UK’s legally binding targets are set on the basis of territorial emissions (that is, emissions within the UK’s territorial borders). It is important to also consider emissions associated with UK imports. However, there has been no update on imported emissions data since our progress report last year and the latest available data are from 2022.

Emissions from imports increased by 7% between 2021 and 2022 but have changed very little since 2008. It will be increasingly important to minimise carbon leakage as the UK decarbonises domestically, but as more countries commit to and deliver on Net Zero, particularly among the UK’s major trading partners, the significance of imported emissions should diminish.

1.2 Emissions in Scotland, Wales, and Northern Ireland

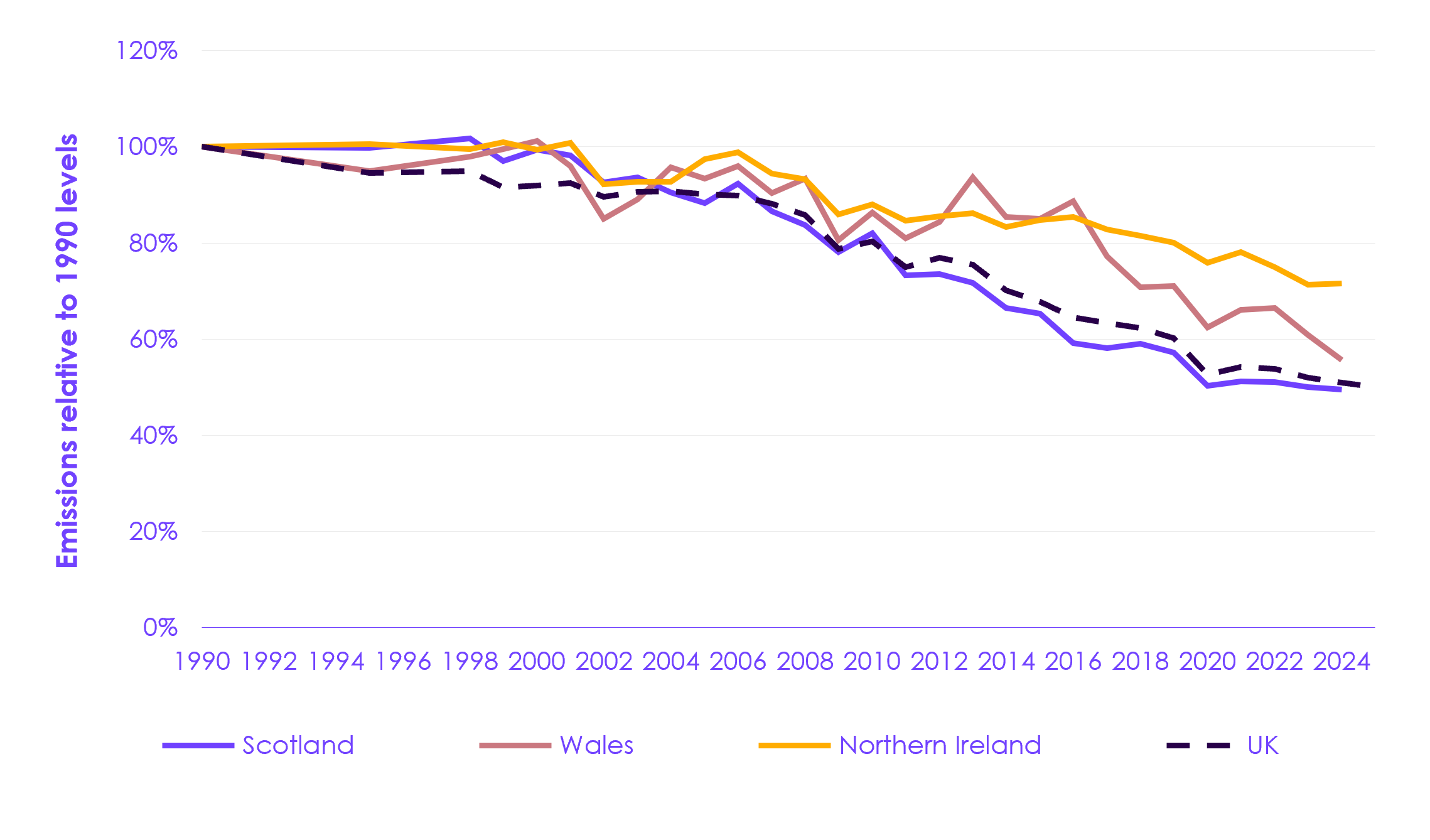

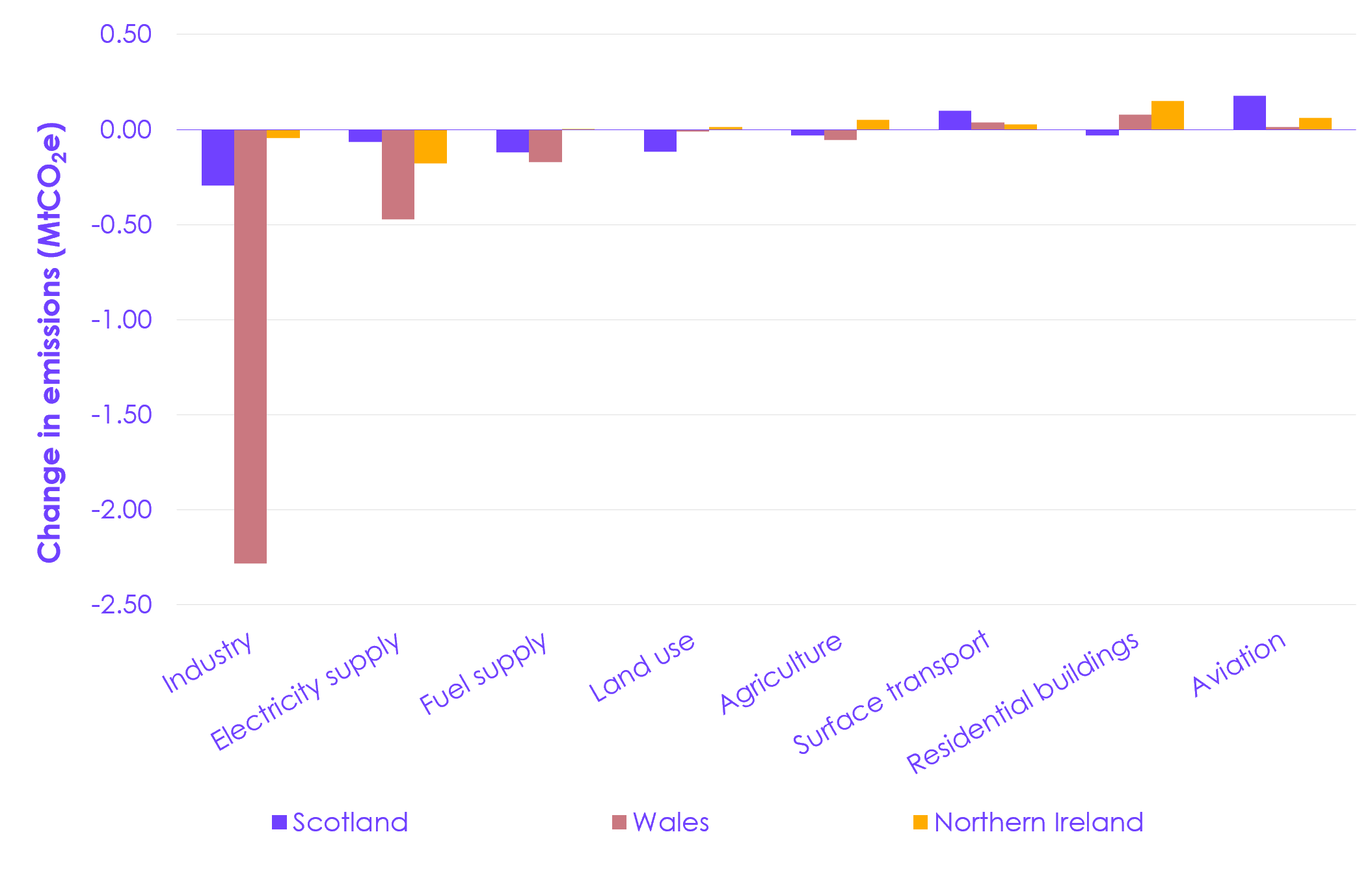

Emissions fell in Scotland and Wales but remained relatively stable in Northern Ireland between 2023 and 2024 (the latest available data) (Figure 1.7). The largest reductions were in Wales, where emissions fell by 2.8 MtCO2e compared to 2023, almost five times the percentage decrease seen in the UK overall, mainly due to the temporary closure of the Port Talbot steelworks ahead of electrification (Figure 1.8). The majority of emissions reductions to date in Scotland, Wales, and Northern Ireland have been in mostly reserved sectors, such as electricity supply, fuel supply, and industry. Future action will need to extend to more sectors of the economy, including those with substantial devolved powers, such as agriculture, land use, buildings (where emissions increased in both Wales and Northern Ireland in 2024), and surface transport (where emissions increased in all three nations between 2023 and 2024) (Figure 1.8).

- Scotland: emissions in 2024 were 39 MtCO2e, 1.0% lower than in 2023 and 50% lower than 1990 levels.[19]

- In 2024, the largest emissions reduction in Scotland occurred in the industry sector, where emissions decreased by 0.3 MtCO2e. There were also small reductions in emissions from electricity supply and fuel supply.

- These decreases were partially offset by increases in the surface transport and aviation sectors.

- Since 1990, 63% of emissions reductions in Scotland have been in the electricity supply, fuel supply, and industry sectors. Scotland’s electricity supply has been almost completely decarbonised, with emissions in 2024 96% lower than in 1990.

- Wales: emissions in 2024 were 30 MtCO2e, 8.6% lower than in 2023 and 44% lower than 1990 levels.

- Industry emissions fell by 2.3 MtCO2e (25%) in 2024 compared to 2023, accounting for 74% of total emissions reductions in Wales. This was driven by the closure of the blast furnaces ahead of electrification at Port Talbot.

- There were also reductions in emissions from electricity supply and fuel supply.

- These decreases were partially offset by increases in the buildings, surface transport, and aviation sectors.

- Since 1990, 76% of emissions reductions in Wales have been in the electricity supply, fuel supply, and industry sectors.

- The rate of emissions reduction in Wales has increased since the Environment Act (Wales) was legislated in 2016, with around three quarters of the emissions reduction from 1990 to 2024 occurring since 2016.

- Northern Ireland: emissions in 2024 were 19 MtCO2e, almost unchanged from 2023 and 29% lower than 1990 levels.

- The largest reductions were in the electricity supply sector, where emissions fell by 0.2 MtCO2e (8.2%) in 2024 compared to 2023, accounting for 68% of total reductions in Northern Ireland.

- Emissions in the residential buildings, surface transport, and agriculture sectors all increased between 2023 and 2024.

- Since 1990, 65% of emissions reductions in Northern Ireland have been in the electricity supply and industry sectors.

| Figure 1.7 Emissions reductions in Scotland, Wales, and Northern Ireland compared to the UK |

Description: Emissions fell in Scotland and Wales in 2024 but remained almost unchanged in Northern Ireland. |

| Figure 1.8 Change in Scotland, Wales, and Northern Ireland emissions for key sectors (2023–2024) |

Description: The largest emissions reductions in 2024 were in the industry sector – particularly in Wales, which saw the largest reductions due to the closure of the Port Talbot steelworks. Source: DESNZ (2026) Final UK greenhouse gas emissions national statistics: 1990 to 2024; National Atmospheric Emissions Inventory (2026) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2024; CCC analysis. |

1.3 The UK in an international context

This section sets out the global context of emissions, warming globally and in the UK, and international climate policy in 2026. It assesses the UK’s international role and contribution towards global efforts to mitigate climate change.

Global GHG emissions are yet to peak, with global temperatures continuing to increase at the fastest rates on record and climate impacts worsening.[20] Climate ambition and policy implementation are generally stable or increasing globally but remain well below what achieving global climate goals would require, and there are notable exceptions.[21] Nonetheless, the low-carbon transition is accelerating in most countries and regions, increasingly slowing or reversing annual emissions growth. Many countries, including the UK, are taking actions which will accelerate these trends in response to the repercussions from the Iran war.

While the UK produces less than 1% of global emissions, over a quarter of global emissions are produced by countries with a share of emissions less than 1%.[22] Through its international actions, the UK should seek to continue to drive global decarbonisation progress.

1.3.1 Global GHG emissions and warming

Global GHG emissions remain around all-time highs, despite slowly falling per-capita emissions. This has led to corresponding increases in atmospheric GHG concentrations, global temperatures, and climate impacts.

- Initial projections for 2025 indicate that global CO2 emissions from fossil fuels and industry were 38.9 GtCO2e, an increase of 0.8%, once again reaching their highest ever level.[23] Global CO2 emissions from land use, for which the uncertainty range is proportionately larger, are estimated to have fallen 11%, continuing a downward trend over the last decade.[24] Global methane emissions from the fossil fuel sector were estimated to remain at record high levels of around 124 MtCH4 (3.5 GtCO2e) in 2025.[25];[26]

- CO2 emissions per capita from fossil fuels and industry were broadly flat in 2025, based on population projections for 2024 and 2025, maintaining a broad plateau slightly below peak levels of 2012.[27];[28];[29]

- Atmospheric CO2 concentration reached 425.6 parts per million (ppm) in 2025, an increase of 2.8 ppm on 2024 levels, and around 50% higher than pre-industrial levels.[30]

- 2023, 2024, and 2025 have been the three hottest years on record. In 2025, warming was around 1.39ºC above pre-industrial levels. This is below 2023 and 2024 levels, when strong El Niño events were observed, but is consistent with the acceleration in long-term warming observed in recent decades. The rate of warming is at a record high.[31]

- This warming is driving increasing climate impacts globally. For example, sea level rise has accelerated to an estimated 3.67 mm on average per year in the period 2006 to 2025, more than double the average rate over 1976 to 1995.[32]

1.3.2 Climate change in the UK

The UK is already experiencing the impacts of global climate change. Hotter average temperatures, more severe heatwaves, and more intense periods of rainfall are causing significant damage and disruption and putting lives at risk. This year, the CCC’s Adaptation Committee has set out the latest evidence on climate risks and adaptations. The Fourth Climate Change Risk Assessment – Independent Assessment (CCRA4-IA) Technical Report sets out the evidence on climate risk to the UK.[33] For the first time, the Adaptation Committee also offers advice on potential solutions to address these risks in its A Well-Adapted UK report.

- 2025 was the UK’s hottest year on record. Extremely dry conditions in spring and summer impacted arable crop production and caused the most destructive wildfire season in the UK ever recorded. The May 2026 heatwave saw many weather stations recording their highest May daily maximum temperatures on record, with the highest recorded May temperature in the UK as a whole recorded in Greater London.[34] In summer 2022, temperatures exceeded 40°C for the first time, causing the early deaths of over 3,000 people in England and Wales and a 500% increase in 999 calls to fire control rooms.

- Early 2026 was exceptionally wet in parts of the UK, with long unbroken spells of rain leading to widespread flooding. Parts of southern England saw nearly twice the long-term average rainfall for January, resulting in flooding to homes, farmland, and some local infrastructure. The fluctuations from dry to wet periods seen over the last year demonstrate the extreme swings in weather already happening today.

- By the middle of the century, the UK’s climate will be much more extreme than today. Hotter heatwaves could see 92% of existing homes overheat, creating dangerous conditions for vulnerable people. Peak river flows will be up to 45% higher, last longer, and occur more frequently, driving increased flooding. Drier summers will mean more widespread drought – shortfalls in water supply could reach over five billion litres per day in England by 2050.

- Without global emissions reductions, it becomes increasingly hard to protect people and places with adaptation measures – particularly in the second half of the century.

- As set out in our advice to the UK Government on adaptation, the UK should, at a minimum, prepare for the weather extremes that would be experienced if global warming levels reach 2°C above preindustrial levels by 2050. Alongside this, it should also support global emissions reduction efforts to keep warming to lower levels.

In the A Well-Adapted UK report, the CCC’s Adaptation Committee set out their advice on potential solutions to address the priority risks from climate change and propose targets to the Government on what is required to adapt to a world of 2°C warming by 2050. Taking action on adaptation today is cheaper than dealing with the damages the UK is already experiencing. Cooling, flood preparedness, and water management are key adaptation priorities that can help address many of the climate risks the UK faces. These key adaptations must be deployed alongside actions to reduce emissions. In some key areas integrating adaptation with mitigation is needed to ensure that emissions reductions are delivered despite a changing climate and that cost and disruption for people are minimised. These include ensuring that low-carbon heating retrofits consider the need for cooling (possibly through reversible heat pumps), tree planting prioritises species (and places) that are compatible with the UK’s future climate conditions, and that new infrastructure (including in the electricity sector) is built to be resilient to future weather extremes.

1.3.3 International climate policy

In a volatile geopolitical context, the UK is among a leading group of countries demonstrating consistent and sustained decarbonisation.

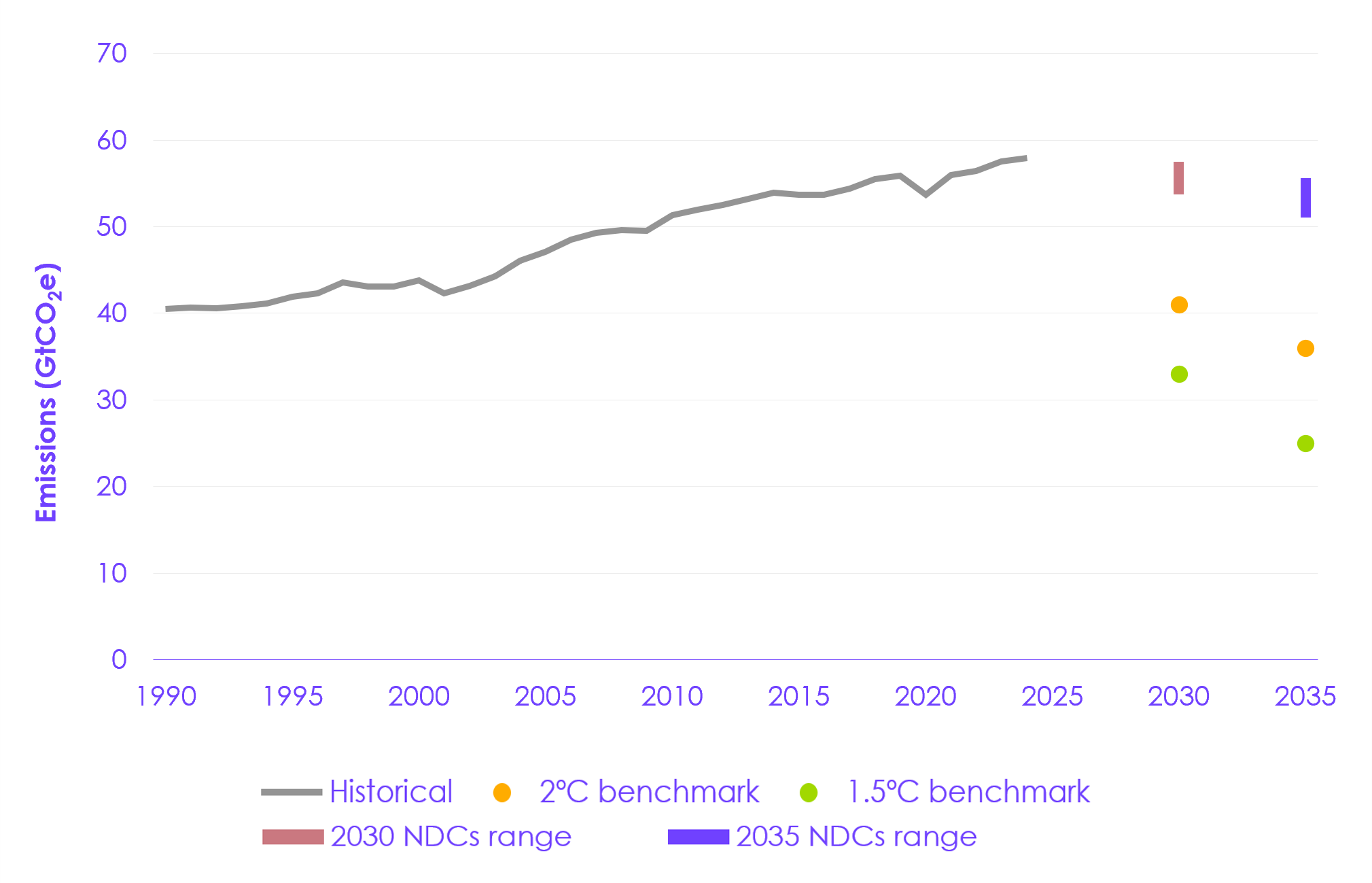

- As of May 2026, 137 countries have submitted 2035 emissions pledges to the United Nations Framework Convention on Climate Change (UNFCCC) which were due in 2025, including 18 G20 countries.[35];[36] Those submitted leave a large gap to global pathways consistent with the Paris temperature goal (Figure (1.9).[37] To deliver on the Paris temperature goal, therefore, it is essential that countries implement their existing targets and increase collective ambition.

- At COP30 in Brazil, countries restated aims to keep 1.5ºC warming within reach but acknowledged that the remaining global carbon budget “is now small and being rapidly depleted”. They resolved to limit overshoot of 1.5ºC as far as possible.[38] Plans for fossil fuel and deforestation roadmaps were not agreed, but the Brazilian presidency committed to producing them outside of the formal process.[39] At the first Transitioning Away From Fossil Fuels conference in Colombia, 57 countries agreed to work on national and regional roadmaps, macroeconomic dependencies and financial architecture, and producer-consumer alignment for the fossil fuel transition.[40]