Footnotes have been removed from the online version of this report. To read the footnoted version, please download the report.

Acknowledgements

The Committee would like to thank:

The team that prepared this report and its analysis. This was led by Emma Pinchbeck, James Richardson, Emily Nurse, Eoin Devane, James Tarlton, and Luke Jones and included Sasha Abraham, Rose Armitage, Florence Bates, Simona Battipaglia, Owen Bellamy, George Blake, Sandra Bogelein, Marili Boufounou, Marta Calore, Christian Calvillo Munoz, Rachel Carr-Whitworth, Lidice Cruz-Rodriguez, Selina Dagless, Bianca de Farias Letti, Victoria de la Cruz, Ramesh Deonarine, Joshua Deru, Tom Dooks, Caitlin Douglas, Kim Dowsett, Kieron Driscoll, Ahmed Gailani, Francesco Maria Giacomini, Ruth Gregg, Esther Harris, Cara Hawkins, Rachel Hay, Cilla Hellgren, Robbie Herring, Gemma Holmes, Daisy Jameson, Ariana Jessa, Sam Karslake, Emma Kearney, Miriam Kennedy, Michael Lord, Grace Macready, Luke Maxfield, Moryse McInniss, Aaron McMahon, Richard Millar, Bea Natzler, Chloe Nemo, Chris Parker, Finna Parkinson, Emma Patterson, Lois Player, Simon Rayner, Andrew Romang, Elena Saggioro, Miranda Schroder, Viv Scott, Penny Seera, Olivia Shears, Marcus Shepheard, Bryony Sheridan, Joris Simaitis, Thomas Smith, Rachael Steller, Felicity Taylor, Seán Taylor, Indra Thillainathan, Sam Van Stroud, Emma Vause, Sophie Vipond, Zelna Weich, Chloe Welsh, Eveline White, Hannah Williams, Kate Williamson, Louis Worthington, Charley Wright, Ken Wright, and Susie Wright.

Our previous Committee member, Professor Michael Davies.

Our expert advisor on the role of households and the public in the Net Zero transition, Professor Rebecca Willis.

A wide range of organisations and individuals who participated in workshops, engaged with us, submitted evidence, or met with the Committee bilaterally.

Executive summary

The climate is changing. Global warming has unequivocally been caused by greenhouse gas emissions, with 100% of the observed long-term temperature change attributable to human causes. Evidence of climate change is visible around the world, including in Scotland. In 2022, Scotland recorded its highest ever temperature of nearly 35°C in the Scottish Borders, impacting health, ecosystems, and infrastructure. In 2023, prolonged rainfall followed by Storm Babet led to widespread flooding and several deaths, as well as substantial disruption to transport and power systems.

The Climate Change (Scotland) Act 2009 (‘the Act’) sets the framework for the Scottish Government to address climate change. The Act has an ambitious target to reach Net Zero greenhouse gas emissions by 2045, with any residual emissions balanced by removing carbon dioxide from the atmosphere. This is five years earlier than the rest of the UK due to the greater potential for carbon sequestration in Scotland.

In 2024, Scotland’s interim emissions targets for 2030 and 2040 were repealed as the progress required to meet the 2030 target was deemed to be beyond what was credible. The Act was amended to replace interim targets with carbon budgets. Carbon budgets are legally binding caps on greenhouse gas emissions in Scotland over five-year periods. The UK, Wales, and Northern Ireland also use carbon budgets to set binding milestones for emissions reductions on the way to their Net Zero emissions targets.

In line with the Act, this report sets out the Committee’s advice on the level of Scotland’s four carbon budgets, covering the period 2026 to 2045. We recommend that the Scottish Government sets its carbon budgets, including Scotland’s share of international aviation and shipping emissions, at annual average levels of emissions that are:

- 57% lower than 1990 levels for the First Carbon Budget (2026 to 2030).

- 69% lower than 1990 levels for the Second Carbon Budget (2031 to 2035).

- 80% lower than 1990 levels for the Third Carbon Budget (2036 to 2040).

- 94% lower than 1990 levels for the Fourth Carbon Budget (2041 to 2045).

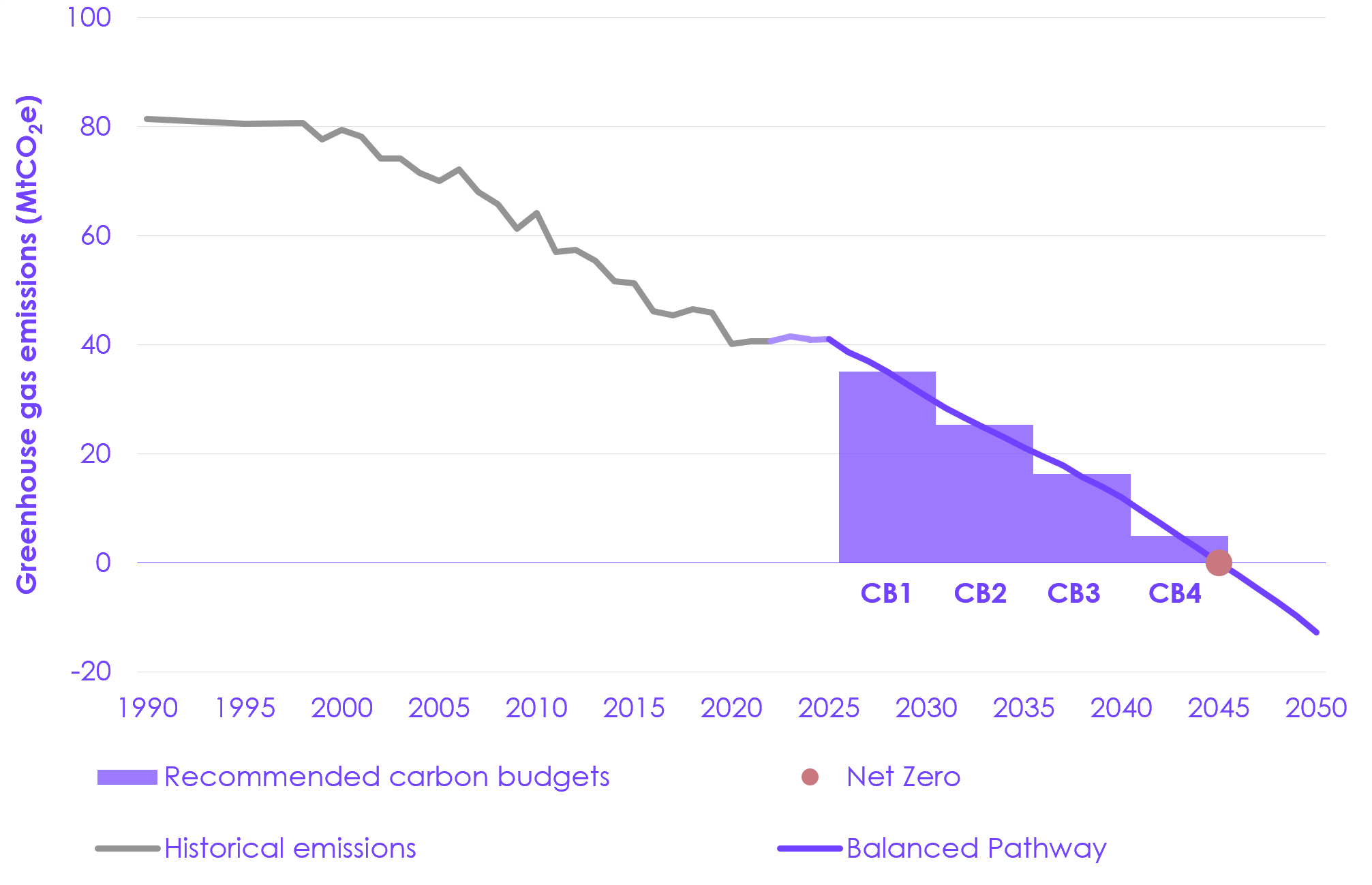

These carbon budgets are given as five-year average percentage reductions from 1990 levels. As of 2022, the latest year for which there is data, emissions were 50% below 1990 levels (Figure 1).

Our advice shows that these proposed carbon budgets are deliverable and Scotland can achieve its 2045 Net Zero target. Our advice is based on the latest technological, social, and economic evidence; extensive sector modelling; and engagement with stakeholders. The Committee’s advice also considers the relationship of UK-wide action on climate change to specific features of the Scottish economy and devolved powers. Our recommendations are based on our Balanced Pathway: an ambitious but credible route to Net Zero for Scotland by 2045.

Achieving these targets would mean households benefit from more efficient technologies, less draughty homes, and cleaner air. For many households, changes to travel and home heating will lead to savings, provided appropriate policy is in place.

Getting to Net Zero by 2045 will require immediate action, at pace and scale. While the Committee offers advice, decisions on the exact pathway and policies within devolved powers are for the Scottish Government and the Scottish Parliament.

Progress to date has largely come from electricity decarbonisation, reflecting Scotland’s abundant renewable resources. This is a reserved area of policy and Scotland has benefited from measures across Great Britain’s electricity system. Action will increasingly be required in predominantly devolved policy areas to hit the Net Zero 2045 target and the proposed carbon budgets. Now that the framework for climate action has been reset, the Scottish Government has the opportunity to use its powers to match its ambitions with action.

Alongside this, the Scottish Government will need to continue working with the UK Government, the Welsh Government and the Northern Ireland Executive to make progress where powers are shared or remain reserved. Making electricity cheaper, through rebalancing prices to remove policy levies from electricity bills, is a key recommendation the Committee have made to the UK Government and will be essential to delivering Scotland’s targets, in tandem with action by the Scottish Government.

|

Figure 1 The recommended carbon budgets for Scotland |

Description: The Balanced Pathway sets the recommended level of Scotland’s carbon budgets. |

Fair and safe Scottish emissions budget

The Act requires the setting of a ‘fair and safe Scottish emissions budget’. This is defined as the aggregate amount of net Scottish emissions of greenhouse gases for the period 2010 to 2050, consistent with Scotland contributing appropriately to holding the increase in global average temperature in line with the Paris agreement goal.[1] The Committee recommends that the fair and safe Scottish emissions budget is set at 1,129 MtCO2e. Reducing emissions in line with our Balanced Pathway would keep Scotland within this proposed fair and safe Scottish emissions budget.

Priority actions

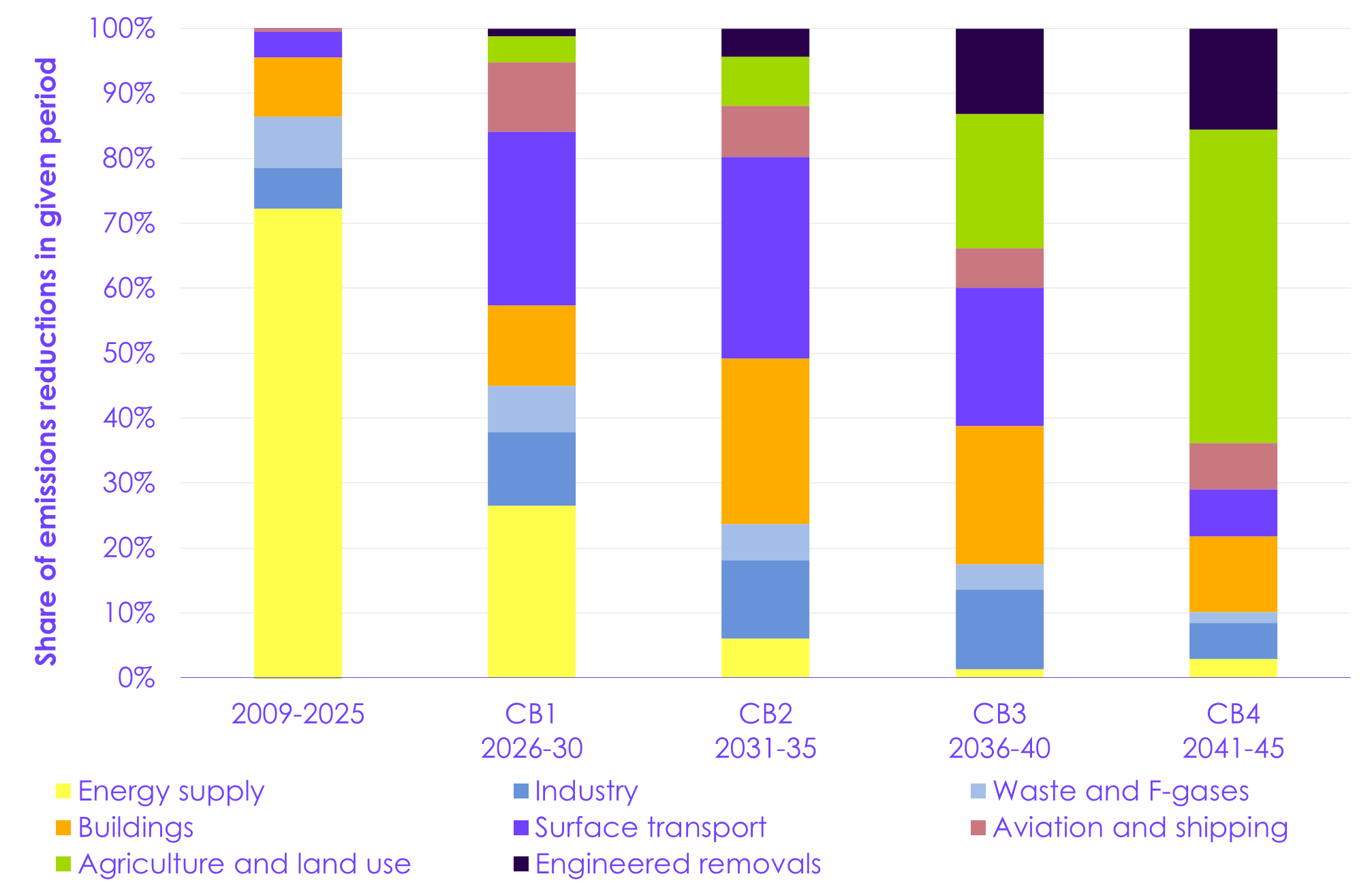

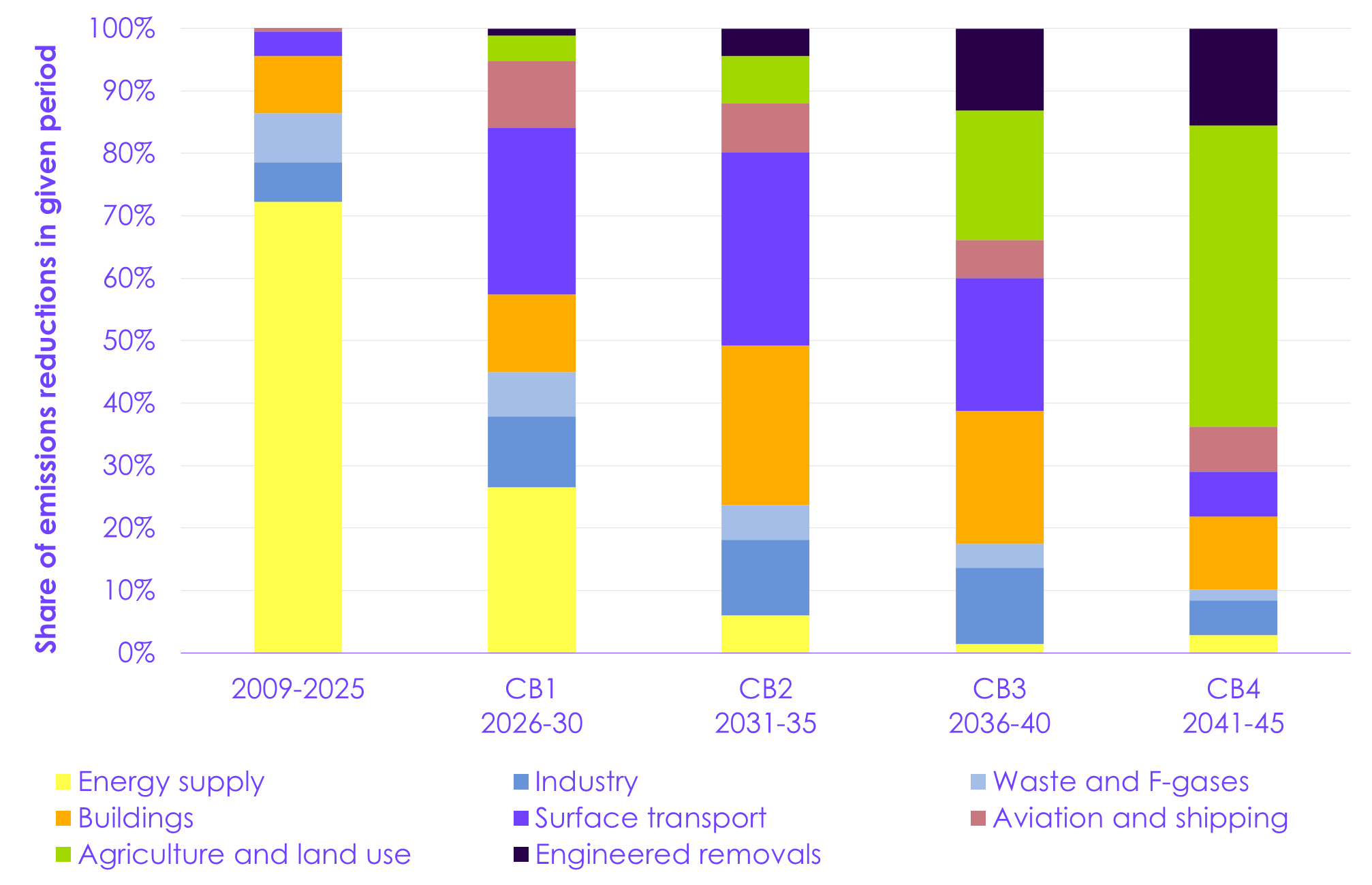

Since the introduction of the Act in 2009, over 70% of the emissions reduction seen in Scotland has been in the energy supply sectors. This is largely due to the phase-out of coal and the ramp-up of renewable electricity generation. The last coal power station in Scotland closed in 2016. Since then, emissions reductions have slowed (outside the effects of the COVID-19 pandemic). Achieving our recommended carbon budgets will require Scotland to resume the pace of emissions reduction that was seen between 2009 and 2016, with contributions broadening to more sectors across the economy (Figure 2).

Electric technologies are now the clear low-carbon choice in many areas. Technologies such as heat pumps and electric vehicles (EVs) are available today and could be deployed rapidly, provided the right incentives are in place. Almost half of emissions reductions in our Balanced Pathway come from electrification, particularly the roll-out of EVs and heat pumps and the remaining decarbonisation of electricity generation.

Emissions reductions from surface transport are the largest contribution to meeting the first two carbon budgets. With the cost of EVs falling, the Scottish Government has an important role in enabling successful implementation of the zero-emission vehicle (ZEV) mandate, including by expanding provision of charging infrastructure and providing reliable public information on EVs. The Scottish Government should also promote modal shift away from cars by improving public transport services and active travel infrastructure.

Emissions reductions from buildings are the second largest contribution to meeting the first two carbon budgets in our pathway. Together with energy efficiency measures, more efficient electrified heating can help reduce fuel poverty in Scottish households. Clean, efficient, electric technologies can offer wider benefits such as reduced air pollution and lower and less volatile energy bills compared to continued reliance on fossil fuel technologies.

It has been 18 months since the Scottish Government initially consulted on the Heat in Buildings Bill, which the Committee described in our 2023 report on Progress in reducing emissions in Scotland as a potential template for other parts of the UK. It is therefore disappointing that the proposals for regulations to upgrade properties at the point of sale have been abandoned, with, as yet, no specific alternative measures to deliver the target for heating to be zero emissions by 2045.

By the time of the Third and Fourth Carbon Budgets, the agriculture and land use sectors will be making the biggest contribution to emissions reduction in our pathway for Scotland. Together, agriculture and land use can reach Net Zero by 2045. Natural carbon sequestration, mostly increased tree planting and restoration of degraded peatlands, offsets the remaining emissions from livestock in 2045. This requires rapid scaling up of tree planting now because of the time it takes for trees to mature and start absorbing substantial amounts of carbon. The Scottish Government will need to support farmers and rural communities to diversify their incomes away from livestock farming and towards woodland creation, peatland restoration, agroforestry, and renewable energy.

|

Figure 2 Distribution of emissions reductions during each carbon budget period in the Balanced Pathway in Scotland |

|

Description: Action to reduce emissions is needed across a wide range of sectors. While the vast majority of emissions reductions to date since the introduction of the Climate Change (Scotland) Act 2009 have come in the energy supply sector, increasing contributions will be required from other sectors to meet the carbon budgets. |

Sources of future emissions reductions

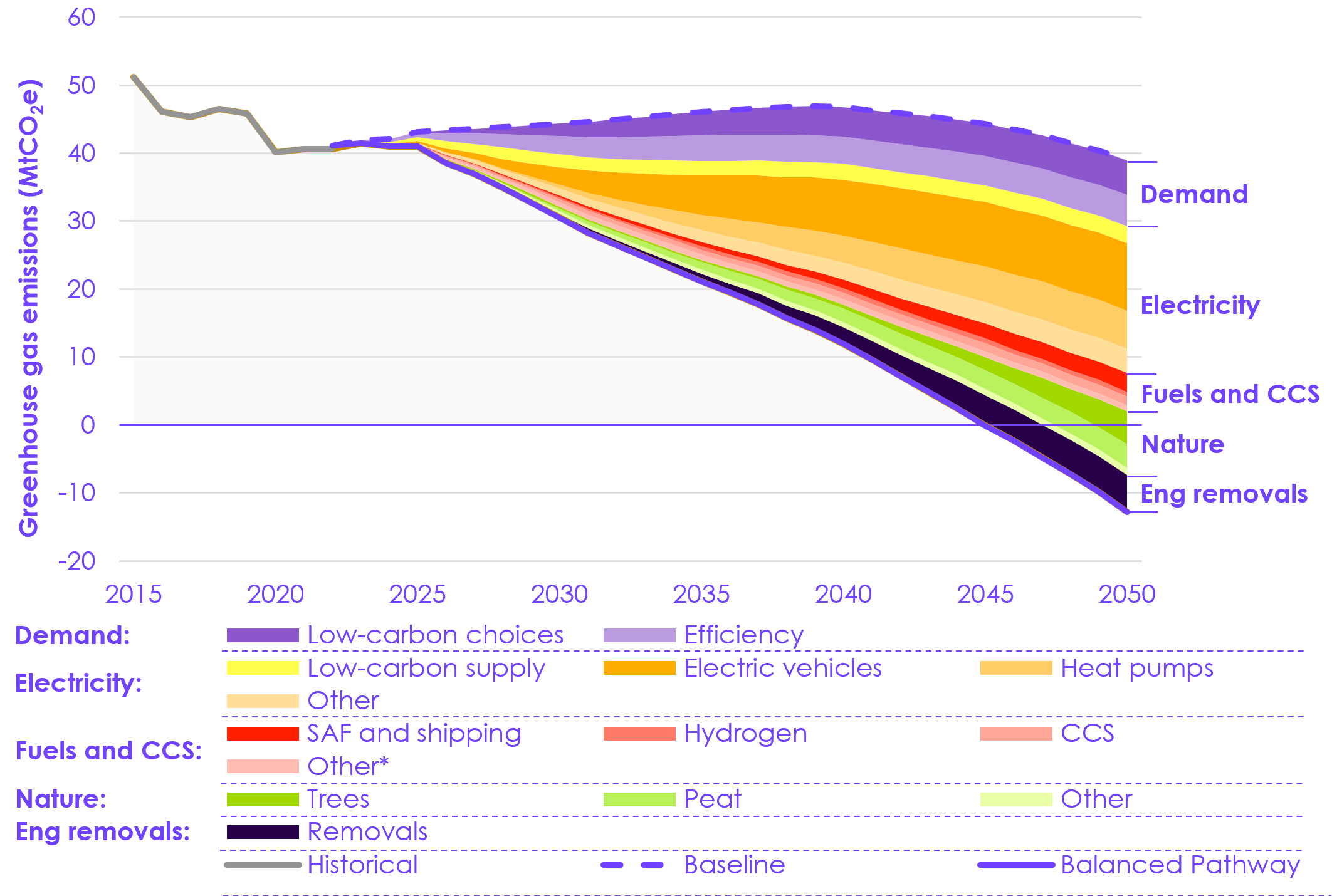

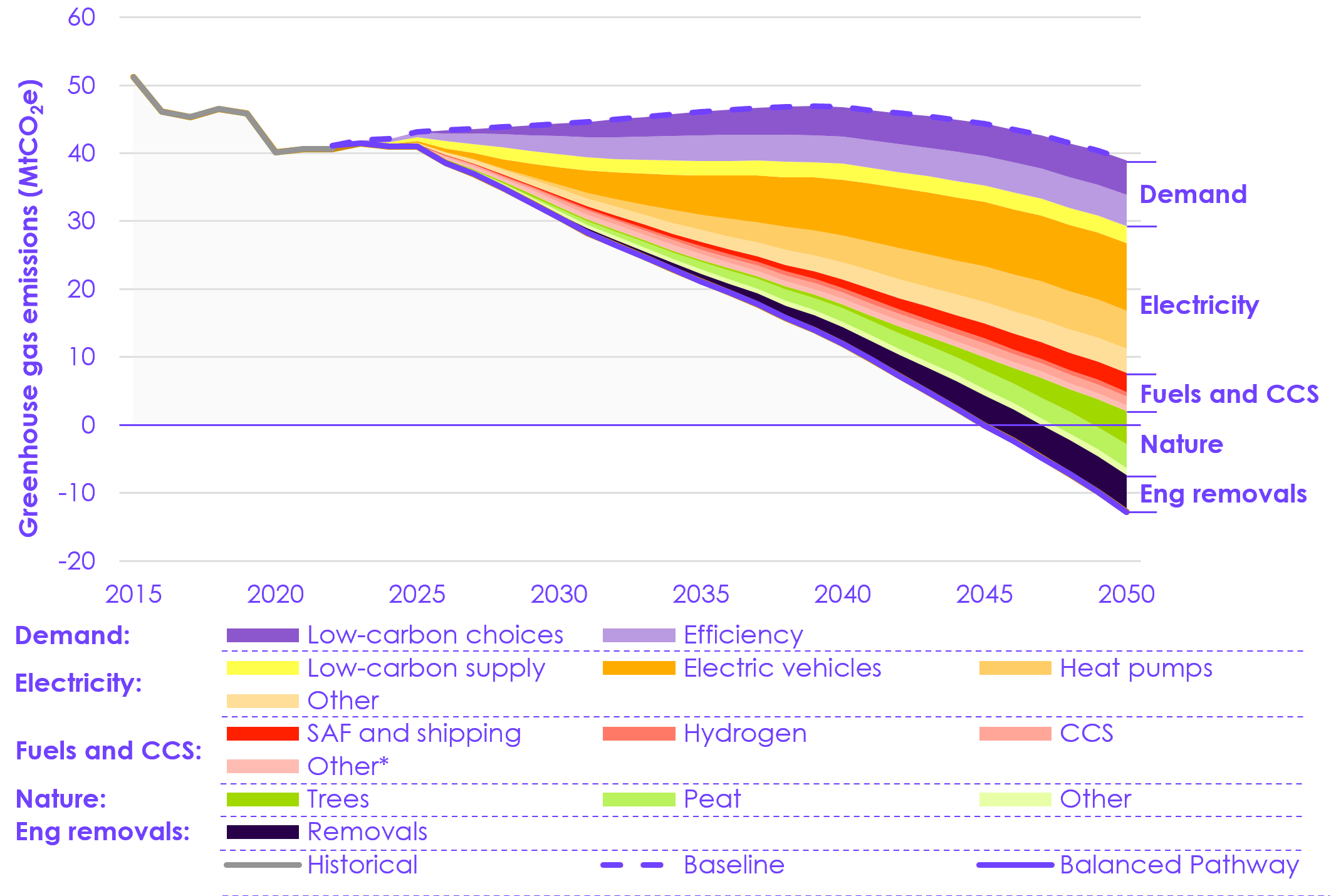

The First and Second Carbon Budgets cover the next decade. In our pathway, they are predominantly met from electrification of key technologies across the economy and measures to reduce demand for high-carbon activities (Figure 3). There are also important contributions from low-carbon farming, low-carbon fuels, and carbon capture and storage (CCS). For the Third and Fourth Carbon Budgets, nature and engineered removals play more of a role in offsetting emissions in areas in which electrification is not possible. Action is needed now to ensure Scotland can deliver these future reductions.

1. Electricity

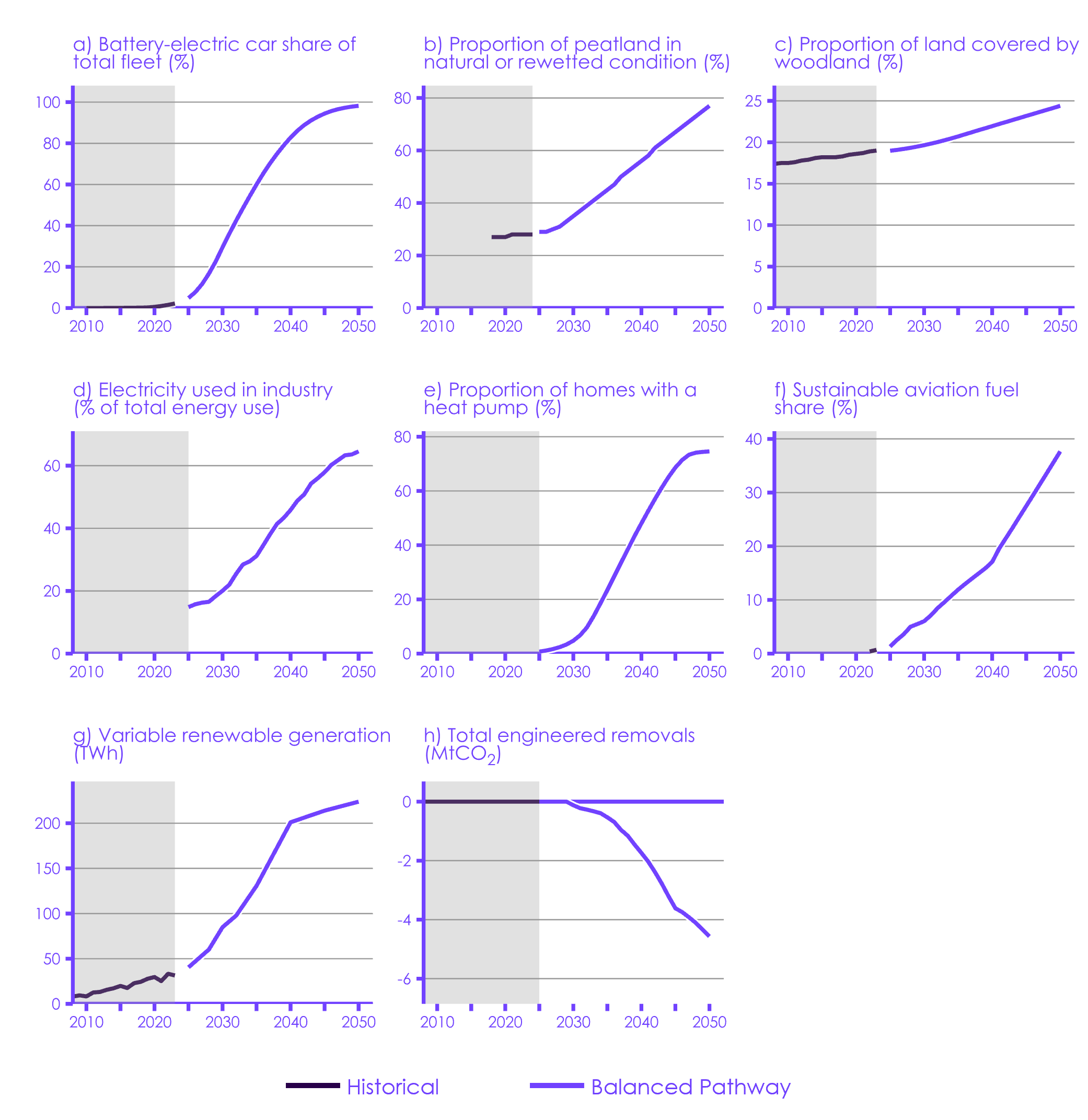

Electric technologies are now the clear low-carbon technology choice in many areas, including surface transport, buildings, and much of industry. They are available today and could be deployed rapidly in many cases, provided the right incentives are put in place. Scaling up these immediate options is key to meeting all of Scotland’s carbon budgets. Throughout the Balanced Pathway, electrification delivers almost half of the total required emissions reduction.

- Low-carbon supply: in our pathway, the capacity of variable renewables in Scotland (including offshore and onshore wind and solar) more than triples from 15 GW in 2023 to 49 GW by 2035, increasing to 66 GW by 2045. This provides 98% of electricity generation in Scotland in 2035 and caters for increasing demand in Scotland and the rest of Great Britain (GB). Grid storage, use of storable fuels on the GB-wide network, and smart demand flexibility ensure a reliable supply of electricity even in adverse weather years. These technologies need to be accompanied by rapidly expanding the transmission grid, upgrading the distribution network, and speeding up the grid connection process. To deliver clean electricity, the planning process to approve large electricity infrastructure projects in Scotland needs to be urgently improved.

- EVs: by 2035, around three-fifths of cars and vans on Scottish roads are fully electric in our pathway, compared to 2.2% for cars and 0.8% for vans in 2023. By 2045, this rises to 94% of cars and vans. This requires a rapid increase in the market share of new electric cars and vans, underpinned by the falling costs of EV batteries, with new electric cars and vans expected to reach price parity with petrol and diesel vehicles between 2026 and 2028.

- Heat pumps: by 2035, 40% of existing homes are heated by low-carbon electric systems in our pathway. The majority of these (around a quarter of existing homes) are heated by a heat pump, either as standalone or communal systems, with the rest heated by heat networks or direct electric systems.[2] By 2045, 92% of existing homes have low-carbon heat, reaching all homes by 2050. Annual heat pump installations in existing homes will need to accelerate rapidly, reaching nearly 35,000 by 2030. This rate of increase is in line with that seen in other European countries, such as the Republic of Ireland and the Netherlands. While this rapid increase in installation rates is feasible, it requires immediate policy support. For tenement buildings, communal heat pumps, including high temperature systems, and heat networks are likely to be the best solutions in many cases. Appropriate governance frameworks will be needed to coordinate residents and support their delivery.

- Industrial electrification: by 2035, the proportion of industrial energy supplied by electricity in our pathway doubles from levels in 2025, reaching around a third. This rises to 58% by 2045. Electric alternatives, such as electric steam crackers in the chemicals sector, replace most types of fossil fuel-fired industrial equipment. Electrifying industry allows manufacturers in Scotland to benefit from global demand for low-carbon goods.

2. Demand

Measures to reduce demand for high-carbon goods and services can be enacted from today and are particularly important to reduce emissions while high-carbon technologies are still being replaced by low-carbon alternatives. They can also deliver savings and health benefits. In 2035, 40% of cars and 60% of home heating systems in Scotland are still powered by fossil fuels in our pathway, so reducing demand and improving efficiency present a significant opportunity to decrease emissions over the first two carbon budgets.

- Increased efficiency: by 2035, our pathway sees cost-effective resource and/or energy efficiency measures deployed across most sectors. This includes home insulation, more efficient use of resources in industry, and reductions in commercial, household, and food waste.

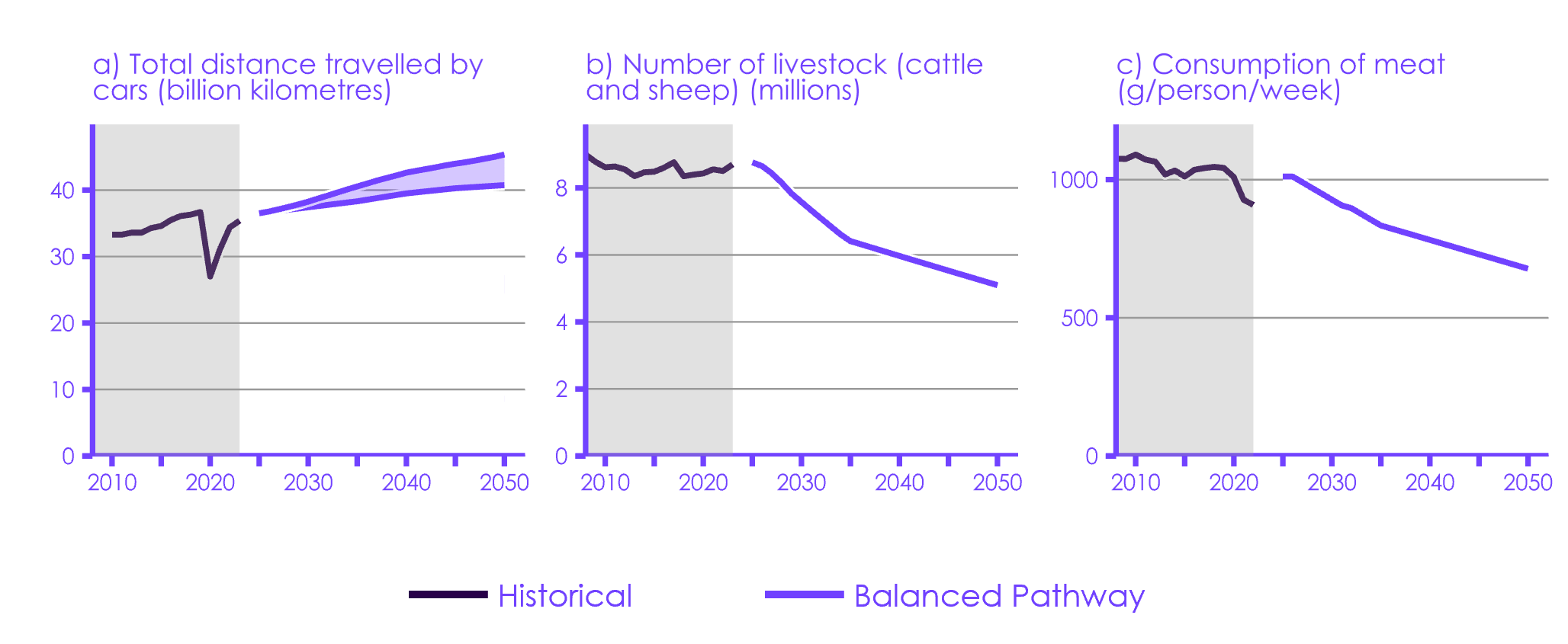

- Low-carbon choices: by 2035, our pathway sees people make some shifts towards lower-carbon choices, including a shift to public transport and active travel, and a reduction in meat (especially beef and lamb) and dairy consumption, within overall healthier diets. This is enabled by making alternatives more available, cheaper, and more attractive. Diet change leads to reductions in livestock herds and their associated emissions as well as freeing up land for nature (see below). Flying remains close to today’s levels until technology develops, with flights to and from the Highlands and Islands assumed to continue, providing essential connectivity.

3. Low-carbon farming, low-carbon fuels, and CCS

While electrification is the main technological decarbonisation solution in key sectors, there is also an important supporting role for low-carbon fuels and CCS to address sources of emissions that are less well suited for electrification. Agriculture is a significant source of emissions in Scotland, so developing low-carbon farming practices is essential. Together, these make up around 10% of the total emissions reductions required in the Balanced Pathway.

- Low-carbon farming: a number of low-carbon farming practices and technologies are introduced in our pathway, providing around half the emissions reductions in the agriculture sector. Livestock dominates the sector in Scotland, with feed additives and waste and manure management being the most important measures.

- Low-carbon fuels: ships transition to a mix of low-carbon fuels, predominantly low-carbon ammonia and synthetic fuels. Planes transition to using some sustainable aviation fuels. Hydrogen plays a small but important role in industry and in larger off-road mobile vehicles in agriculture. However, we see no role for hydrogen in heating for buildings.

- CCS: carbon capture and storage plays an important role in industry, for example capturing emissions from chemicals and cement production. It is also used for some low-carbon hydrogen production, at Scotland’s energy from waste plants, and to underpin engineered removals in our pathway.

4. Nature

Nature-based measures, including restoring peatland and planting new woodland, are integral in growing land-based carbon sequestration. Together with renewables and agroforestry, they provide opportunities for Scottish farmers and land managers to diversify their income streams away from livestock farming.

Nature-based measures are vital for Scotland to achieve its longer-term targets, contributing 8% of the emissions reductions required by 2035. This increases to 13% by 2045. There is a delay between the planting of woodlands and the time it takes for them to reach peak rates of absorbing CO2, so immediate action is needed to capture these benefits later in the pathway. Scaling up these nature-based actions allows agriculture and land use together to reach Net Zero emissions by 2045.

- Peatlands: rewetting and restoration of degraded peatlands delivers the majority of the emissions reductions in land use in our pathway. Our pathway sees a rise in the proportion of peatland under such management from the current 29% to 45% in 2035, and to 67% by 2045.

- Woodland and agroforestry: 38% of the new woodland created in our UK-wide pathway between 2025 and 2050 is in Scotland. The proportion of woodland cover in Scotland rises from the current 19% to 21% in 2035, and 23% by 2045. Delivering this will require support for land managers and farmers to more than double planting rates over the next decade. Trees and hedges on farms also play a role, supporting continued food production alongside sequestration in vegetation and soils.

5. Engineered removals

Engineered removals help to balance residual emissions from sectors that cannot fully decarbonise. With emissions from agriculture balanced by land use sinks in our pathway, engineered removals are used to balance small residual emissions, especially in aviation and industry. Engineered removals contribute around 10% of the total emissions reductions required by 2045.

Our pathway sees a gradual ramp-up in engineered removals starting at the end of the First Carbon Budget and reaching -3.6 MtCO2e by 2045. It is predominantly a mix of direct air carbon capture and storage (DACCS) and bioenergy with carbon capture and storage (BECCS), with smaller contributions from enhanced weathering and biochar.

The amount of engineered removals in 2045 is driven by the need for the UK as a whole to balance residual emissions to achieve Net Zero in 2050, and a feasible scale-up to reach that level. Scotland’s share of engineered removals technologies is based on geographical assumptions in our pathway, such as the location of existing facilities and expected CCS clusters.

|

Figure 3 Sources of abatement in the Balanced Pathway |

|

Description: Scotland’s carbon budgets are delivered through five key routes: electricity; demand, low-carbon farming, low-carbon fuels, and CCS; nature; and engineered removals. The largest share of emissions reduction is from the switch from fossil fuels to electric technologies powered using low-carbon electricity. |

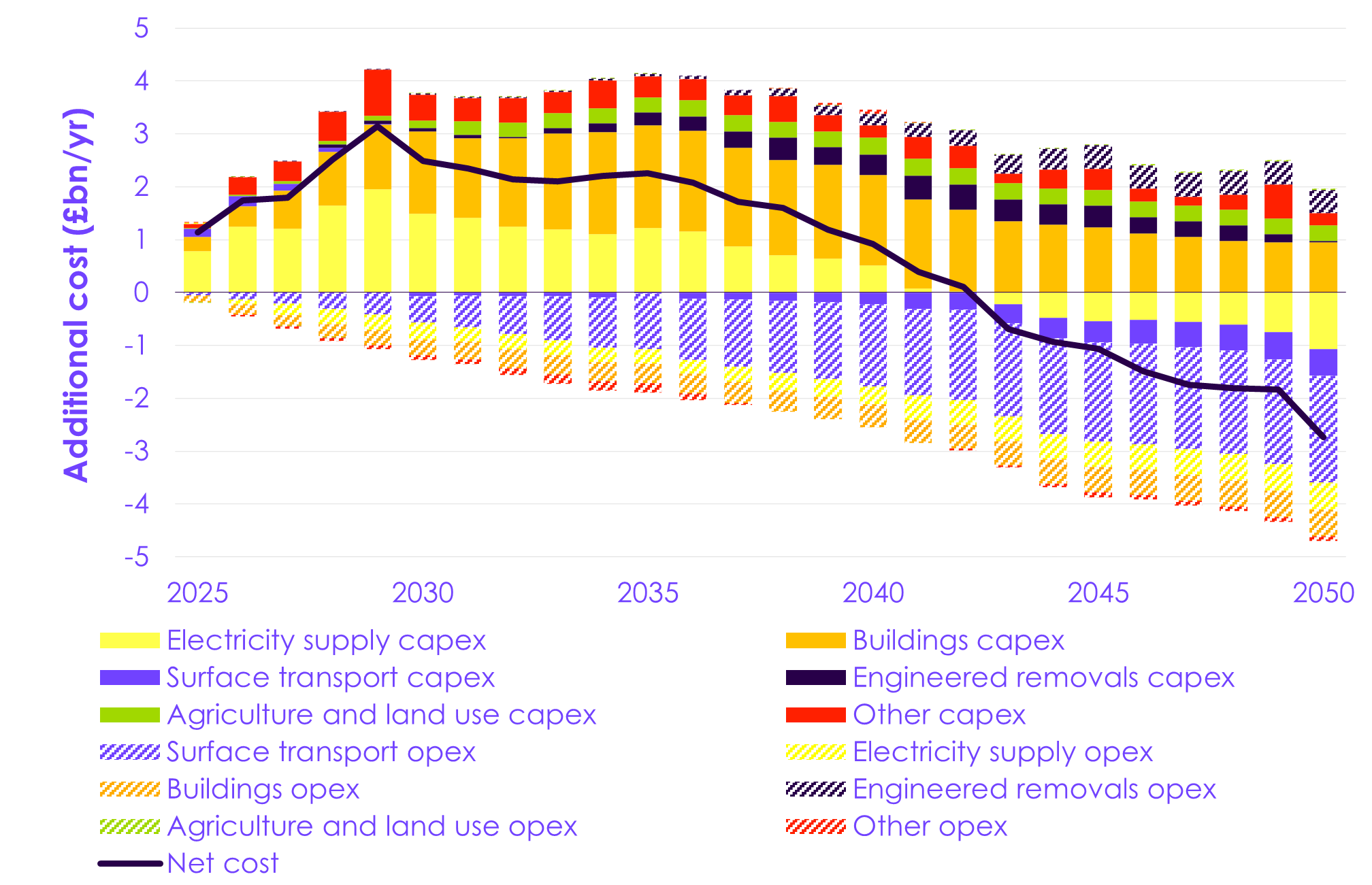

The cost of the transition

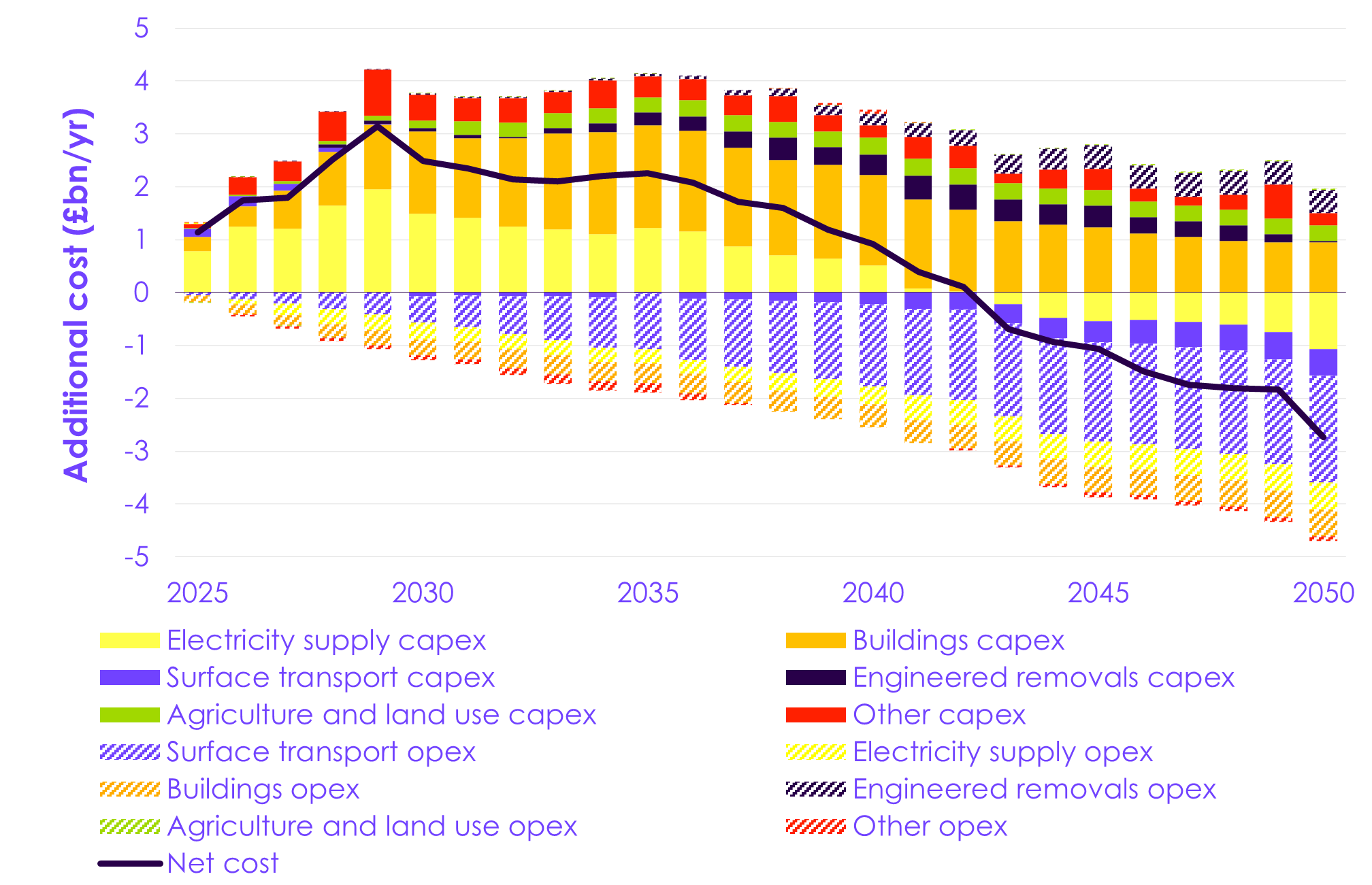

The Balanced Pathway requires upfront investment. In many sectors, this will lead to significant savings in the future as inefficient fossil fuel technologies are replaced by more efficient, low-carbon alternatives. When combining capital and operating costs, we expect the Balanced Pathway to result in a net saving during the early 2040s. On average, there will be a net cost of around £750 million per year between 2025 and 2050, which is around 0.4% of Scotland’s GDP (Figure 4).

- EVs will lead to a significant cost saving. Electric cars and vans are already generally cheaper to run and maintain, and will soon be cheaper to buy, than their fossil fuel-based alternatives. Households will see a significant reduction in the cost of driving.

- Heat pumps are more efficient than gas boilers, which should lead to lower household energy bills provided electricity is made cheaper, reflecting its true economic cost. However, homes in Scotland are predominantly designed around gas heating and will need a one-off improvement to be suitable for heat pumps in many cases. This upfront investment is a sizeable element of the total costs, and households will require policy support with these one-off costs.

- Electricity supply requires upfront investment in renewable generation and grid infrastructure. With much lower operating costs, this generates savings over time in our pathway.

- We include the costs of engineered removals in our costs analysis. Who pays for removals is a policy choice. In our UK-wide Seventh Carbon Budget advice (2025), we assumed that the costs of removals, UK-wide, are predominantly borne on a ‘polluter pays’ basis by industries such as aviation that have residual CO2 emissions. These costs would therefore be met by people across the UK, rather than necessarily in Scotland.

|

Figure 4 Additional capital expenditure and operating costs in the Balanced Pathway, compared to the baseline |

|

Description: Additional costs in the Balanced Pathway are frontloaded, peaking in 2029. Capital costs are offset by operating savings in later years, with the pathway becoming a net cost saving overall in 2043. |

Households and the economy

So far, emissions reductions in Scotland have largely involved actions by business and government. To meet Scotland’s carbon budgets, households will need to make some changes. The most important will be to buy heat pumps (including communal systems) and electric cars, when it is time to replace fossil fuel boilers or cars; to eat less meat and dairy, building on current dietary trends; and to keep flying close to today’s levels until technology develops. Policy and business action will need to make household low-carbon choices easy, attractive, and affordable, and ensure trusted information is provided to the public.

Households in Scotland, including those in less energy efficient properties or in fuel poverty (31% of Scottish households in 2022), will benefit from more efficient technologies, lower bills, less draughty homes, and cleaner air.

Most sectors of the economy, particularly in services, will see little change in activity other than switching to low-carbon heating and vehicles. However, it will be important to plan carefully for some sectors and regions:

- The oil and gas industry has been a key part of the Scottish economy, and in particular the local economy in Aberdeen and North East Scotland, for decades, alongside other industries. Regardless of the Net Zero transition, North Sea production will continue to decline, creating a requirement for new sources of well-paid employment. The Net Zero transition presents opportunities in low-carbon offshore industries, electricity network development, and onshore wind. The Scottish Government should work with communities, workers, and businesses to develop proactive transition plans that enable access to secure employment and business opportunities that come with the Net Zero transition.

- The Scottish Government needs to engage with farmers and their communities, and support them to diversify their incomes, including towards woodland creation, peatland restoration, agroforestry, and renewable energy. This should keep in mind implications for Scottish heritage and culture. UK-wide policy must protect against risks of carbon leakage from agricultural imports. In the Balanced Pathway, a reduction in demand for meat and dairy across the UK avoids imports of these products increasing. Carbon border adjustment mechanisms may also be needed.

Key actions

We have 18 priority recommendations for immediate action to put Scotland on track to deliver the carbon budgets. The full set can be found in Annex 1. Core themes include:

- Supporting households to install low-carbon heating. Scotland needs to rapidly transition to low-carbon electrified heat. While the transition should lead to lower energy bills for consumers, continued support is needed to address barriers in upfront costs, especially for low-income households. The Scottish Government urgently needs to develop an alternative to the abandoned proposals in the Heat in Buildings bill for regulations to upgrade properties at the point of sale. This will need to enable a rapid transition from fossil-fuel heating systems to low-carbon heating in privately owned homes, supporting the proposed heating decarbonisation target. The Scottish Government will need to develop governance frameworks to allow for the installation of communal low-carbon heating systems, where these are appropriate (in particular, in tenements).

- Supporting households to install home insulation measures. It is also important to provide effective support to households, particularly those on low incomes, to install home insulation measures. The Scottish Government should urgently consult on the details of the proposed minimum energy efficiency standards for privately owned homes, noting that delaying this further could have negative impacts on fuel poverty in Scotland.

- Expanding EV charging and travel infrastructure. The Scottish Government should support the deployment of public charge points across Scotland. The number of public EV charge points per capita in Scotland is 7% higher than the UK average but will need to continue to increase in line with EV uptake. With prices for new and second-hand EVs falling, there is an opportunity for rapid take-up provided the right infrastructure is in place and people are provided with accessible, accurate information on their benefits. Scotland should also invest to improve public transport services and active travel infrastructure.

- Farming and nature. Long-term certainty is needed on public funding for farming practices and technologies to reduce emissions from managing crops and livestock. The Scottish Government should provide incentives and markets for farmers and land managers to diversify their incomes for actions including woodland creation, peatland restoration, agroforestry, and renewable energy.

- Engagement. The Scottish Government should work with the UK Government to develop the existing engagement strategy. This should provide clear, trusted information about the most impactful low-carbon choices for households and businesses in Scotland to reduce emissions, and the benefits of low-carbon choices, signposting to available sources of advice and support.

- Jobs and industry. The Scottish Government should continue to work with the UK Government to support the development of plans to develop CCS and hydrogen in the Scottish Cluster and work with the UK Government to develop new low-carbon industrial opportunities, such as those identified by Project Willow for Grangemouth. The Scottish Government should work with communities, workers, and businesses to develop proactive transition plans that enable access to secure employment and business opportunities that come with the Net Zero transition.

Next steps

The Committee provides advice but does not set policy. Decisions remain with the Scottish Government and the Scottish Parliament. As set out in the Act, the Scottish Government needs to lay draft regulations to set the carbon budgets within three months of receiving this advice. The Scottish Government must also lay before the Scottish Parliament a draft Climate Change Plan (CCP) containing its proposals and policies to meet legislated emissions reduction targets for the relevant period of the CCP within two months of the regulations setting the carbon budgets coming into force.

We are only 20 years away from 2045. To deliver the pathway to Scotland’s Net Zero target, immediate action is necessary. The First Carbon Budget begins next year and requires significant reductions in emissions across the economy. Many of the actions needed are in devolved areas, where the Scottish Government has substantial powers. With a new framework of carbon budgets in place, it is time for the Scottish Government to take action to drive emissions reductions, cut bills, and increase the resilience of the Scottish economy.

Chapter 1: Introduction

Introduction and key messages

This report sets out the Committee’s advice to the Scottish Government on the level of Scotland’s carbon budgets, covering the period 2026 to 2045, as required by the Climate Change (Scotland) Act 2009 (‘the Act’). Our advice is based on analysis underpinning our UK-wide Seventh Carbon Budget advice. That advice report contains more detail on the analysis.

This chapter summarises the latest scientific knowledge about climate change, sets out Scotland’s current targets under the Act, and summarises current emissions trends in Scotland.

Our key messages are:

- The Earth’s climate is changing rapidly as human-induced warming is increasing at an unprecedented rate. Risks are increasing – extreme weather events show the impact that climate change is already having, globally, in the UK, and in Scotland. Every 0.1°C of additional warming creates increasing threats from climate change.

- The science is clear that human activities have driven increases in greenhouse gases (GHGs) in the atmosphere to levels not previously experienced by our species. Long-term human-induced warming now reaches around 1.3ºC above pre-industrial levels and is rising at over 0.2ºC per decade.

- Net Zero CO2 emissions as well as deep reductions in other GHG emissions globally are required to halt further global warming. While it is now almost inevitable that warming levels will exceed 1.5ºC in the next ten years, it may still be possible to limit warming close to 1.5ºC in the longer term, provided deep global emissions cuts begin immediately.

- Global action must speed up. The UN Framework Convention on Climate Change (UNFCCC) process, the Paris Agreement, government policies, action from non-state actors, and market initiatives are driving progress. Global GHG emissions are likely near their peak, and on a per capita basis have begun to fall. But much more action is needed.

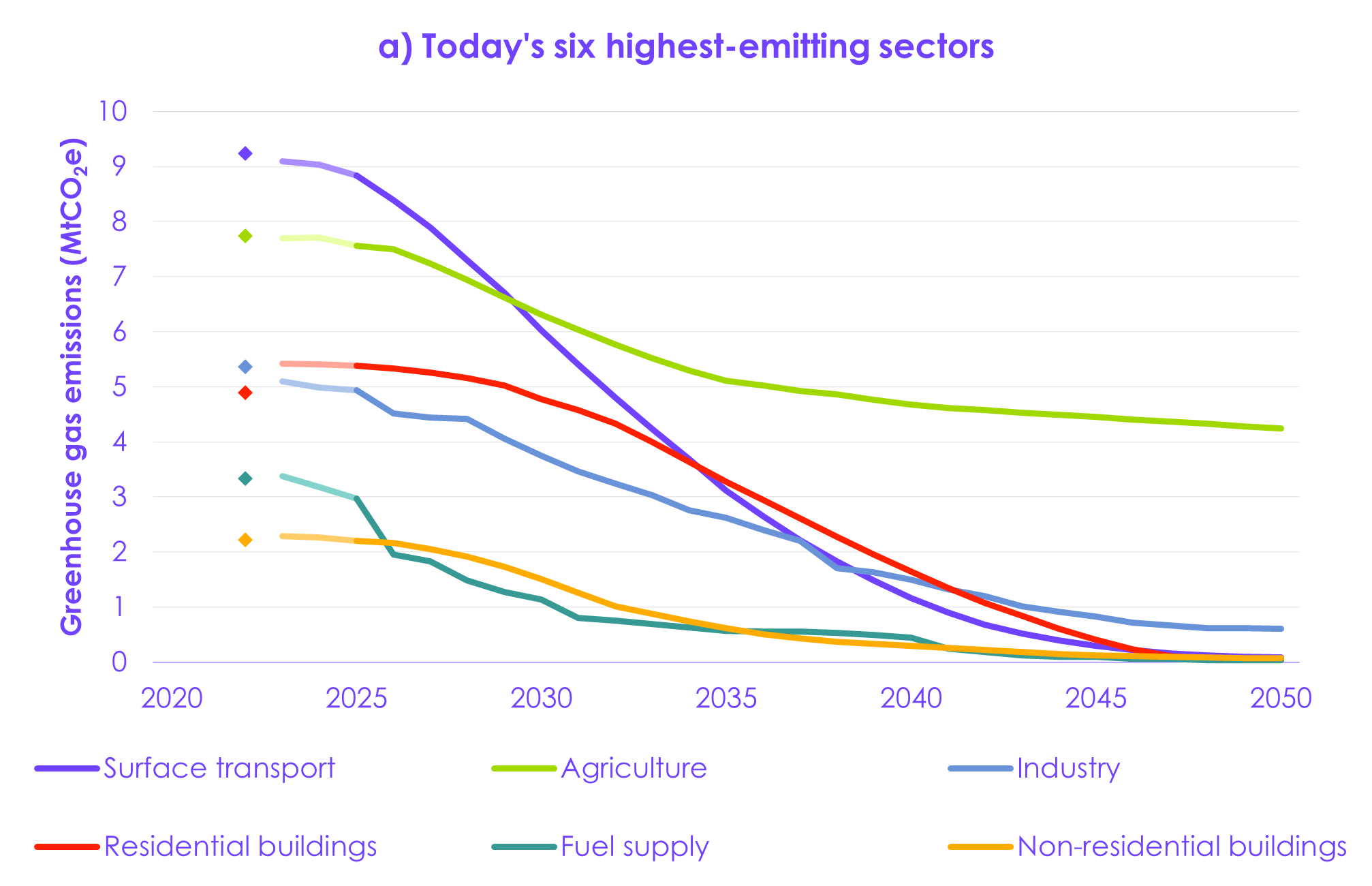

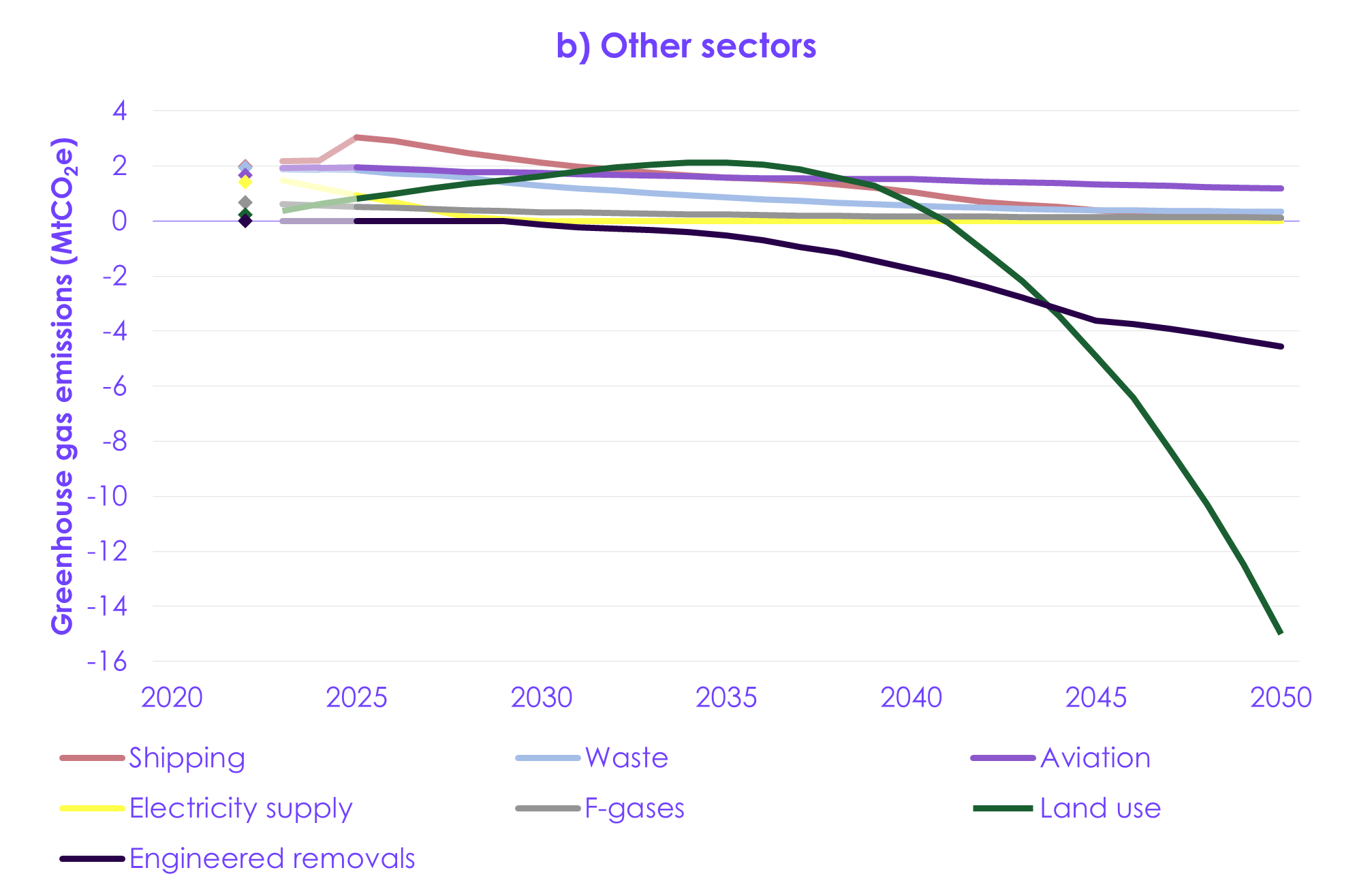

- Emissions in Scotland, including Scotland’s share of international aviation and shipping, have decreased by 50% since 1990.[3] The highest-emitting sectors in 2022 were surface transport, agriculture, industry, and residential buildings, with significant contributions from other sectors.

1.1 The latest scientific knowledge about climate change

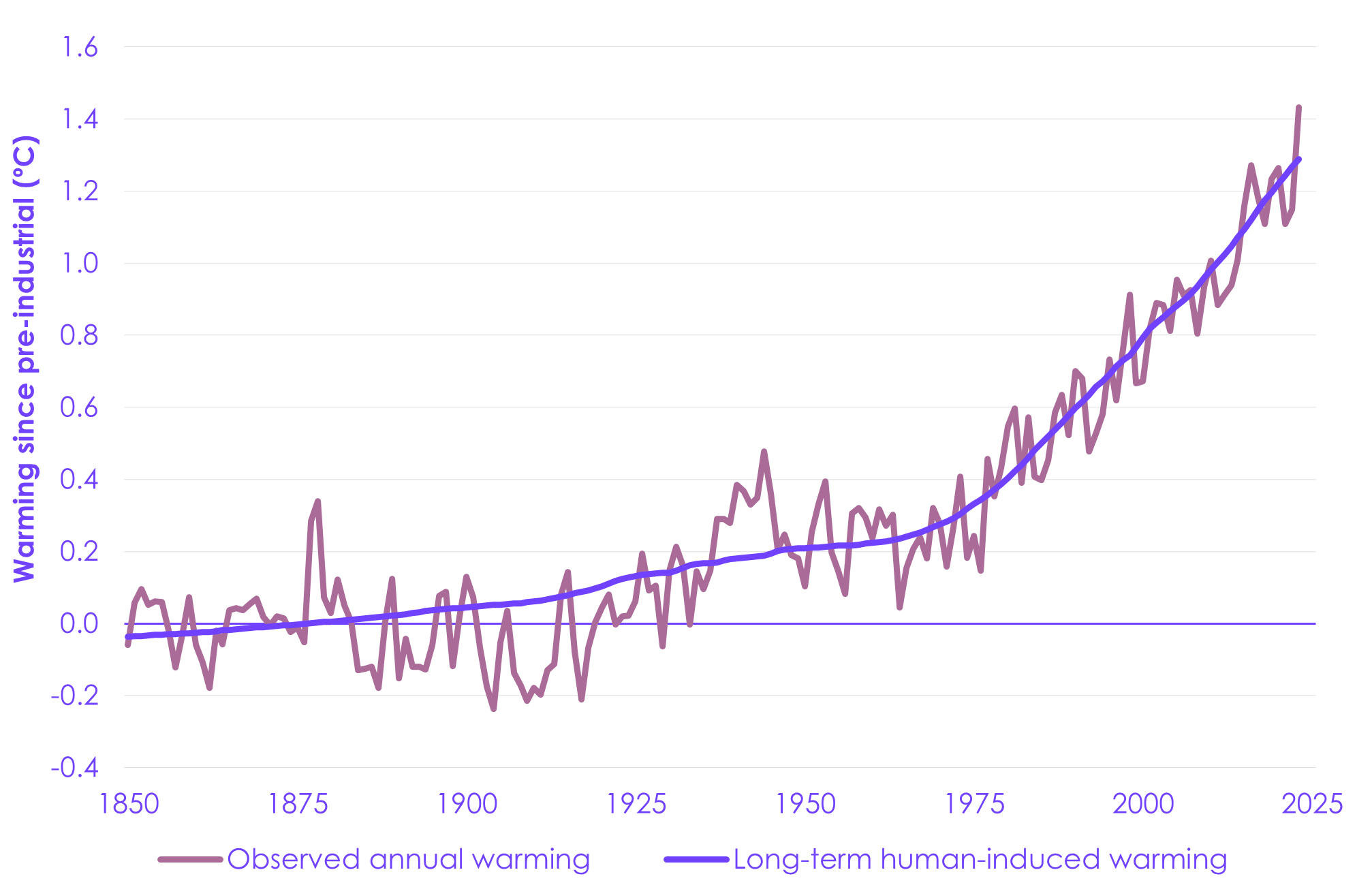

Global temperatures are rising (Figure 1.1). Since 2020, climate and weather records have continued to be broken around the world.

- Global temperatures have continued to increase. 2024 was the warmest year on record, at 1.6ºC above pre-industrial average levels.[4] Long-term human-induced global warming in 2023 is estimated to have risen to 1.3ºC (1.1 to 1.7ºC, 5th to 95th percentile range) above pre-industrial average levels.[5] The rate of increase is unprecedented, reaching 0.26°C per decade over 2014 to 2023.[6];[7]

- Records for climate and weather extremes continue to be broken. In 2023, ocean heat content reached its highest level in the 65-year observational record and global mean sea level reached a record high. Extreme weather events, such as wildfires and flooding, led to widespread loss of life and property destruction.[8]

- Warming will inevitably continue in the near term. Global temperatures will continue to rise until the point when the world reaches Net Zero CO2 emissions, with deep reductions in other GHGs also needed to limit warming.[9] This continued warming means that the world is rapidly approaching the lower end of the Paris Agreement long-term temperature goal (see Box 1.1).

|

Figure 1.1 Global average temperature rise |

|

Description: Since 1850, global average temperatures have been increasing, with a particular acceleration beginning around 1970. Observed annual temperatures fluctuate around long-term human-induced warming. |

| Box 1.1 Global warming of 1.5°C |

|

Long-term warming The 2015 Paris Agreement has a single long-term temperature goal: ‘holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels’. While not formally defined in the Agreement itself, the warming levels referenced in this goal are widely interpreted as referring to multi-decadal human-induced average warming, excluding short-term natural variability.[10] For simplicity, this is often referred to as ‘long-term warming’. Since 2015, advancing climate science has further highlighted risks of exceeding 1.5ºC of long-term warming. The UNFCCC Conference of the Parties (COP) has recognised these risks and put a greater focus on pursuing efforts to keep to 1.5°C above pre-industrial levels – such as in the agreed conclusions on the first Global Stocktake under the Paris Agreement which concluded in 2023. Long-term global warming, as measured according to this interpretation, has not yet exceeded 1.5ºC above pre-industrial levels, but it is rapidly approaching it. Estimates of current human-induced long-term warming are around 1.31ºC above pre-industrial levels and are rising at 0.26ºC per decade.[11] Short-term variability The Earth’s temperature also experiences short-term fluctuations on both annual and monthly timescales which can temporarily increase or lower global temperatures from the human-induced long-term average. A major contributor to this is the El Niño cycle – which occurs in the Pacific but has a large impact on global temperature. The large and persistent El Niño occurring over late 2023 and 2024 was one of the reasons that global average temperature anomalies have repeatedly, but temporarily, reached 1.5ºC or higher above pre-industrial levels. February 2023 to January 2024 was the first 12-month period where the mean global average temperature exceeded 1.5ºC above pre-industrial levels, and June 2024 marked the twelfth consecutive month to reach or surpass 1.5ºC warming.[12] 2024 was the warmest calendar year on record, surpassing 1.5ºC warming for the first time.[13] This does not mean that the long-term temperature goal of the Paris Agreement has been breached; limiting long-term warming to 1.5ºC remains a central goal in the UNFCCC process. Looking ahead While it is theoretically possible to return long-term warming to below 1.5ºC following a limited overshoot, every increment of global warming brings additional risks, both in terms of climate impacts and to the chances of bringing warming back down over time.[14]

|

1.1.2 Global emissions

There is a near-linear relationship between cumulative anthropogenic CO2 emissions and the global warming they cause. Continued emissions of CO2 and other long-lived GHGs therefore imply continued warming.[21]

Global GHG emissions grew steeply throughout the second half of the 20th century and have continued to grow over recent years, albeit at a slowing rate.

- Annual net global CO2 emissions from fossil fuels and land use, land use change, and forestry (‘land use’) in 2023 were around 41 GtCO2.[22] This makes 2023 emissions approximately joint highest in the modern record, with 2019.

- The rate of increase has slowed over the past decade. The rate of growth in global fossil CO2 emissions peaked at nearly 3% per year during the 2000s but has slowed in the last decade to less than 1% per year on average.[26]

- Various sources expect global emissions to peak this decade.

- The International Energy Agency and Bloomberg New Energy Finance both project an immediate or mid-2020s peak for energy sector CO2 emissions under current policy settings.[29];[30]

- The UNFCCC assesses that if countries implement their 2030 emissions targets in full, global GHG emissions will peak in the 2020s.[31]

1.1.3 Latest scientific understanding

The Intergovernmental Panel on Climate Change (IPCC) completed its Sixth Assessment Report (AR6) cycle in 2023. This brings together the last five years of scientific studies and provides the scientific basis for this report. It concluded that human activities have ‘unequivocally caused global warming’, and that limiting human-induced global warming to 1.5ºC requires deep, rapid, and sustained reductions in GHG emissions.

- Global temperatures are increasing as a result of human activities. The increase in average global surface temperatures has been driven by increases in GHG concentrations, which have unequivocally been caused by GHG emissions from fossil fuels and other human activities.

- Human-caused climate change is already affecting weather extremes across the globe. Evidence has strengthened linking human influence to observed changes in extremes such as heatwaves, heavy rainfall, droughts, and tropical storms. Human influence has also likely increased the chance of these events occurring simultaneously. Vulnerable communities are disproportionately affected by these extreme events.

- Risks increase as warming increases. Changes in extreme climate events become larger with every additional increment of warming. Concurrent extreme weather and sea level events are projected to become more frequent, storms to become more intense, and arid conditions to become more widespread. Abrupt and irreversible changes, including those triggered when tipping points are reached, become more likely and more impactful with further warming. For any given level of warming, many climate-related risks are assessed to be higher than in the IPCC’s previous assessments.

- Limiting human-caused warming requires deep and immediate emissions cuts. Modelled IPCC pathways that limit warming to 1.5°C (with low or no overshoot) reach global Net Zero CO2 in the early 2050s. These pathways see global GHG emissions peak by 2025 and assume deep and immediate cuts in emissions are made across most sectors this decade.

- Net Zero refers to a state in which GHG emissions entering the atmosphere are balanced by removals out of the atmosphere. Reaching Net Zero CO2 emissions globally is necessary for limiting global warming to any level. In most modelled scenarios, Net Zero global GHG emissions is associated with net negative global CO2 emissions (needed to balance residual non-CO2 emissions) and falling temperatures.[32]

- Limiting warming requires both limiting cumulative CO2 emissions and strong reductions in other GHGs. The IPCC has high confidence that the level of emissions reduction by 2030 will be key to determining whether warming can be limited to 1.5°C or 2°C.

- Global warming will continue to increase in the near term, as cumulative CO2 emissions continue to rise in all the IPCC’s modelled scenarios. Even under the IPCC’s very low emissions scenario, global warming is more likely than not to reach 1.5°C before 2040.

- Rapid action on mitigation and adaptation can reduce projected losses and damage. Actions this decade are crucial to reducing emissions quickly and adapting to the changing climate, since there are often long implementation times. Delaying action could also have other detrimental consequences, including risking lock-in to high-emissions infrastructure, stranded assets, and rising costs for people and businesses.

- The IPCC reports a 10–23% climate change-caused decline in annual global GDP by 2100 under a high warming scenario, though statistical approaches point towards the upper end of this range.[33];[34] Recent actuarial assessments emphasise the risk that losses could be considerably higher than currently considered in decision-making.[35];[36]

- Integrated responses that address both mitigation and adaptation objectives can take advantage of synergies and reduce trade-offs.

1.2 The UK and international context

Scotland reports on its progress towards the formal global agreements on climate change as part of the UK. However, Scotland’s ambition in climate change is also set in a broader context of other state, private sector, and non-state action against climate change.[37]

1.2.1 Global agreements on climate change

The UNFCCC process

The UNFCCC is the UN process for negotiating a global approach to address climate change. 197 countries plus the European Union are currently party to this process. Negotiations take place through the annual Conference of the Parties (COP). COP21 in 2015 negotiated the Paris Agreement, which is the latest global agreement on climate change mitigation.

- The Paris Agreement: this set several goals and objectives extending across mitigation, adaptation, and finance, including:

- A long-term temperature goal of limiting global warming to ‘well below 2ºC above pre-industrial levels’ and to ‘pursue efforts to’ limit warming to 1.5ºC above pre-industrial levels.

- On mitigation, setting three high-level milestones for global GHG emissions: global peaking as soon as possible, rapid reductions thereafter, and achieving a balance between emissions sources and sinks in the second half of this century (Net Zero GHGs).

- The UK has substantially reduced its emissions and has set targets consistent with reaching Net Zero emissions by 2050. Other developed economies such as the European Union are also committing to comparable targets (see Section 10.1.1 of the UK-wide Seventh Carbon Budget advice report for more detail).

- Nationally Determined Contributions: under the Paris Agreement, countries are required to submit Nationally Determined Contributions (NDCs). NDCs should set out ambitious targets and plans to reduce emissions in line with the aims of the Agreement.

- The UK set its first NDC to require a reduction in GHG emissions (excluding emissions from international aviation and shipping) of at least 68% by 2030, compared to 1990 levels.

- In January 2025, the UK submitted its second NDC, requiring at least an 81% reduction in GHG emissions by 2035, compared to 1990 levels. Both NDCs have been set in line with the Committee’s advice.

- Scotland reports on its international commitments formally to the UN as part of the UK-wide NDC.

- The Global Stocktake: the Paris Agreement established a five-yearly Global Stocktake to assess progress towards achieving its objectives. The first Global Stocktake concluded at COP28 in 2023 and highlighted significant gaps between current action and that needed to achieve the Agreement’s goals, notably (in the context of this advice) on mitigation.

- Reacting to the latest scientific evidence and political momentum built at COP26 and since, the Global Stocktake placed particular emphasis on the importance of 1.5ºC, underscoring that climate impacts would be much less severe than at 2ºC, and noting the gap between existing commitments and a 1.5ºC-consistent trajectory.

- The Global Stocktake set out several global objectives, including:

- A tripling of global renewable energy capacity and a doubling of the global average annual rate of energy efficiency improvements by 2030.

- Accelerating the phase-down of unabated coal power and transitioning away from fossil fuels, with particular focus on accelerated action this decade.

- Accelerating reductions in non-CO2 GHG emissions, including in particular methane by 2030.

- Accelerating deployment of low- and zero-emission technologies including zero-emission vehicles, renewables, nuclear, removals, and carbon capture technologies.

- Phasing out inefficient fossil fuel subsidies.

Global ambition and delivery

National Net Zero targets and ambitions now cover approximately 76% of present global GHG emissions.[38];[39];[40] Many of these targets are assessed as lacking detail and credibility, with short-term ambitions out of step with long-term goals.[41]

These targets are increasingly accompanied by policy packages designed to incentivise take-up of low-carbon technologies and boost domestic energy security and low-carbon competitiveness, albeit still falling short of alignment with NDC targets. Major low-carbon transition programmes (often with a notable electrification focus) are underway in the world’s largest economies.

Progress is being driven by improving economics of low-carbon technologies interacting with policy support. The global average cost for new electricity generation has fallen by 88% for solar PV and 60% for wind since 2010, with the global average cost of battery storage falling by nearly 90% over the same period.[42] The world now invests almost twice as much in clean energy as it does in fossil fuels, with clean energy investment expected to reach $2 trillion in 2024.[43]

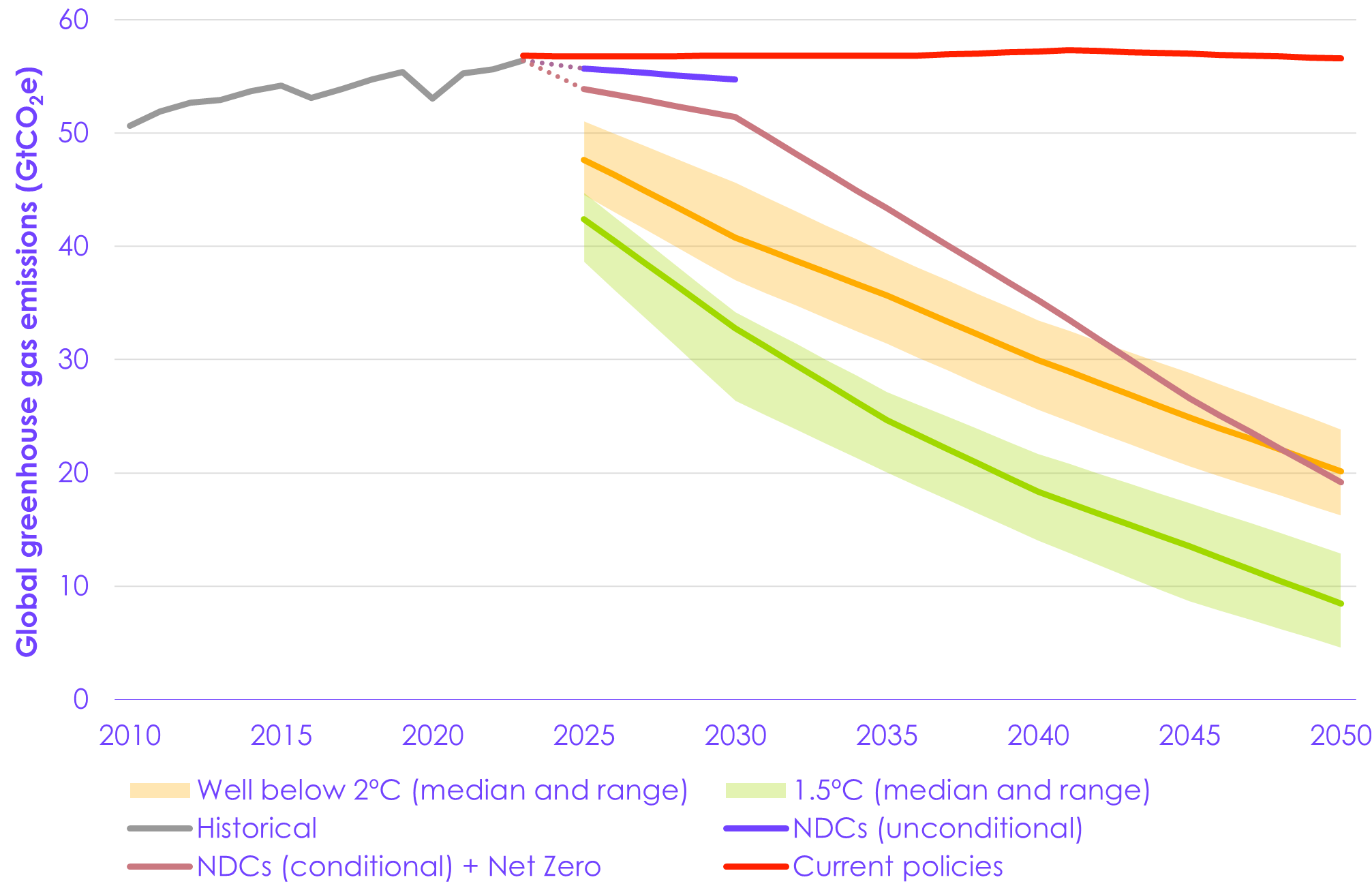

Globally, however, efforts remain significantly off track to achieve the Paris Agreement temperature goal (Figure 1.2).[44];[45]

- Global GHG emissions implied by NDCs are consistent with warming of around 2.5ºC by 2100 and would need to be 19–22 GtCO2e lower in 2030 than those implied by current NDCs to align with a 1.5ºC scenario. Current policies in turn fall short of what would be needed to deliver NDCs, implying warming of around 3ºC by 2100 and indicating an implementation gap on top of the ambition gap.[46];[47]

- Nonetheless, significant progress has been made in recent years. When major emitters’ Net Zero pledges are considered alongside NDCs, latest commitments imply warming below 2ºC if implemented in full (which countries are not currently on track to do), compared to the 3–4ºC projected before the Paris Agreement was adopted.[48]

|

Figure 1.2 Global GHG emissions under current ambition, compared to Paris-aligned trajectories |

|

|

1.2.2 The Climate Change Act and UK carbon budgets

The Climate Change Act (2008) is the UK’s legal framework for tackling and responding to climate change. The UK Climate Change Act sets in law a long-term goal of reaching Net Zero UK GHG emissions by 2050 as well as intermediate steps defined by the level of carbon budgets, which set legally binding caps on UK GHG emissions over five-year periods. These make clear the required level of emissions reduction in the short and medium term to ensure the UK is on track to decarbonise by 2050.

- Emissions in Scotland are covered by the UK Climate Change Act, and therefore contribute to the UK’s carbon budgets and long-term emissions reduction goal.

- The UK has approximately halved its emissions since 1990 and has met all of its three carbon budgets so far.

The next three steps on the way to Net Zero for the UK are the Fourth, Fifth and Sixth Carbon Budgets, covering the periods 2023 to 2027, 2028 to 2032, and 2033 to 2037. These have been legislated, while the UK-wide Seventh Carbon Budget, covering the period 2038 to 2042, is due to be legislated by 30 June 2026.

1.3 The Climate Change (Scotland) Act

Evidence of climate change is visible around the world, including in Scotland. Scotland’s annual average temperature over 2013 to 2022 was around 0.65°C warmer than it was around 30 years ago (an average of the 1981 to 2000 period).[49] In 2022, Scotland recorded its highest ever temperature of nearly 35°C in the Scottish Borders, impacting health, ecosystems, and infrastructure.[50] In 2023, prolonged rainfall followed by Storm Babet led to widespread flooding and several deaths, as well as substantial disruption to transport and power systems. Some areas in Angus and Aberdeenshire saw over 150 mm of rainfall in 36 hours.[51] Research has found that this rainfall was made about 20% heavier by human-caused climate change.[52]

The Climate Change (Scotland) Act 2009 sets the framework for the Scottish Government to address climate change. Emissions in Scotland are covered by both Scotland’s targets, set under the Act, and UK-wide targets, set under the UK Climate Change Act (2008) and as part of the UNFCCC process (see Section 1.2.2).

- The Act was amended in 2019 to include an ambitious target to reach Net Zero greenhouse gas emissions by 2045 and interim decadal emissions targets for 2020, 2030, and 2040.[53]

- In our 2023 Progress in reducing emissions in Scotland report, we advised that the acceleration required in emissions reduction to meet the 2030 target was beyond what is credible. The Act was amended in 2024 to repeal the interim targets and introduce five-yearly carbon budgets aligned with the 2045 Net Zero target.[54]

- Emissions from international aviation and shipping are included in these targets.

This report provides our advice on four carbon budgets for Scotland, covering the period from 2026 to 2045. As set out in the Act, the Scottish Government needs to lay draft regulations to set the carbon budgets within three months of receiving this advice. The Scottish Government must also lay before the Scottish Parliament a draft Climate Change Plan (CCP) containing its proposals and policies to meet legislated emissions reduction targets for the relevant period of the CCP within two months of the regulations setting the carbon budgets coming into force.

We have previously set out recommendations to the Scottish Government on key considerations for the upcoming CCP (see Box 1.2).

| Box 1.2 Recommendations for the upcoming Climate Change Plan |

|

In the Committee’s 2023 Progress in reducing emissions in Scotland report, we included priority recommendations setting out key considerations for the Climate Change Plan (CCP):

In a letter to Màiri McAllan MSP, Cabinet Secretary for Net Zero and Just Transition dated 14 May 2024 on the design and implementation of carbon budgets in Scotland, the Committee advised that the Scottish Government should develop a monitoring and evaluation plan that can be used to identify where there are risks of delivery falling behind the pace of change that is required.

|

The target-setting criteria

The Act requires the Committee to provide advice on Scotland’s carbon budgets taking into account the target-setting criteria. Table 1.1 sets out how we have considered the target-setting criteria in this advice.

| Table 1.1 Alignment with the target-setting criteria |

|

| Criterion |

How the Committee has considered the criterion |

| The fair and safe Scottish emissions budget | Scotland’s 2045 Net Zero target represents Scotland’s fair contribution to the UK-wide target and hence to the Paris Agreement (see Section 2.2.1). We recommend carbon budgets that are deliverable and consistent with the Net Zero targets for Scotland and the UK (see Section 2.2.2). We then determine the fair and safe Scottish emissions budget that is compatible with the Net Zero target and the recommended carbon budgets (see Section 2.2.3). |

| European and international law and policy relating to climate change | See Section 1.2.1 for how this advice considers global agreements on climate change. |

| Scientific knowledge about climate change | See Section 1.1 for how this advice considers the latest scientific knowledge about climate change. |

| Technology relevant to climate change | See Section 3.2 for how this advice considers key low-carbon technologies in the pathway to Net Zero emissions. |

| Economic circumstances | See Section 4.2 for how this advice considers economic circumstances in Scotland, including the likely impact of the carbon budgets on the Scottish economy, the competitiveness of particular sectors of the Scottish economy, small- and medium-sized enterprises, and jobs and employment opportunities. |

| Fiscal circumstances | See Section 4.3 for how this advice considers fiscal circumstances in Scotland, including the likely impact of the carbon budgets on taxation, public spending, and public borrowing. |

| Social circumstances | See Section 4.3 for how this advice considers social circumstances in Scotland, including the likely impact of the carbon budgets on those living in poorer or deprived communities. |

|

Impact on public health |

See Section 4.3 for how this advice considers the impact of the carbon budgets on public health in Scotland. |

|

Impact on remote rural communities and island communities |

See Section 4.3 for how this advice considers the impact of the carbon budgets on those living in remote rural communities and island communities in Scotland. |

|

Energy policy |

See Section 3.2.10 for how this advice considers the impact of the carbon budgets on energy supplies, the renewable energy sector, and the carbon and energy intensity of the Scottish economy. |

|

Environmental considerations |

See Section 3.2.2 for how this advice considers the likely impact of the carbon budgets on the environment, including on biodiversity in Scotland. |

|

Impact on sustainable development |

The carbon budgets will contribute to sustainable development in Scotland, particularly Sustainable Development Goal (SDG) 13 (Climate Action). The carbon budgets will also contribute to SDGs:

|

|

Current international carbon reporting practice |

This advice is consistent with current international carbon reporting practice under the protocols to the UNFCCC. See Section 1.2.1 for how this advice considers global agreements on climate change. |

1.4 Current emissions in Scotland

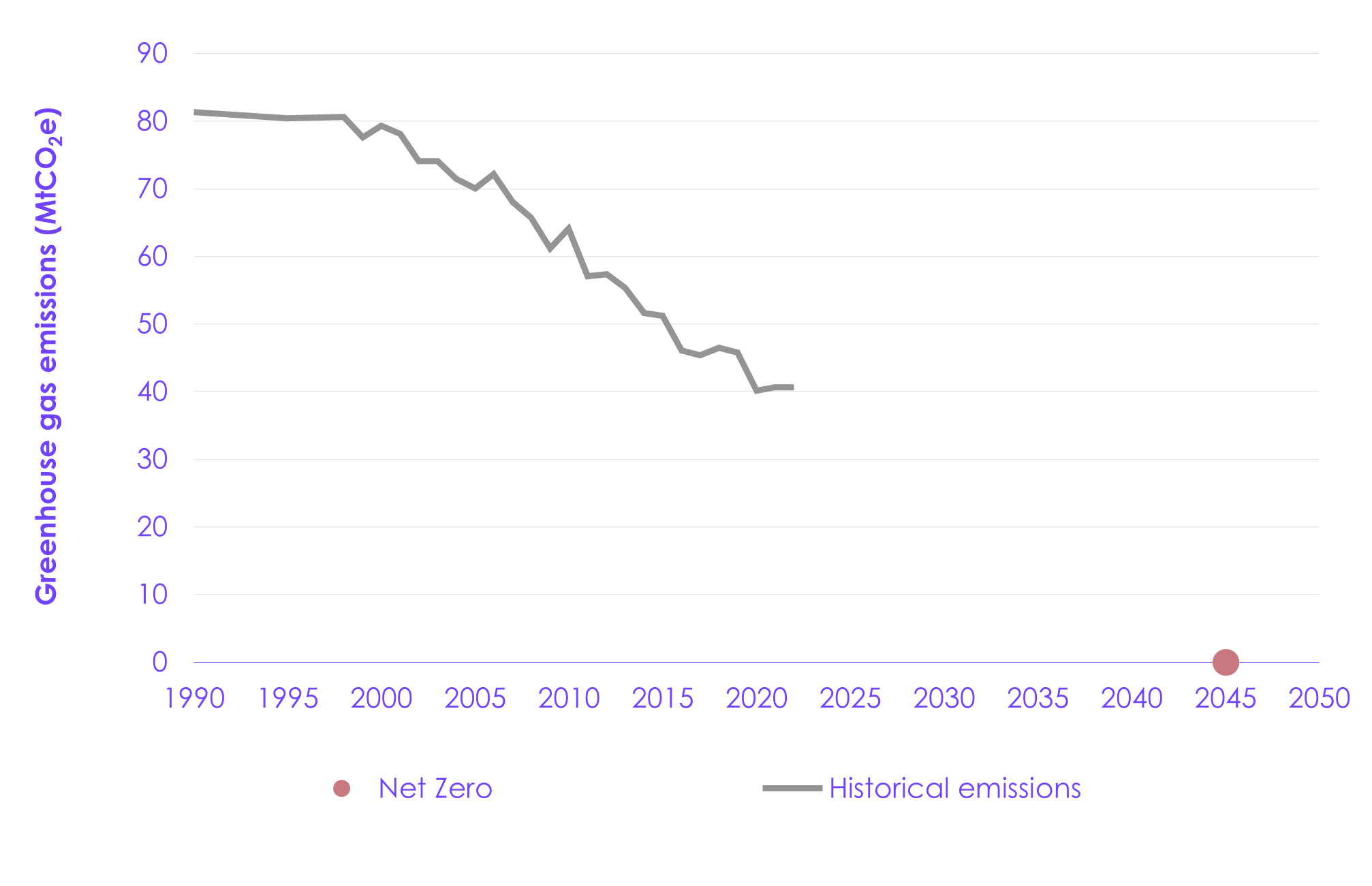

Emissions in Scotland, including Scotland’s share of international aviation and shipping, were 40.6 MtCO2e in 2022, the most recent year for which data are available (Figure 1.3).

- Emissions have fallen by 50% since 1990. Emissions were relatively constant between 1990 and 2000 but have since fallen by around 1.8 MtCO2e per year between 2000 and 2022 on average.

- So far, emissions reductions have been driven by the electricity supply and industry sectors due to the phase-out of coal, the ramp-up of renewable electricity generation, and a structural shift towards less carbon-intensive, higher value industrial output. There have also been significant reductions in the land use sector.

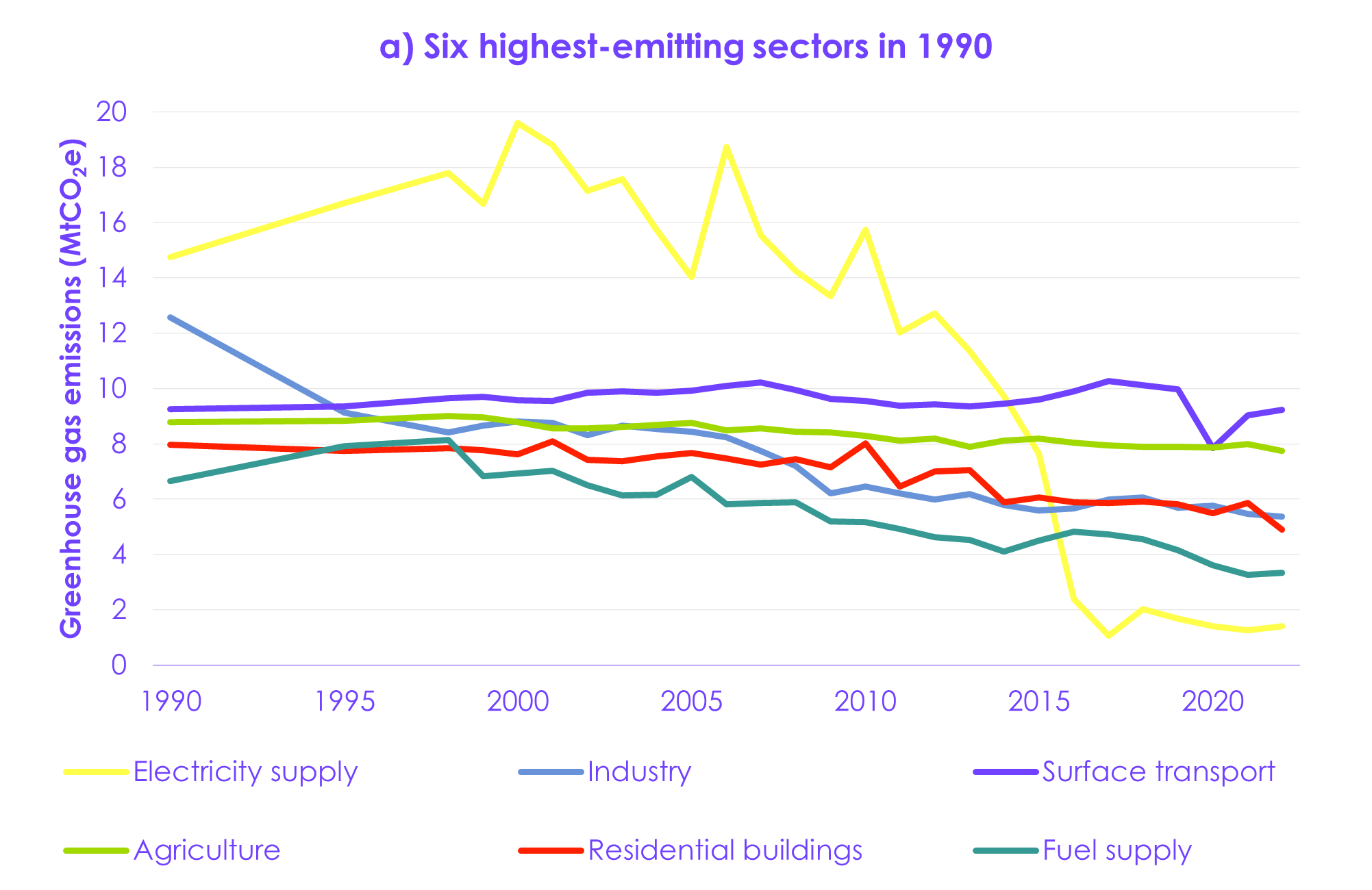

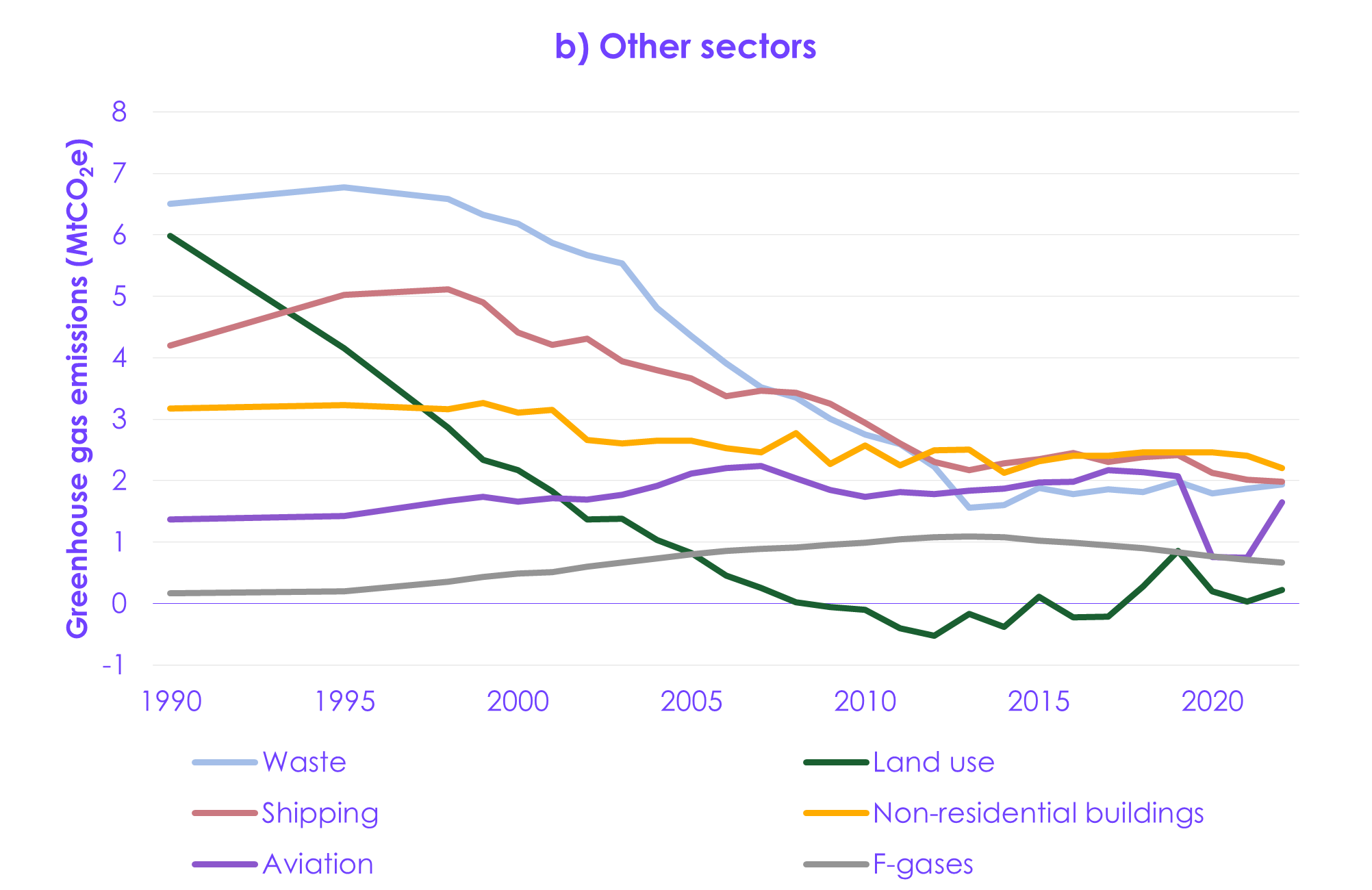

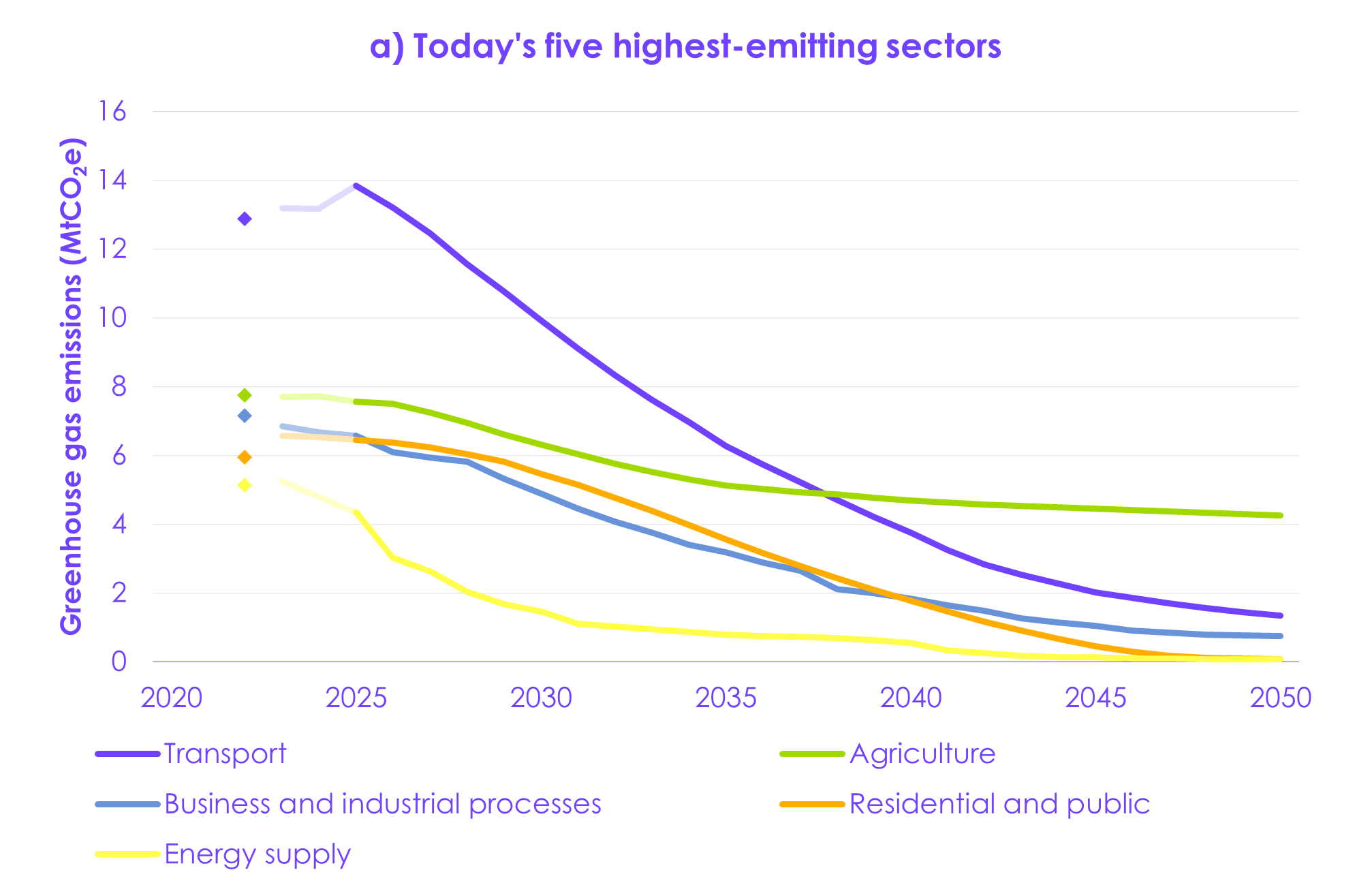

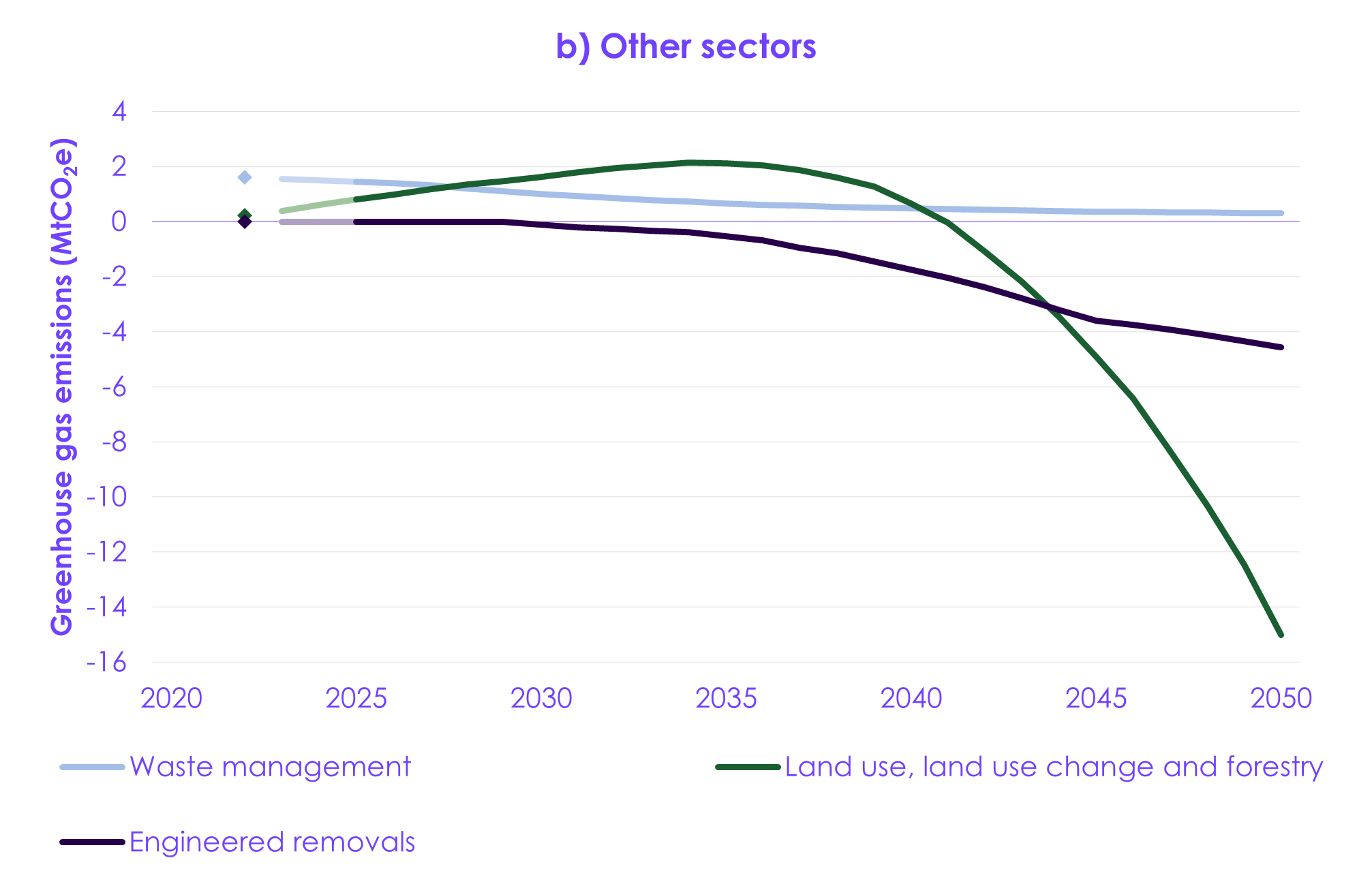

- The highest-emitting sectors in 2022 were surface transport, agriculture, industry, and residential buildings, with significant contributions from other sectors (Figure 1.4).[55]

|

Figure 1.3 Scotland’s historical emissions and current targets |

|

|

|

Figure 1.4 Scotland’s historical emissions by sector |

|

|

Chapter 2: Scotland’s path to Net Zero

Introduction and key messages

This chapter sets out our recommended level for Scotland’s carbon budgets. Our recommendation is based on our Balanced Pathway for Scotland from 2025 to Net Zero by 2045.

Our key messages are:

- Scotland’s target to achieve Net Zero by 2045 represents a fair contribution towards UK and global efforts under the Paris Agreement to limit global average temperatures. It is appropriate that Scotland’s target is earlier than the UK-wide target, because Scotland has proportionally more land suitable for tree planting and higher potential for engineered removals.

- The Committee recommends that Scotland’s carbon budgets, including Scotland’s share of international aviation and shipping emissions, are set at annual average levels of emissions that are:

- 57% lower than 1990 levels for the First Carbon Budget (2026 to 2030).

- 69% lower than 1990 levels for the Second Carbon Budget (2031 to 2035).

- 80% lower than 1990 levels for the Third Carbon Budget (2036 to 2040).

- 94% lower than 1990 levels for the Fourth Carbon Budget (2041 to 2045).[56]

- The Scottish Government should plan to deliver the emissions reductions required to meet the carbon budgets through domestic decarbonisation action within Scotland and should not plan to use international credits (referred to as ‘carbon units’ in the Act) to achieve the carbon budgets.

- The definition of removals in the Act currently only refers to land-based removals. However, engineered removals are needed to achieve Scotland’s 2045 Net Zero target. The Scottish Government should amend the Act (which can be done by order) to extend the definition of removals to include engineered removals when legislating the carbon budget targets.

- Scotland will need to resume the pace of emissions reduction that was seen between 2009 and 2016 in order to meet the recommended carbon budgets, with contributions broadening to more sectors across the economy. Achieving this will depend largely on ramping up deployment of solutions that are available today. Electrification of key technologies is the key driver of the emissions reduction required to achieve the carbon budgets.

- The Scottish Government has devolved powers to deliver the necessary emissions reductions in key sectors, particularly buildings, surface transport, agriculture, and land use.

- The overall cost of meeting the Balanced Pathway for Scotland is estimated to be around £750 million per year on average between 2025 and 2050, relative to a baseline of no further decarbonisation action. This is around 0.4% of Scotland’s GDP.

2.1 The Balanced Pathway for Scotland

2.1.1 Developing our Balanced Pathway

Our advice on Scotland’s carbon budgets is based on our Balanced Pathway, which represents the Committee’s assessment of an ambitious but deliverable pathway for Scotland to reach Net Zero by 2045. The pathway is not prescriptive but illustrates a feasible and cost-effective route to achieve Scotland’s Net Zero target.

- Our pathway includes all greenhouse gases (GHGs) and covers the period 2025 to 2050. It includes Scotland’s share of international aviation and shipping emissions.

- The pathway is aligned with Scotland’s contribution to the UK’s Balanced Pathway, which we presented in our 2025 UK-wide Seventh Carbon Budget advice. The UK’s Balanced Pathway represents our assessment of a pathway to Net Zero UK GHG emissions that is based on actions that are feasible and cost effective across the UK and takes into account the different resources, opportunities, and costs seen in different parts of the UK.

- Scotland reaches Net Zero by 2045 in our pathway but the transition to low-carbon technologies continues beyond 2045. For example, technologies such as electric vehicles (EVs) and heat pumps continue to replace high-carbon alternatives out to 2050, in line with UK-wide deployment rates.

- Scotland’s greater potential for land-based and engineered removals allows negative emissions to grow proportionately faster than in the rest of the UK, offsetting remaining emissions by 2045.

- The Scottish Government could choose to reduce the remaining emissions in some sectors more quickly than in our pathway (see Section 3.3).

- The Balanced Pathway is presented compared to a baseline pathway of no further decarbonisation action.[57] This allows us to calculate the required abatement, investment needs, costs, and cost savings associated with the future actions to reduce Scotland’s GHG emissions. See Chapter 2 of our UK-wide Seventh Carbon Budget advice for further details on our baseline and the general approach we take to developing emissions pathways.

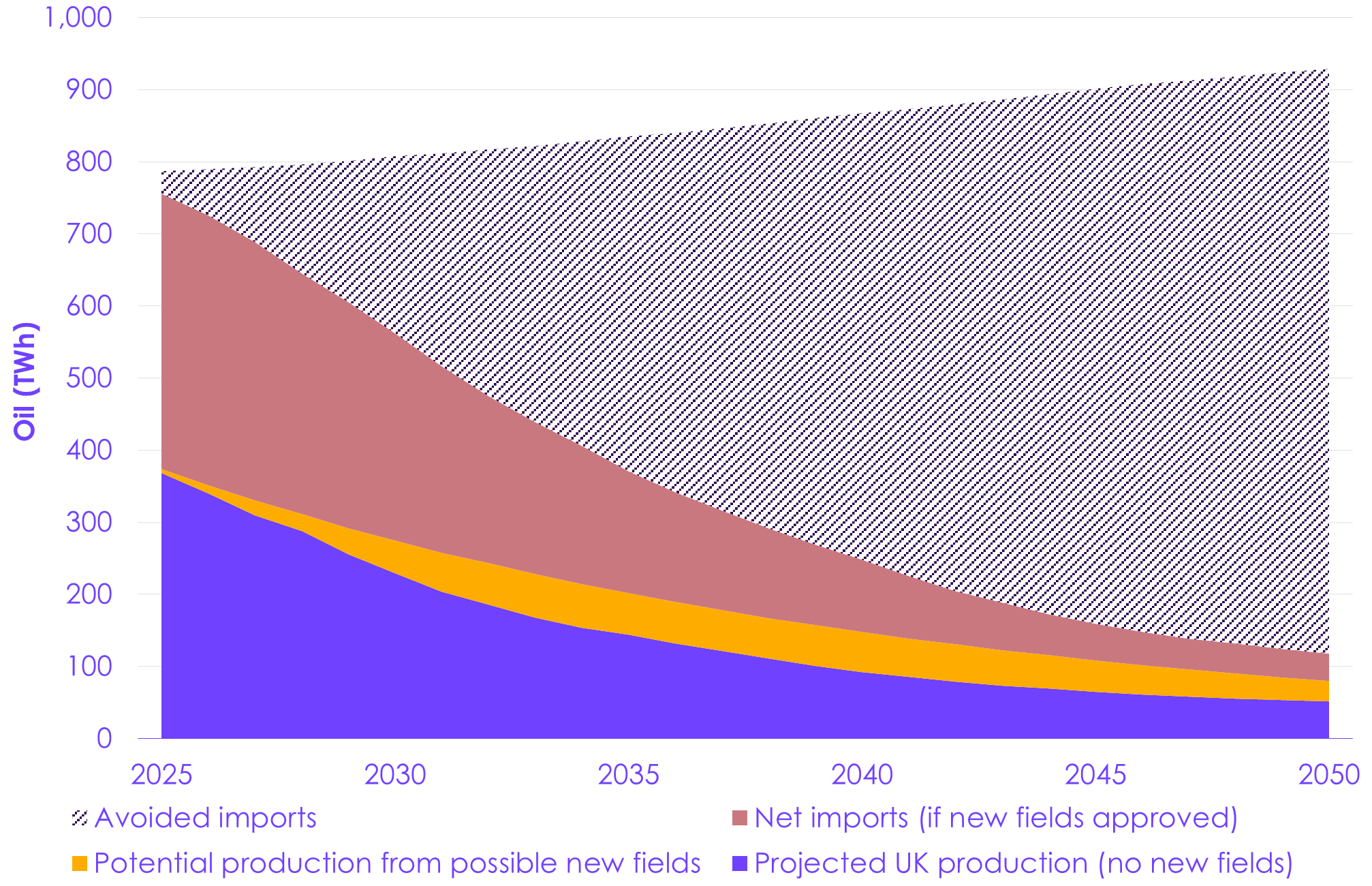

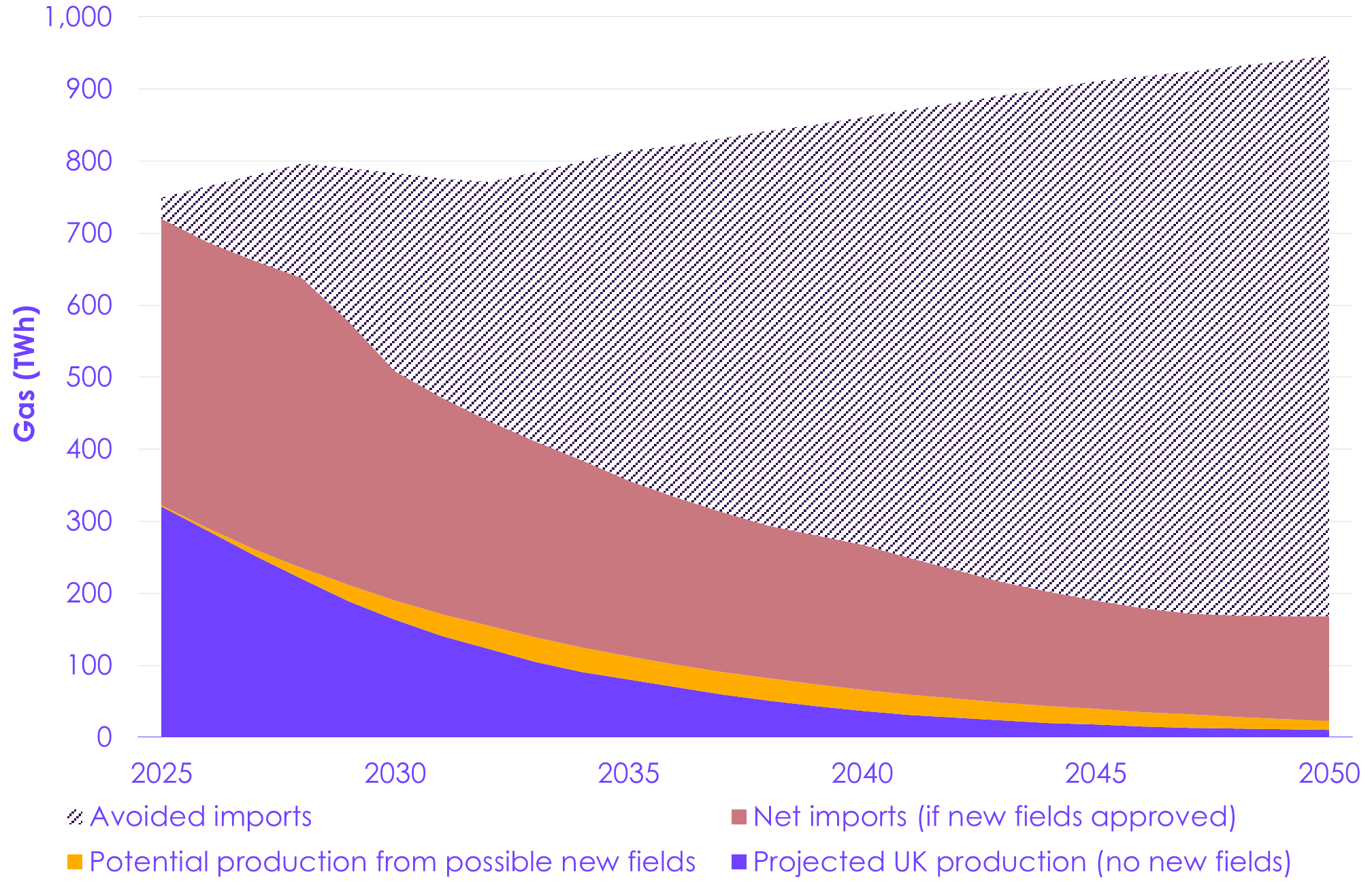

- Emissions in the baseline increase between 2022 and 2040 due to growth in population, which peaks in Scotland in 2033, and GDP.[58] After 2040, emissions fall slightly due to increasing sequestration from tree planting, which is assumed in the baseline to continue at current rates, and a reduction in emissions in fuel supply, largely due to the decline of North Sea oil and gas reserves.

2.1.2 Emissions in the Balanced Pathway

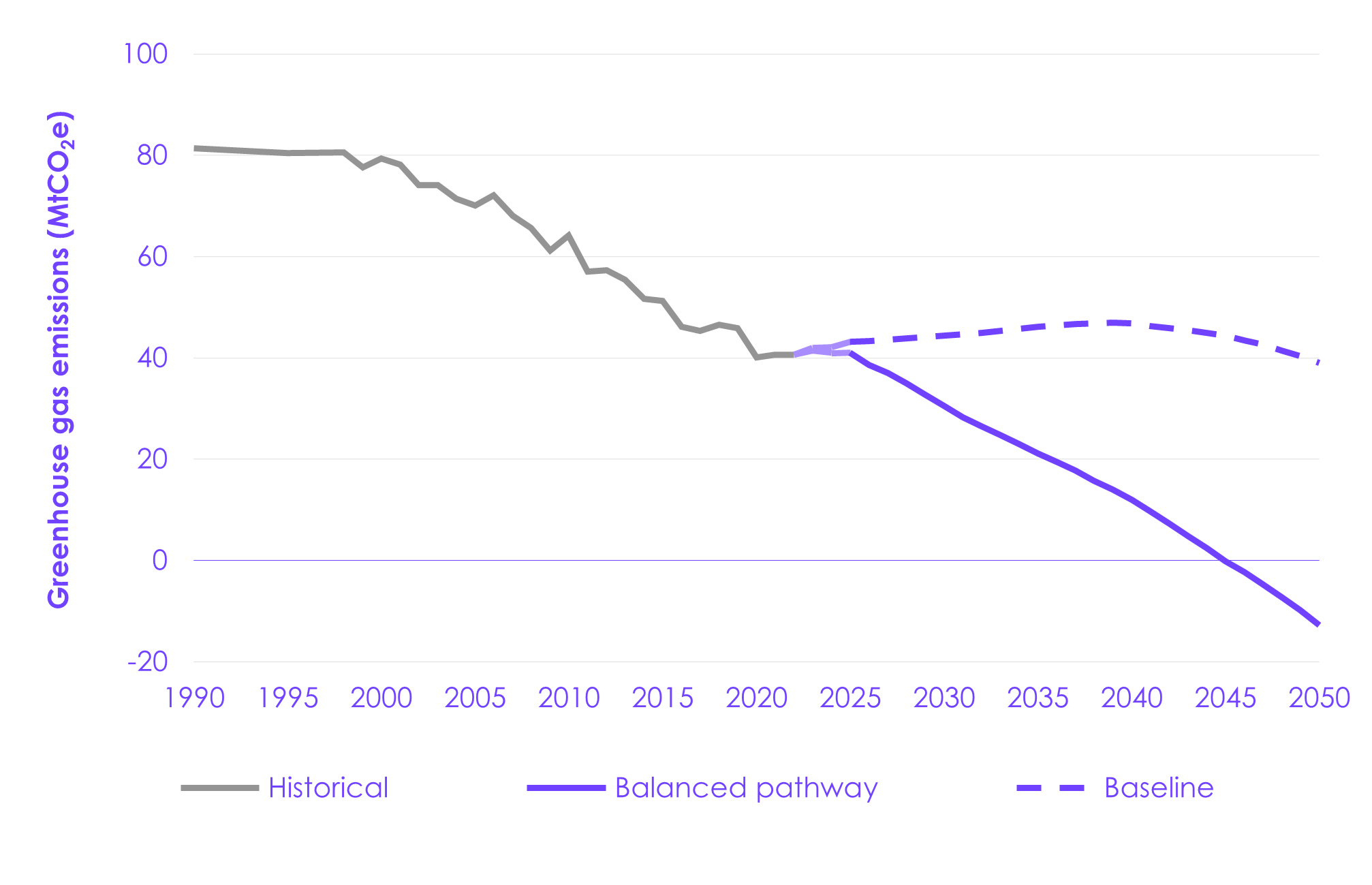

Emissions in Scotland have fallen by 50% between 1990 and 2022.

- In the Balanced Pathway, emissions need to fall by around 2.1 MtCO2e per year on average between 2025 and 2045 (Figure 2.1). This is similar to the pace previously seen between 2009 and 2016, but emissions reductions now need to broaden to more sectors across the economy, particularly buildings, surface transport, agriculture, and land use (see Section 3.2). The Scottish Government has substantial devolved powers to deliver the necessary emissions reductions in these key sectors.

- Much of this reduction will come from technologies and choices that are available today and can be deployed quickly (see Section 2.3.2). This emphasises the importance of putting the conditions in place to enable low-carbon markets and choices to scale up quickly.

|

Figure 2.1 The Balanced Pathway to Net Zero and the carbon budgets in Scotland |

|

|

2.2 Scotland’s emissions targets

2.2.1 Performance against previous and existing future emissions targets

Scotland’s Net Zero target

The Balanced Pathway meets Scotland’s Net Zero target, reaching Net Zero GHG emissions in 2045.

- The UK’s 2050 Net Zero target was set to deliver the UK’s commitments under the Paris Agreement, in line with the Committee’s 2019 Net Zero advice. It represents a fair contribution towards limiting the rise in global average temperature to ‘well below 2°C above pre-industrial levels’ and to ‘pursue efforts to’ limit warming to 1.5ºC above pre-industrial levels.

- Scotland’s Net Zero target represents a feasible and fair contribution for Scotland to the UK-wide target and hence to the Paris Agreement. Scotland’s target is earlier because there is proportionally more land suitable for tree planting and higher potential for engineered removals in Scotland than the rest of the UK.

- This means that 38% of the new woodland created in our UK-wide pathway between 2025 and 2050 is in Scotland.

- As a result, Scotland’s land use sink scales up more quickly than in the rest of the UK, offsetting residual emissions from the agriculture sector five years sooner than in our UK-wide analysis (see Section 2.4).

- Scotland has natural advantages which favour development of engineered removals via direct air carbon capture and storage (DACCS), notably abundant renewable generation, particularly from wind, and proximity to large geological storage locations.

- A credible share of UK-wide engineered removals is then sufficient to balance residual emissions from sectors other than agriculture, demonstrating that the 2045 Net Zero target for Scotland is appropriate and achievable (see Section 2.4). There may be scope for a slightly lower dependence on engineered removals if Scotland were to eliminate emissions in other sectors, such as surface transport and buildings, more quickly than in our UK-wide analysis (see Section 3.3).

Previous interim targets

Amendments to the Act in 2019 introduced interim emissions targets to reduce emissions by 75% on 1990 levels by 2030 and by 90% on 1990 levels by 2040. These interim targets were repealed through amendments to the Act in 2024, which replaced them with a carbon budgets framework aligned with the 2045 Net Zero target.

When setting carbon budget regulations, the Act requires Scottish Ministers to state in which carbon budget period they expect these 75% and 90% emissions reduction milestones to be achieved.

In the Balanced Pathway, these percentage reductions are reached in 2036 (during the Third Carbon Budget period) and 2042 (during the Fourth Carbon Budget period), respectively.

2.2.2 Recommended levels of Scotland’s carbon budgets

Table 2.1 sets out the recommended levels of Scotland’s carbon budgets, including Scotland’s share of international aviation and shipping emissions. Scotland’s carbon budgets are expressed as annual average levels of emissions below the 1990 baseline.[59]

| Table 2.1 Recommended levels of Scotland’s carbon budgets |

|

| Carbon budget period | Annual average level of GHG emissions for the relevant period below 1990 levels |

| First Carbon Budget (2026–2030) | 57% |

| Second Carbon Budget (2031–2035) | 69% |

| Third Carbon Budget (2036–2040) | 80% |

| Fourth Carbon Budget (2041–2045) | 94% |

| Notes: The recommended budget levels are in line with the average reduction in emissions in the Balanced Pathway over each five-year carbon budget period compared to 1990 levels, rounded down to the nearest percentage point. | |

These recommended carbon budgets would require around half of the emissions reductions compared to 2022 levels to happen between now and 2035, with the remaining half in the decade from then to 2045 (Figure 2.2).

The Scottish Government should plan to deliver the emissions reductions required to meet the carbon budgets through domestic decarbonisation action within Scotland and should not plan to use international credits (referred to as ‘carbon units’ in the Act) to achieve the carbon budgets.

Under the Act, the Committee is required to provide advice on whether an aviation multiplier to reflect the direct and indirect non-CO2 climate change impacts of emissions at altitude from international aviation is appropriate. We continue to recommend that Scottish targets do not take non-CO2 effects into account (i.e. the multiplier should be set at one) (see Box 3.2).

- The exact quantitative role that non-CO2 effects play in global warming is still too uncertain to explicitly include in Scottish targets. It would also be inconsistent with the approach taken across the rest of the UK.

- In line with our UK-wide Seventh Carbon Budget advice to the UK Government, the Scottish Government should work with the UK Government to ensure that the cost of aviation mitigating its emissions is reflected in the cost to fly, start monitoring non-CO2 effects of aviation, and set a minimum goal of no further warming after 2050 from non-CO2 effects.

- In our modelling, the UK Government’s high carbon value is included in the cost of flying used to forecast future demand. We use the high, rather than central, value to account for non-CO2 effects.

|

Figure 2.2 The recommended carbon budgets for Scotland |

Description: The Balanced Pathway sets the recommended level of Scotland’s carbon budgets. Source: National Atmospheric Emissions Inventory (2024) Greenhouse Gas Inventories for England, Scotland, Wales & Northern Ireland: 1990-2022; CCC analysis. Notes: (1) Our pathway and baseline are modelled using historical data up to 2022. Emissions reductions prior to 2025 are based largely on existing trends; additional decarbonisation measures only begin to be applied in our modelling after 2025. (2) ‘CB’ refers to Scottish carbon budgets: ‘CB1’ refers to the First Carbon Budget; subsequent numbers refer to subsequent carbon budgets. (3) Our pathway for shipping begins above the latest historical data mainly because, from 2025, we have based our estimate of shipping emissions on the UK Department for Transport’s emissions model, which uses more recent activity data for domestic shipping and as a result gives a higher estimate of current shipping emissions than the GHG inventory. (4) There was a significant drop in emissions from residential buildings between 2021 and 2022 due to warmer-than-average winters and record high energy prices. Our pathway assumes that some of this reduction was a direct response to the weather and prices and will therefore only be short-term. Therefore, emissions in our pathway increase between 2022 and 2025. (5) Emissions from aviation increase between 2022 to 2025 due to a rebound in demand following the COVID-19 pandemic. |

2.2.3 Recommended level of the fair and safe emissions budget

The Act defines the fair and safe Scottish emissions budget as the aggregate amount of net Scottish emissions of GHGs for the period 2010 to 2050 as recommended as being consistent with Scotland, in line with the principles set out in Article 3 of the United Nations Framework Convention on Climate Change (UNFCCC), contributing appropriately to the holding of the increase in global average temperature to well below 2°C above pre-industrial levels, and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels.

Scotland’s 2045 Net Zero target represents Scotland’s fair contribution to the UK-wide target and hence to the Paris Agreement (see Section 2.2.1). We recommend carbon budgets that are deliverable and consistent with the Net Zero target (see Section 2.2.2). We then determine the fair and safe Scottish emissions budget that is compatible with the Net Zero target and the recommended carbon budgets.

- The Committee recommends that the fair and safe budget for the period 2010 to 2050 should be set at 1,129 MtCO2e.

- This assumes that emissions between 2045 and 2050 are negative, which is feasible as Scotland has proportionally more land suitable for tree planting and higher potential for engineered removals than the rest of the UK. Net negative emissions in Scotland between 2045 and 2050 are part of Scotland’s fair contribution to our UK-wide Balanced Pathway, in order to achieve Net Zero by 2050 across the UK.

2.2.4 Contribution to meeting the UK’s emissions targets

The pace of emissions reductions in Scotland is lower than the pace required across the UK over the first three Scottish carbon budget periods, but faster over Scotland’s Fourth Carbon Budget period (Table 2.2).

- The exact pace of decarbonisation in each sector compared to the UK will vary, as we have considered Scotland’s specific circumstances in our pathway (see Section 3.1.3).

- The overall trend reflects the trend in the land use sector, where emissions reductions are proportionally slower over the first three Scottish carbon budget periods in Scotland than across the UK. However, over Scotland’s Fourth Carbon Budget period, land-based removals ramp up proportionally more quickly in Scotland than across the UK. This is because Scotland has proportionally more tree planting than the rest of the UK, which in the short term increases soil emissions as new woodlands are planted. This is then offset by sequestration as the trees grow.

- Engineered removals via DACCS ramp up more quickly in Scotland than in the rest of the UK, reflecting natural advantages such as abundant renewable generation, particularly from wind. We largely assume that engineered removals are funded in line with a ‘polluter pays’ principle, in which case these costs would fall UK-wide rather than necessarily to people in Scotland.

| Table 2.2 Emissions reductions in Scotland’s recommended carbon budgets compared to the UK Balanced Pathway |

||

| Scottish carbon budget period | Annual average level of emissions below 2022 levels for the period for Scotland | Annual average level of emissions below 2022 levels for the period for the UK |

| First Carbon Budget (2026–2030) |

14% | 21% |

| Second Carbon Budget (2031–2035) |

39% | 48% |

| Third Carbon Budget (2036–2040) |

61% | 69% |

| Fourth Carbon Budget (2041–2045) |

88% | 85% |

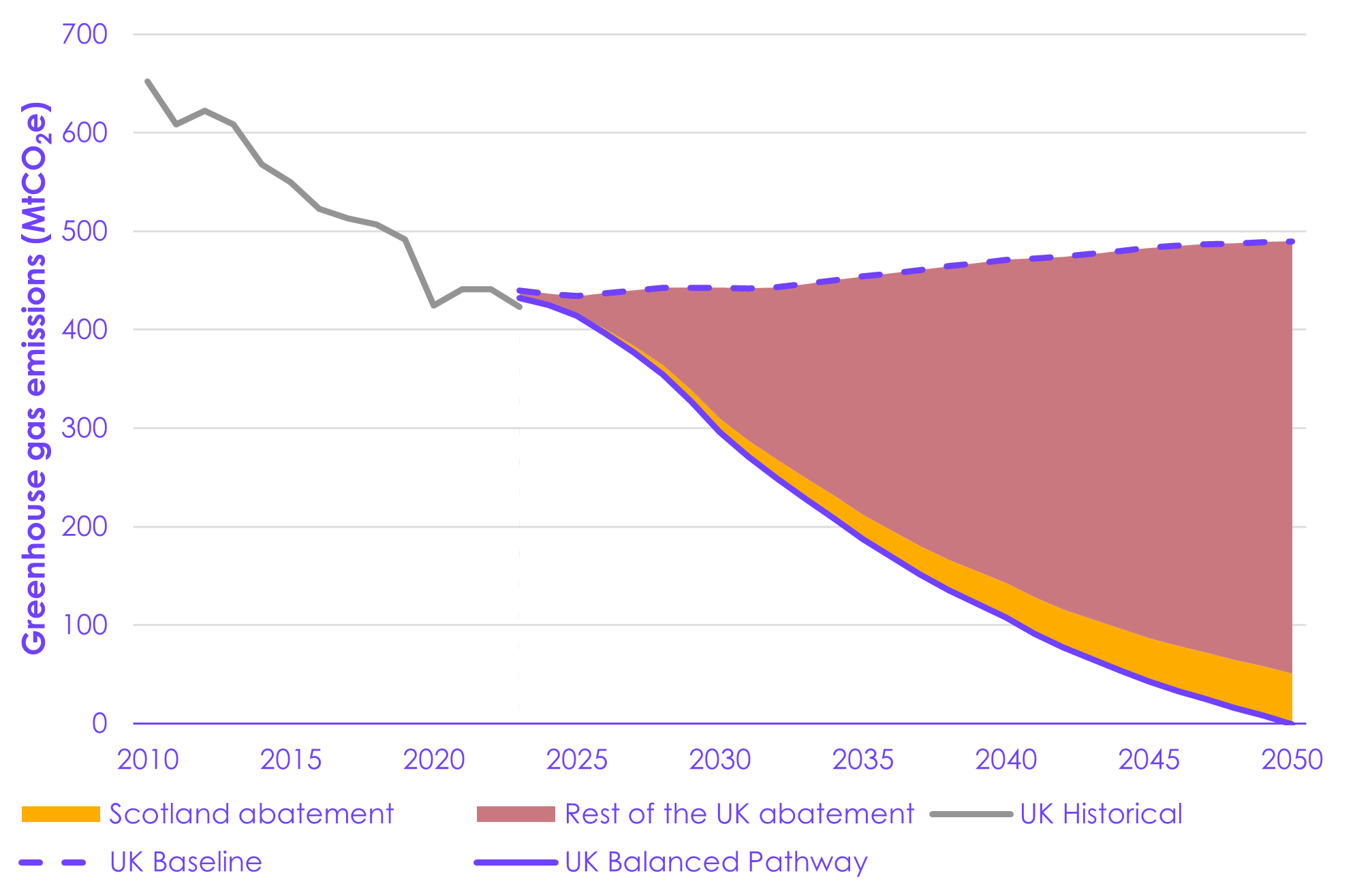

Emissions reductions in Scotland deliver around 10% of the overall abatement required between 2025 and 2050 to meet the recommended UK-wide Seventh Carbon Budget and Net Zero target, similar to Scotland’s share of total current UK emissions of around 9% (Figure 2.3).

|

Figure 2.3 Scotland’s contribution to the UK-wide Balanced Pathway |

|

|

2.2.5 Contribution towards the Paris Agreement temperature goal

The Act requires the Committee to advise on the estimated contribution of the carbon budgets towards global efforts to limit the global average temperature increase to 1.5°C above pre-industrial levels.

- The recommended carbon budgets are aligned to Scotland’s 2045 Net Zero target and the UK Balanced Pathway to achieve Net Zero by 2050 across the UK. In our UK-wide Seventh Carbon Budget advice, we set out how the UK Balanced Pathway relates to the Paris Agreement principles (see Section 10.1 of that report).

- We assess our recommended carbon budgets to represent a fair and ambitious contribution to global efforts to tackle climate change. They would be a credible contribution towards the ambition to limit long-term global warming to the 1.5ºC benchmark referenced in the Paris Agreement.

- They imply emissions reductions at least as fast as the global average under 1.5ºC scenarios on most baselines, on the basis of globally cost-effective 1.5ºC scenarios with ‘no or low overshoot’, with action beginning in 2020, as synthesised in the Intergovernmental Panel on Climate Change’s (IPCC) Sixth Assessment Report (AR6).[60]

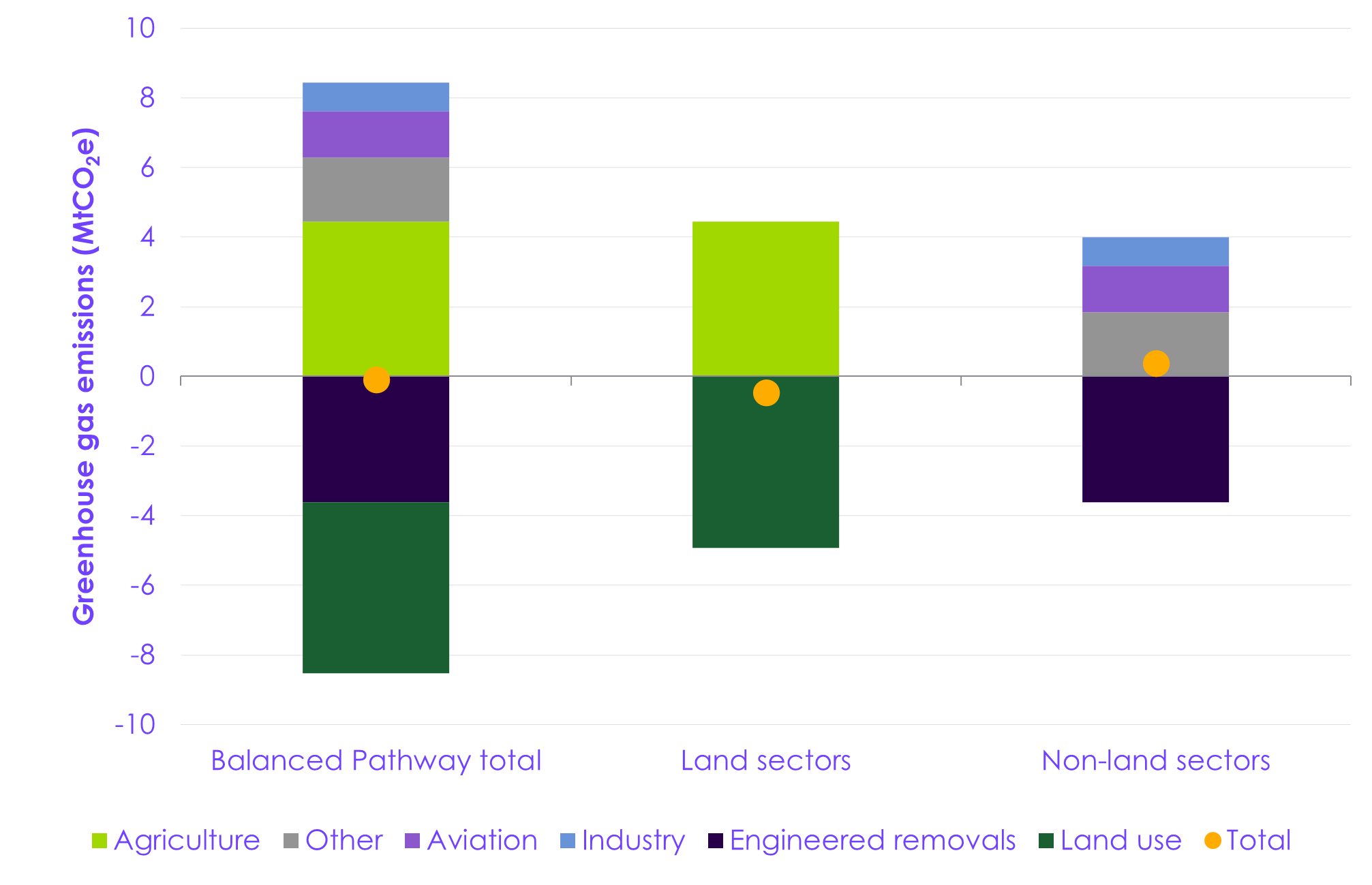

- The residual GHG emissions that remain in our pathway in 2045 are a mix of long-lived CO2 and nitrous oxide, and short-lived methane. These are all balanced by land-based and engineered removals of CO2. Overall, this leads to a peak and then decline in Scotland’s contribution to global warming by 2045, as continuing shorter-lived methane emissions are offset by removals of long-lived CO2 (see Section 2.4).

2.3 Drivers of emissions reductions in the Balanced Pathway

2.3.1 Emissions by greenhouse gas

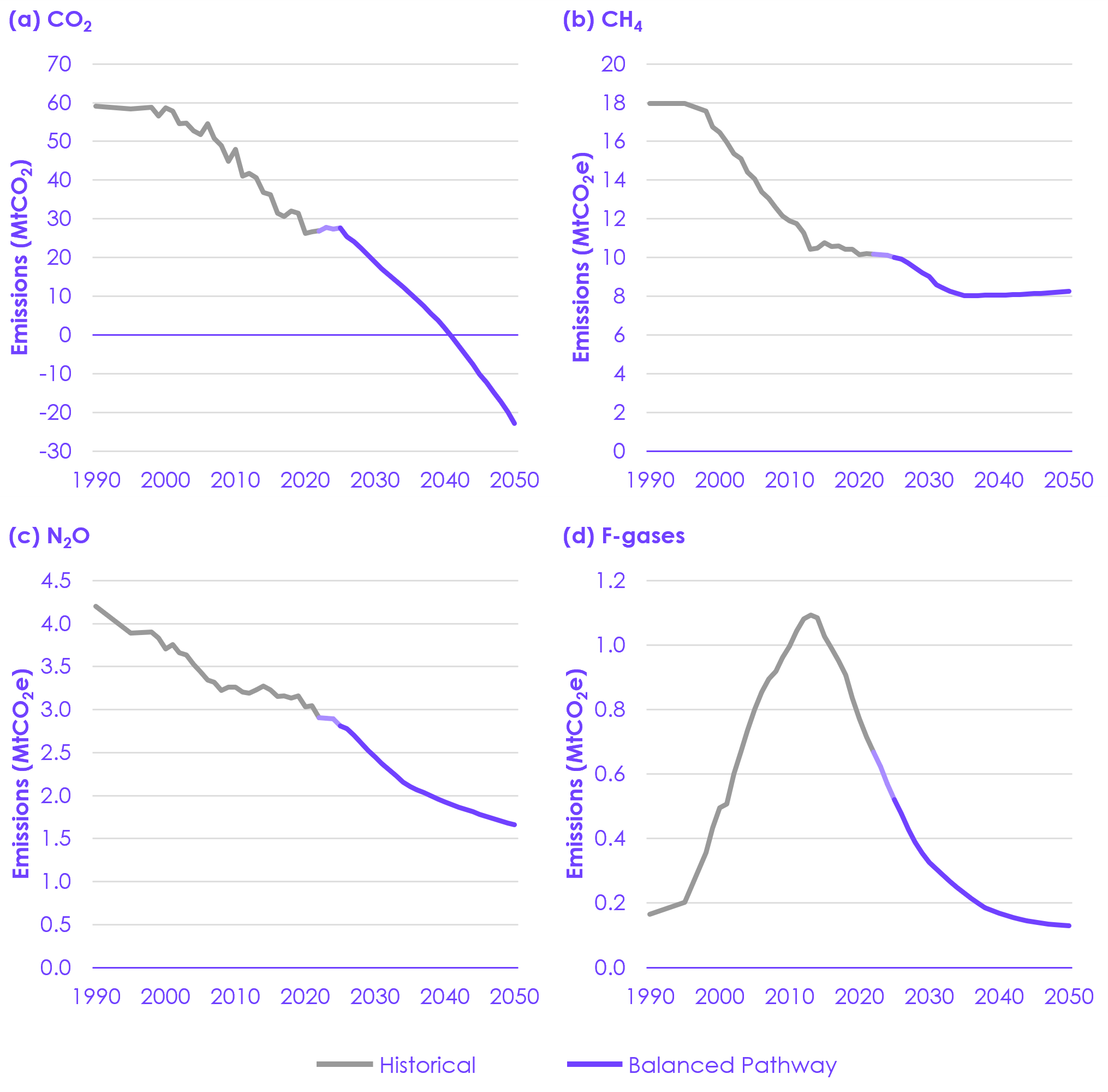

The Balanced Pathway reaches Net Zero across all GHGs in 2045 (Figure 2.4).

- Scotland reaches Net Zero CO2 four years earlier than the UK-wide Balanced Pathway, in 2041.

- This is largely due to proportionally higher rates of tree planting and faster deployment of DACCS in Scotland than in the other nations of the UK.

- CO2 reductions in our pathway come mostly from the roll-out of low-carbon technologies displacing fossil fuel combustion, along with reduced demand for high-carbon activities and deployment of engineered and land-based CO2 removals.

- Methane (CH4) emissions fall to 2035 but increase slightly between 2035 and 2050.

- Scotland saw large reductions in methane emissions during the 2000s, primarily due to reductions in waste and fuel supply emissions, although these have since plateaued.

- Methane emissions fall in the 2020s and early 2030s, mostly due to the impact of on-farm measures and diversification away from red meat and dairy production in agriculture, and reductions in methane generation at landfills.

- After 2035, methane emissions increase slightly. This is due to the significance of peatlands in Scotland. As peatlands are restored, rising water levels increase anaerobic decomposition, which in turn results in higher methane emissions. However, this is offset by CO2 savings as a growing proportion of peatlands are rewetted in the pathway.

- Nitrous oxide (N2O) emissions fall in the 2020s and early 2030s. Reductions come mainly in the agriculture sector, along with smaller reductions from reduced fossil fuel combustion across other sectors.

- Emissions of fluorinated gases (F-gases) continue recent trends of falling quickly. These are discussed in Section 3.2.11.

|

Figure 2.4 The Balanced Pathway by greenhouse gas in Scotland |

|

|

2.3.2 Sources of abatement

The first two carbon budgets cover the next decade. Therefore, meeting them will depend mostly on solutions that are available today, the vast majority of which come from electrification of key technologies across the economy and measures to reduce demand for high-carbon activities (Figure 2.5). Later in the pathway, nature and engineered removals play more of a role in balancing emissions in areas in which electrification is not feasible.

- Electricity: electrification delivers almost half of the total emissions reduction required throughout the Balanced Pathway. Electric technologies are now the clear low-carbon technology choice in many areas (including surface transport and home heating). They are available today and could be deployed rapidly in many key areas, provided the right incentives are put in place. Continuing to expand the supply of low-carbon electricity and the grid infrastructure to allow its use will be important to enable this to take place. Scaling up these immediate options is key to meeting all of Scotland’s carbon budgets.

- Demand: measures to reduce demand for high-carbon activities can be enacted from today and are particularly important to reduce emissions in the First Carbon Budget while technologies are still transitioning. They contribute around 30% of the total emissions reduction required by 2035. This includes measures to increase energy efficiency in homes, to use resources more efficiently in industry, and to reduce commercial, household, and food waste. There are also some sustained shifts away from high-carbon activities, including a shift to public transport and active travel and a reduction in livestock numbers driven by both reductions in meat consumption across the UK and measures to incentivise farmers to diversify income streams. Flying remains close to today’s levels until technology develops.

- Low-carbon farming, low-carbon fuels, and CCS: other low-carbon technologies play an important supporting role. This includes the deployment of hydrogen and CCS, which help to address sources of emissions that are less suited for electrification. In addition, a number of low-carbon farming practices and technologies are introduced in our pathway. Together these measures contribute around 10% of the total emissions reduction required in the Balanced Pathway.