Footnotes have been removed from the online version of this report. Please download the PDF for the footnoted version of this report.

Executive summary

Scotland has newly legislated emissions targets consistent with achieving Net Zero by 2045. The targets are achievable, provided the Scottish Government urgently utilises policy powers within its gift. Now it is time to deliver, with an opportunity to demonstrate commitment to this ambition.

Greenhouse gas emissions in Scotland fell 2.6% between 2021 and 2023. They are now less than half the levels seen in 1990. This good progress was mainly driven by a rapid scale-up of wind and solar electricity generation, supporting the GB-wide grid, while coal generation was phased out and gas generation declined. To achieve Scotland’s targets, action must now broaden to more sectors.

The Climate Change (Scotland) Act 2009 was amended in 2024 to repeal the previous interim targets. The Scottish Government and Parliament have since made rapid progress to legislate five-yearly carbon budgets, covering the period 2026 to 2045. These have been set at levels in line with the Committee’s advice and with achieving Net Zero by 2045. This is a positive step forward.

Following this, the Scottish Government published its draft Climate Change Plan (CCP), including a set of quantified policies and proposals for achieving the first three carbon budgets. While most of the required emissions savings to achieve the First Carbon Budget (2026 to 2030) have credible plans or plans with only some risks, there are significant risks to achieving much of the Second (2031 to 2035) and Third (2036 to 2040) Carbon Budgets. Time is tight, with long lead times between policy action and emissions reductions in many cases. More detail is needed on the expected roll-out of key technologies and measures to ensure effective monitoring is possible.

Most of the required emissions reductions will come from sectors with policy powers devolved to the Scottish Government. This includes a transition to modern, efficient, electrified technologies for transport and heat in buildings, as well as reducing emissions in agriculture and land use.

- Electric vehicles: with prices of new electric vehicles (EVs) falling, public charge points being rapidly rolled out, and strong policy in the UK’s zero-emission vehicle (ZEV) mandate, there is potential for sales to grow quickly. This should be supported by continued pace in the charge point roll-out and strong supportive messaging.

- Low-carbon heat: the draft CCP lacks sufficient plans for buildings. Very little emissions reduction is projected to occur over the next ten years, compensated for by a rapid acceleration in the late 2030s. It is not clear what will drive this acceleration, which will be challenging for supply chains to deliver. This ‘delay and catch-up’ approach therefore carries significant risk. A more plausible approach would be to implement policy to build on, and accelerate, the recent steady increase in heat pump installations seen in Scotland.

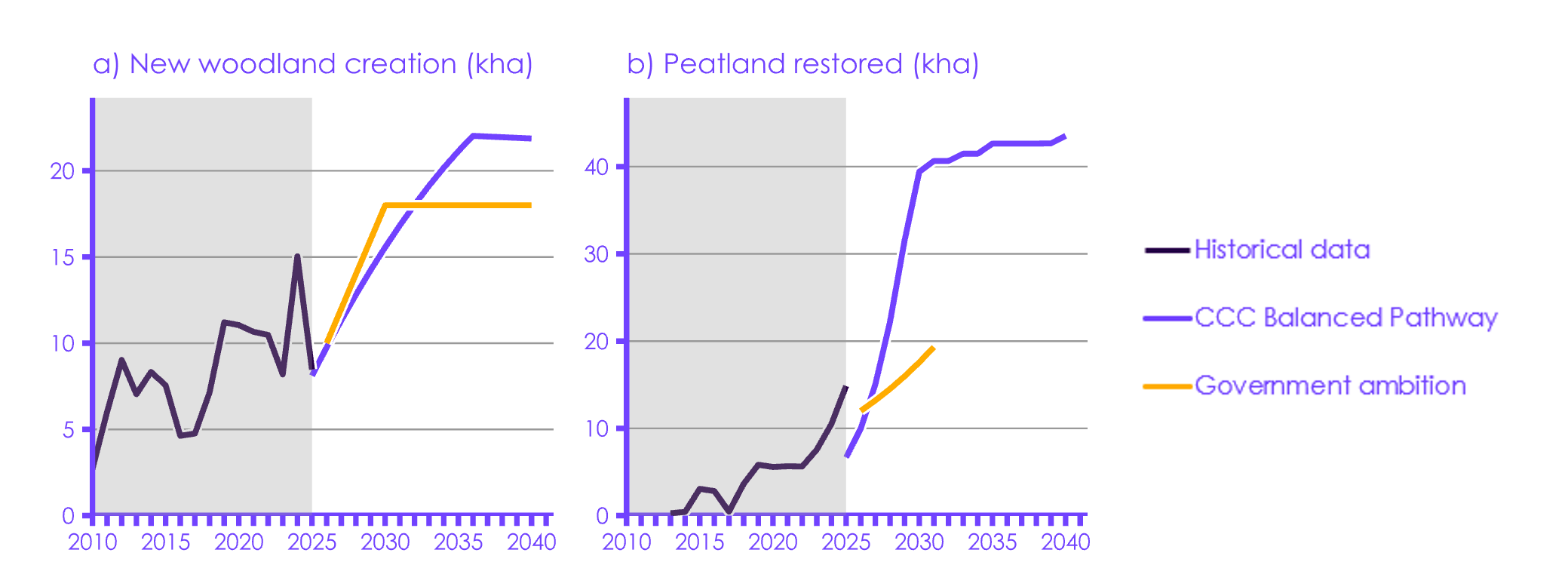

- Woodland and peatland: a significant and sustained increase in tree planting and peatland restoration is needed. While both have seen recent increases, tree planting rates have not been sustained, and low historical planting rates have led to a decline in the forestry sink. Stop-start funding leads to uncertainty and damages supply chains. A joined-up approach with agriculture will be needed to understand the scale and type of land required.

While the majority of the required emissions reduction is in sectors with policy powers in the Scottish Government’s hands, it is vital that the Scottish and UK Governments work together effectively to achieve their shared objectives. This is particularly important given the Scottish Government has chosen a pathway with a heavy reliance on negative emissions technologies (NETs), an area with significant risk and with policy powers largely reserved to the UK Government. A co-ordinated approach with plans for UK-wide NETs will be needed to ensure successful delivery, with the Scottish Government ensuring Scotland is an attractive location for NETs.

Climate change in Scotland

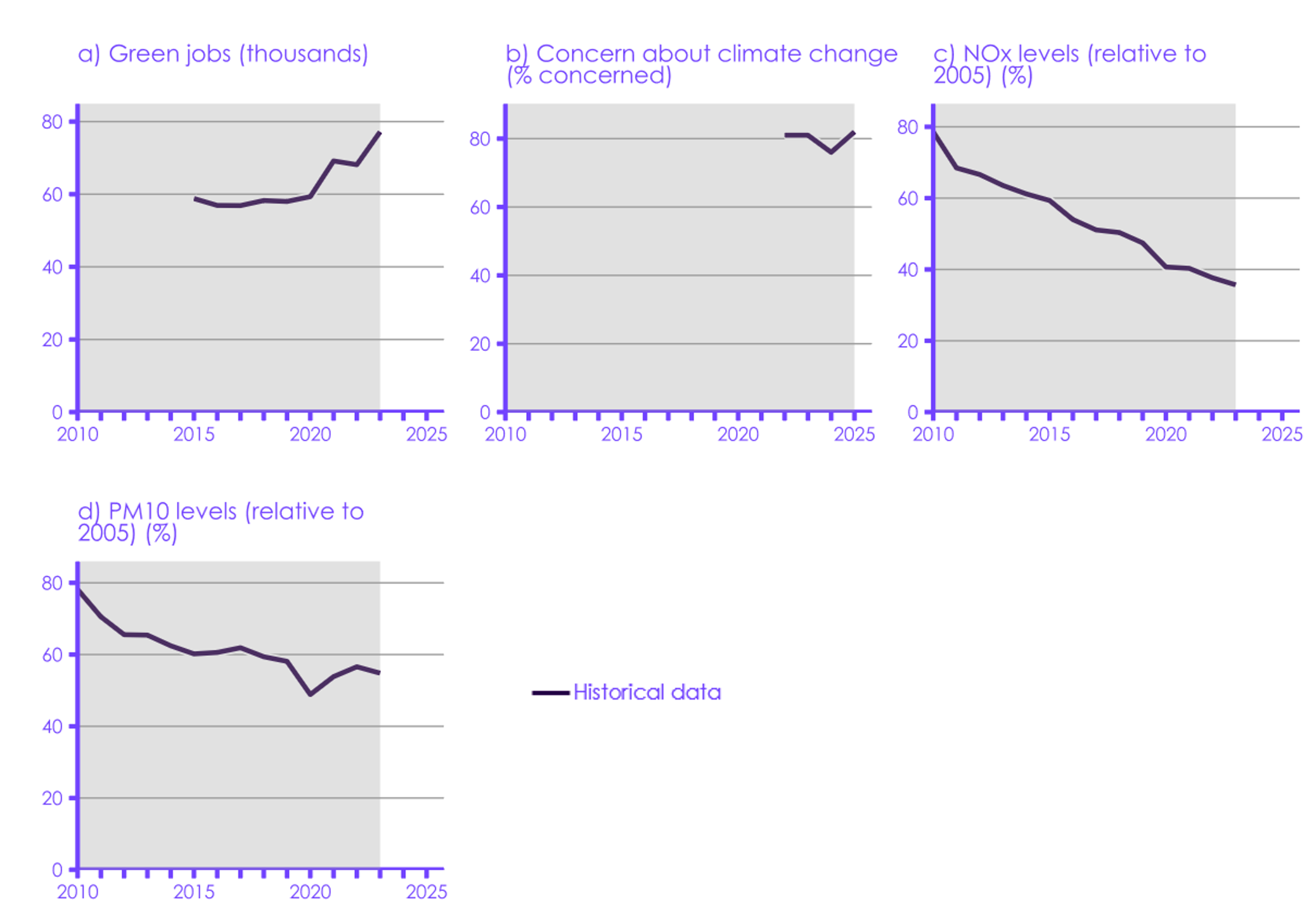

The people of Scotland are already feeling the effects of climate change today. According to the Summer 2025 Public Attitudes Tracker, 82% of Scottish respondents were very or fairly concerned about climate change. Winters are getting wetter, raising flood risk. Summers are getting warmer, with more intense and more frequent heatwaves impacting people’s health. Sea levels are rising around the coasts of Scotland and its islands. Scotland is also experiencing more instances of new climate impacts such as wildfires and drought in East Scotland, impacting rural parts of the country. Scotland must continue to reduce its greenhouse gas emissions while simultaneously becoming more resilient and preparing for the rapidly increasing severity of future risks. A failure to prepare for the effects of climate change in Scotland will increasingly create risks to the delivery of the pathway to Net Zero – this must be addressed alongside reducing greenhouse gas emissions.

Scotland’s carbon budgets and the draft Climate Change Plan

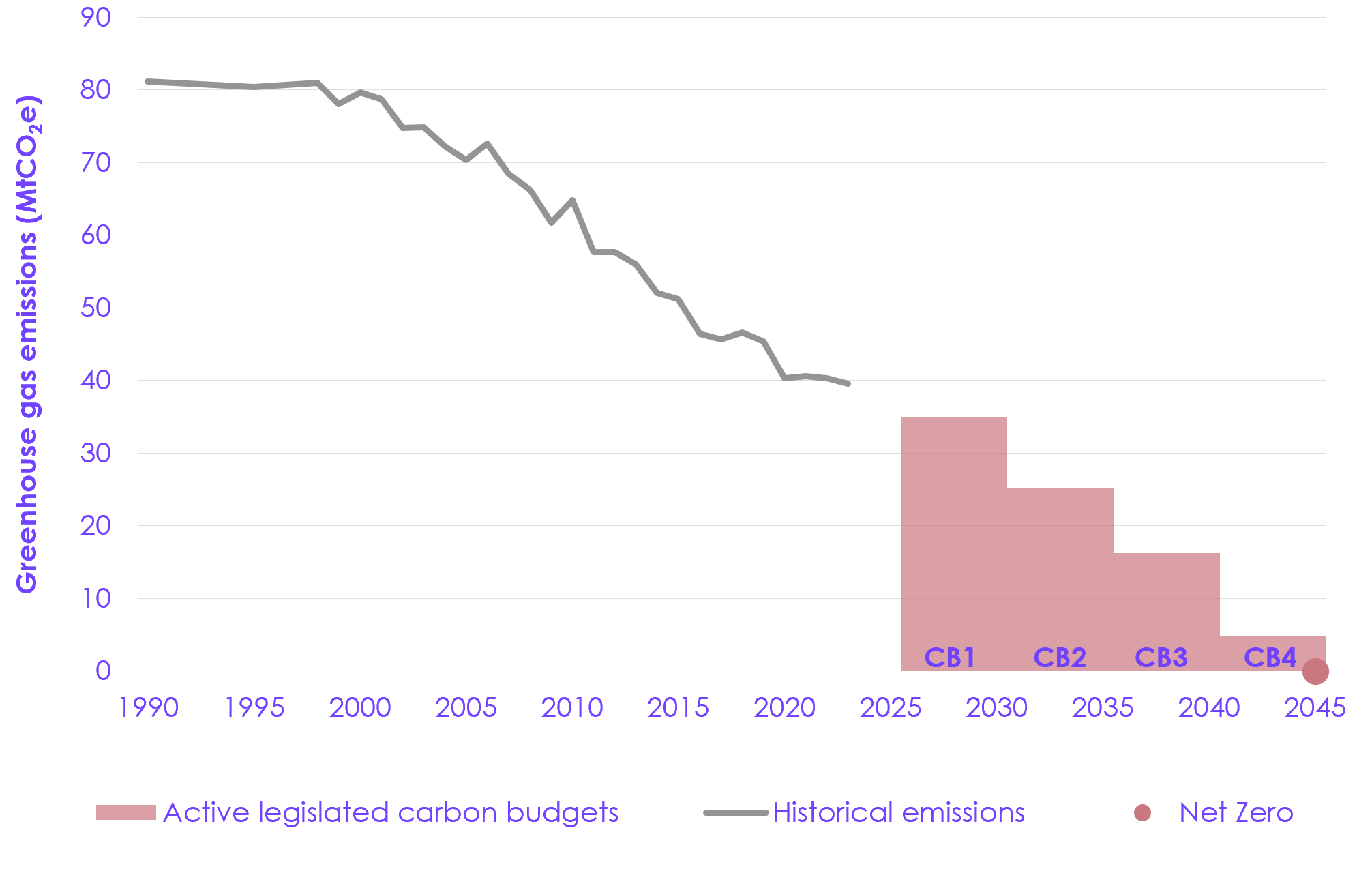

Under the Climate Change (Scotland) Act 2009 (the Act), Scotland has a target to reach Net Zero greenhouse gas emissions by 2045. In 2024, the Act was amended to replace the old interim decadal and annual targets with a framework of five-yearly carbon budgets (a carbon budget is a cap on greenhouse gases emitted in Scotland over a five-year period). Since then, the Scottish Government and Scottish Parliament have made rapid progress in legislating the levels of the four carbon budgets, covering the period 2026 to 2045. The carbon budgets are set such that the average annual level of emissions will be:

- 57% lower than 1990 levels for the First Carbon Budget (2026 to 2030), implying a 12% reduction from levels in 2023.

- 69% lower than 1990 levels for the Second Carbon Budget (2031 to 2035), implying a 36% reduction from levels in 2023.

- 80% lower than 1990 levels for the Third Carbon Budget (2036 to 2040), implying a 59% reduction from levels in 2023.

- 94% lower than 1990 levels for the Fourth Carbon Budget (2041 to 2045), implying an 88% reduction from levels in 2023.

These targets are in line with our advice and with reaching Net Zero by 2045. Achieving them will require rapid decarbonisation action and will represent a fair contribution for Scotland to UK-wide and global efforts to mitigate climate change.

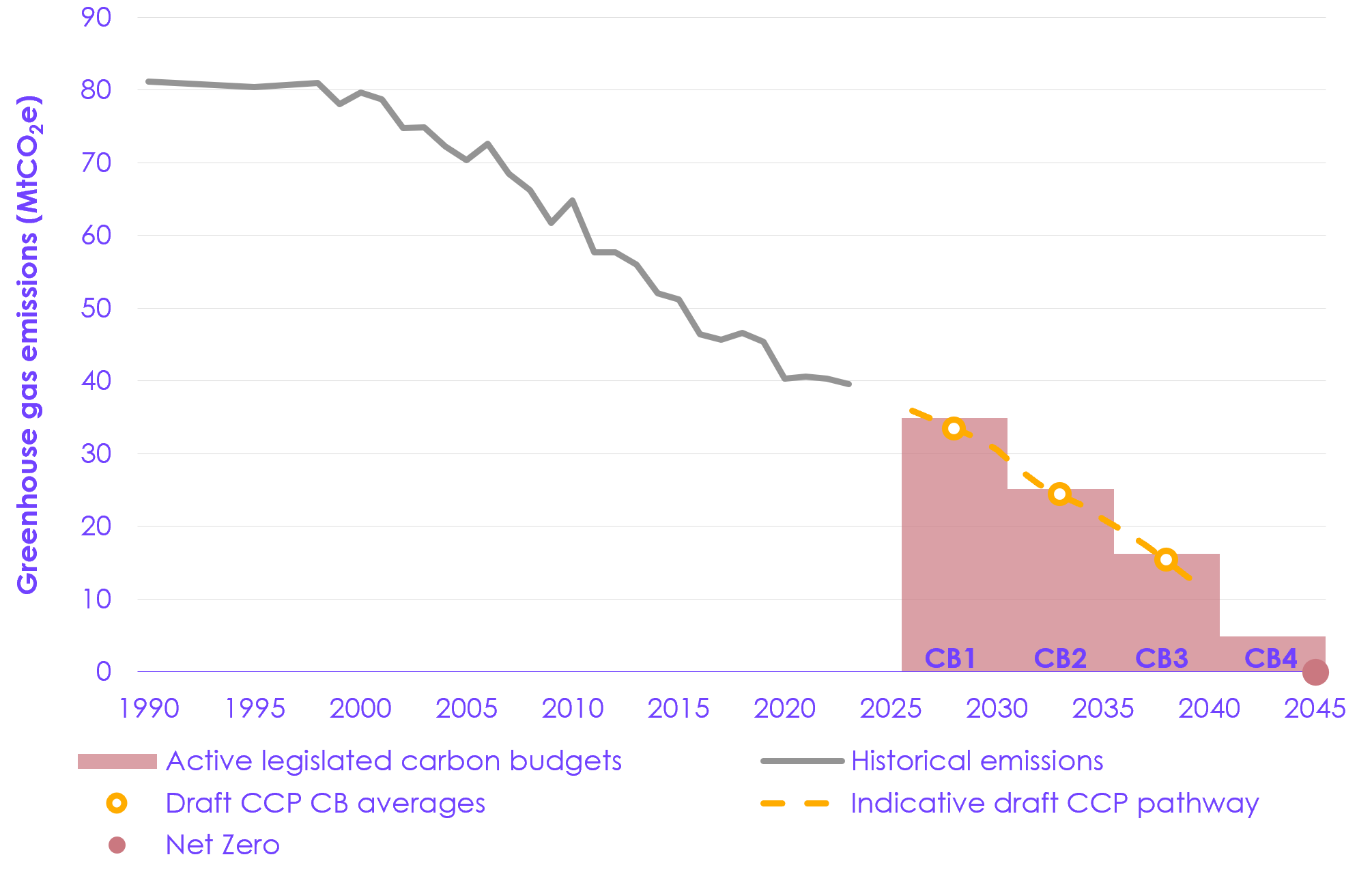

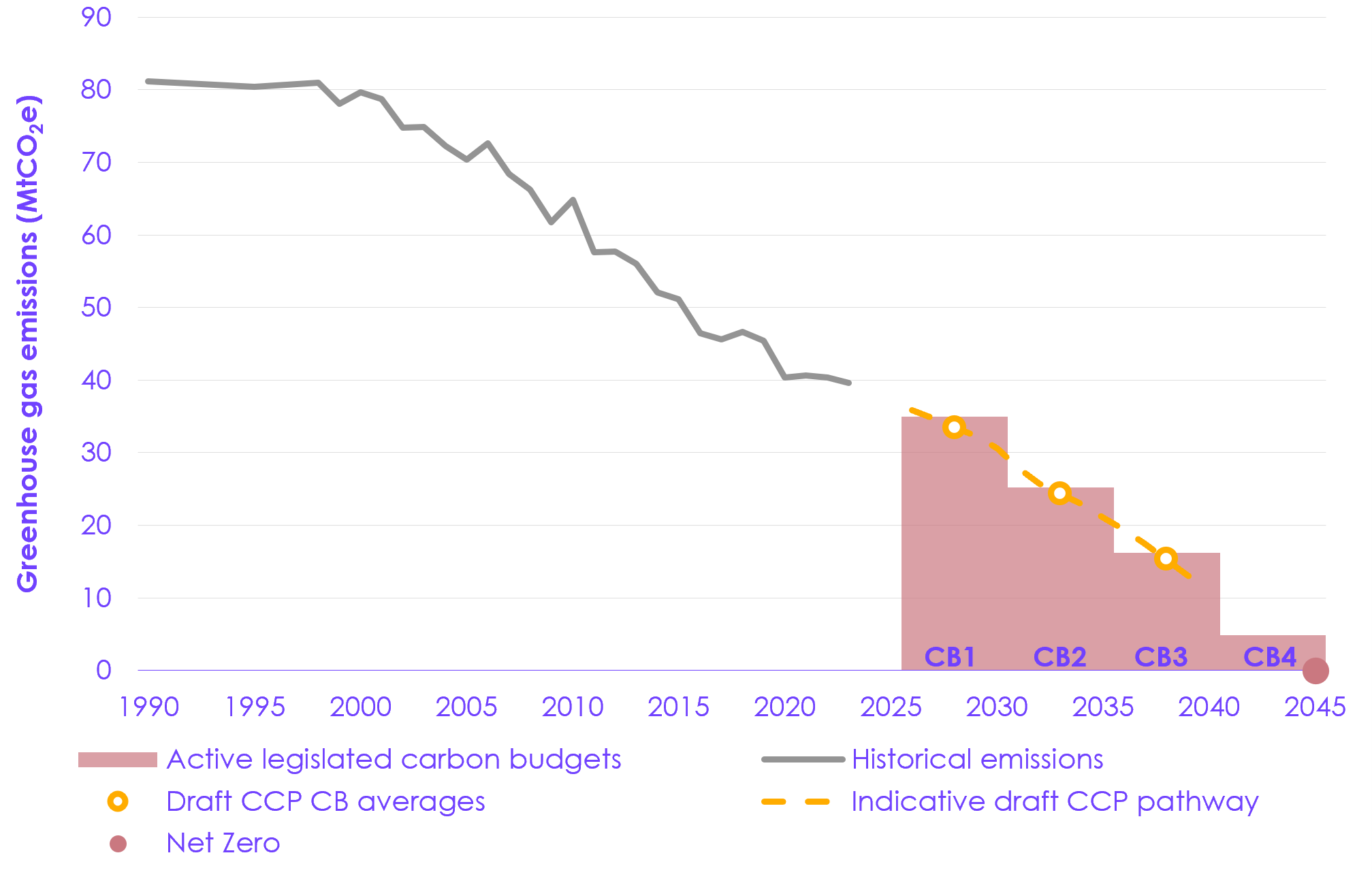

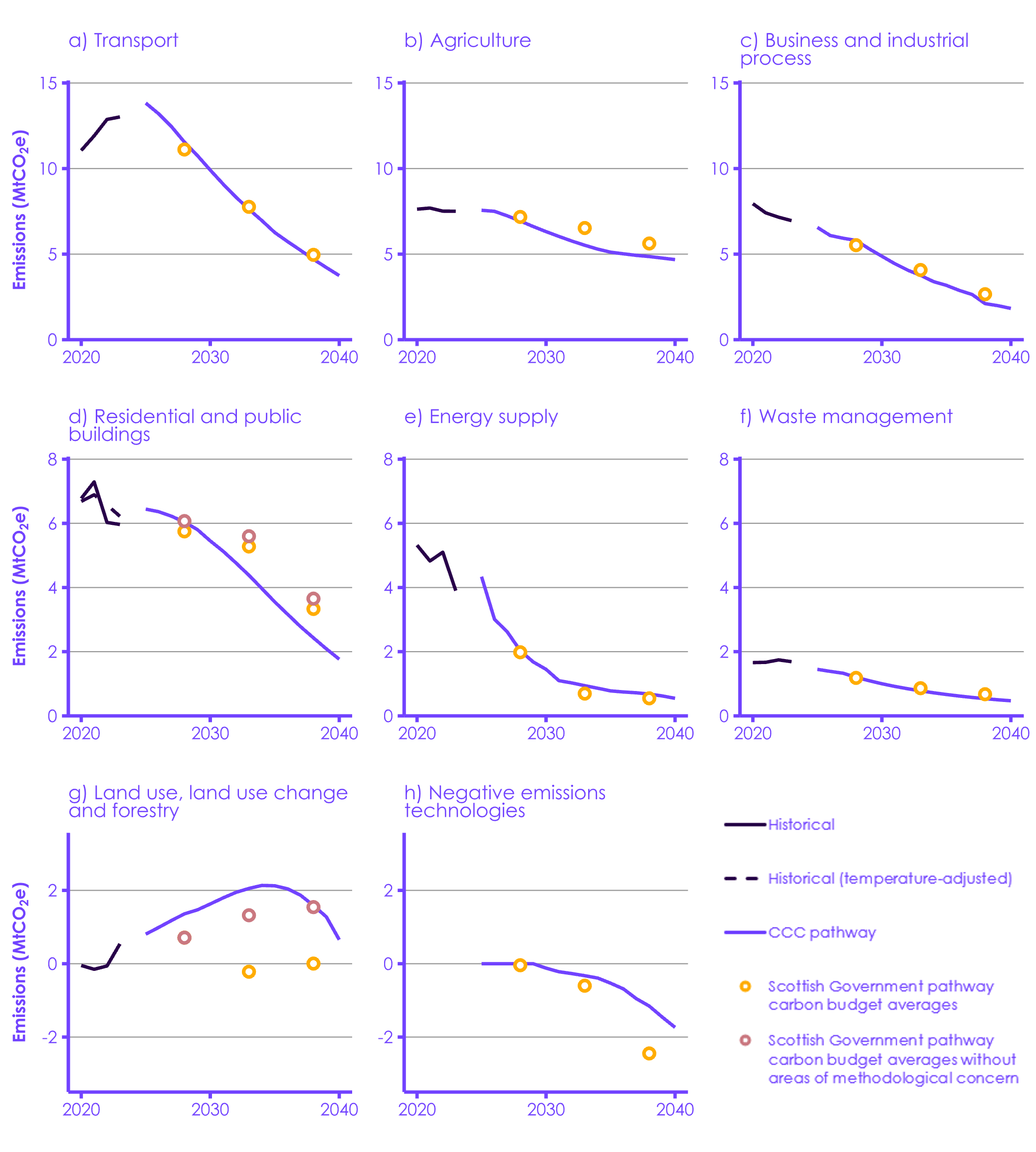

In November 2025, the Scottish Government published its draft CCP for the first three carbon budgets (2026 to 2040), setting out – for the first time – policies and plans with quantified emissions reductions attached to policy outcomes across all sectors of the economy and providing an emissions pathway that achieves the carbon budgets (Figure 1). We welcome this new draft plan, and it is positive to see it contain plans for a monitoring and evaluation framework, which includes just transition indicators for the first time. However, the draft CCP does not include deployment pathways for each key indicator. Nor does it include annual sectoral emissions pathways, with only carbon budget averages given. Due to the lag in reported emissions data, this makes it very difficult to monitor progress until a given carbon budget is almost over, when it will likely be too late to make adjustments to the pathway. The framework in the final CCP should include indicative annual sectoral emissions and indicator pathways, so that progress can be effectively monitored.

| Figure 1 Greenhouse gas emissions in Scotland and the Scottish Government’s targets and pathway |

Description: Scotland is more than halfway to Net Zero emissions. Scotland’s carbon budgets and draft Climate Change Plan (CCP) pathway are in line with Net Zero by 2045. |

Historical emissions in Scotland

Greenhouse gas emissions in Scotland were 39.6 MtCO2e in 2023, 51.3% lower than 1990 levels. This is significant progress, with emissions steadily falling since the start of the century (Figure 1).

- The primary driver of emissions reductions so far has been electricity supply. A significant ramp-up of wind and solar generation has enabled the phase-out of coal generation in 2016 and a steady decline in gas generation, which in 2023 contributed only 7% of the electricity generated in Scotland. The remaining 93% was low-carbon generation, primarily from wind power.

- There have also been substantial reductions in the business and industrial process; land use, land use change and forestry (land use); and waste management sectors.

Between 2021 and 2023, emissions fell by 2.6%, falling year-on-year in both 2022 and 2023, following a slight increase in 2021.

- Emissions reductions over these two years were largely driven by the residential and public buildings (buildings) and energy supply sectors.

- For buildings, around half of the overall reduction was due to milder-than-average winter months in 2022 and 2023 contrasting the colder winter months in 2021, and a likely behavioural response to record-high gas prices, rather than sustained changes in how buildings in Scotland are heated.

- Emissions from buildings vary considerably year-to-year due to annual variations in temperature and are likely to increase in colder winters. Additionally, it is highly uncertain whether behavioural responses will be maintained following reductions in gas prices.

- These reductions in emissions were partially offset by an increase in emissions in transport, as flying levels increased following the pandemic. There was also an increase in land use emissions, in part due to a legacy of lower tree planting rates over the previous two decades. This has led to a declining forestry carbon sink in Scotland. The land use sector has consequently recently transitioned from a net sink to a net source of emissions.

Emissions from imports from outside the UK, which are not included in the climate targets in the Act, have been relatively steady since 2009, following a drop after the financial crisis. This has happened despite territorial emissions falling considerably during this period, showing that this decrease is not being offset by increased emissions elsewhere.

Assessment of delivery and policy progress

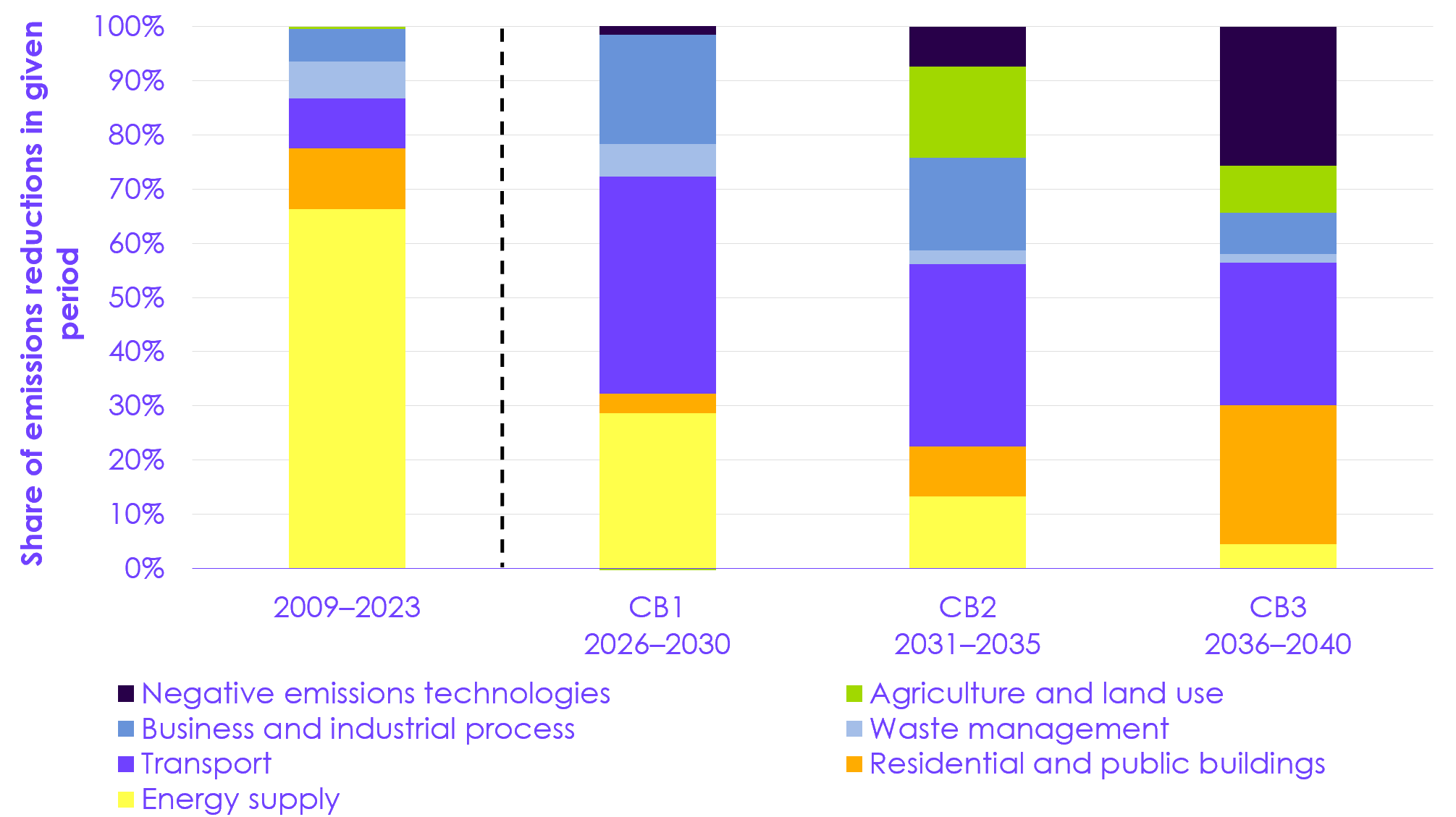

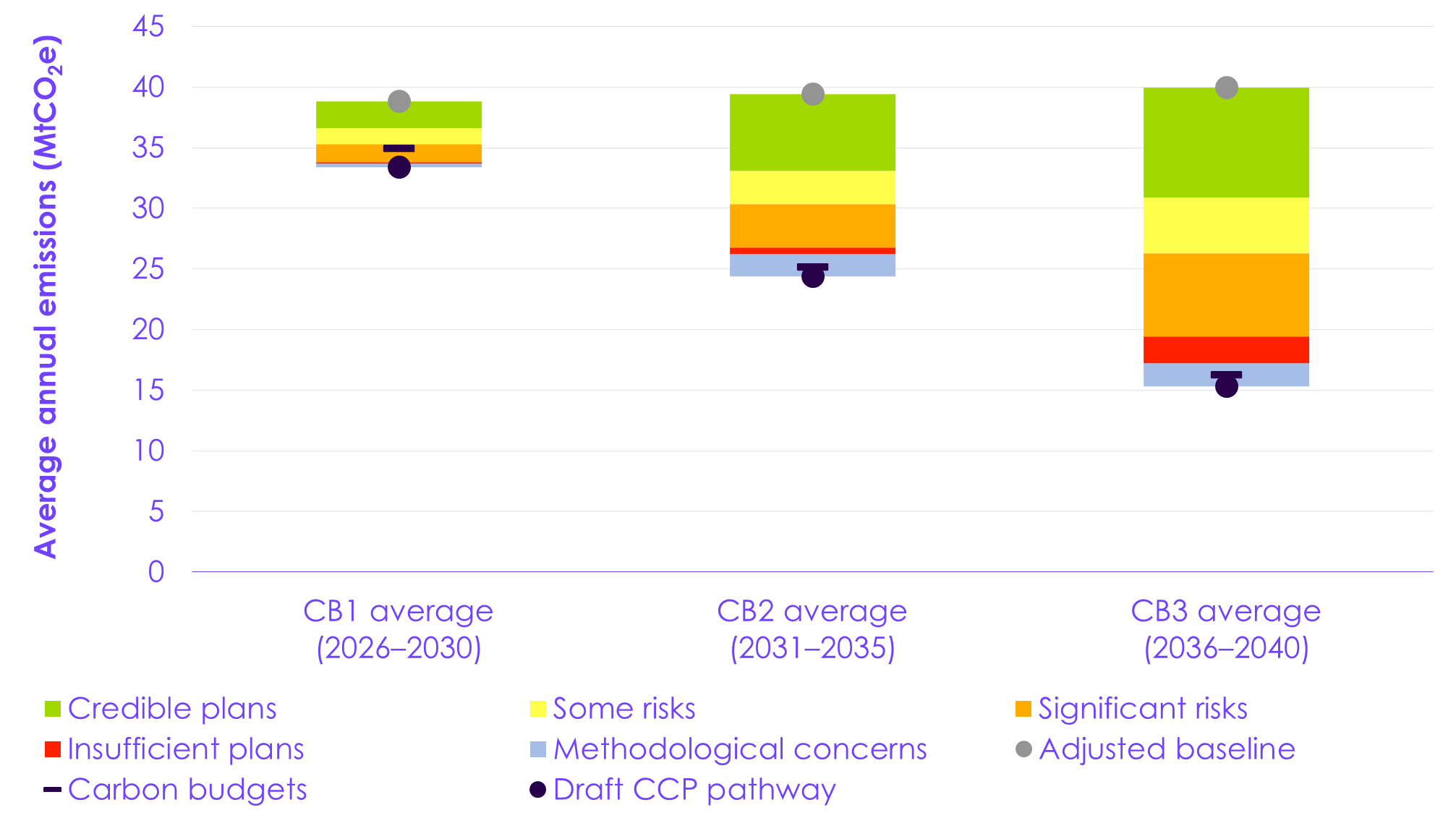

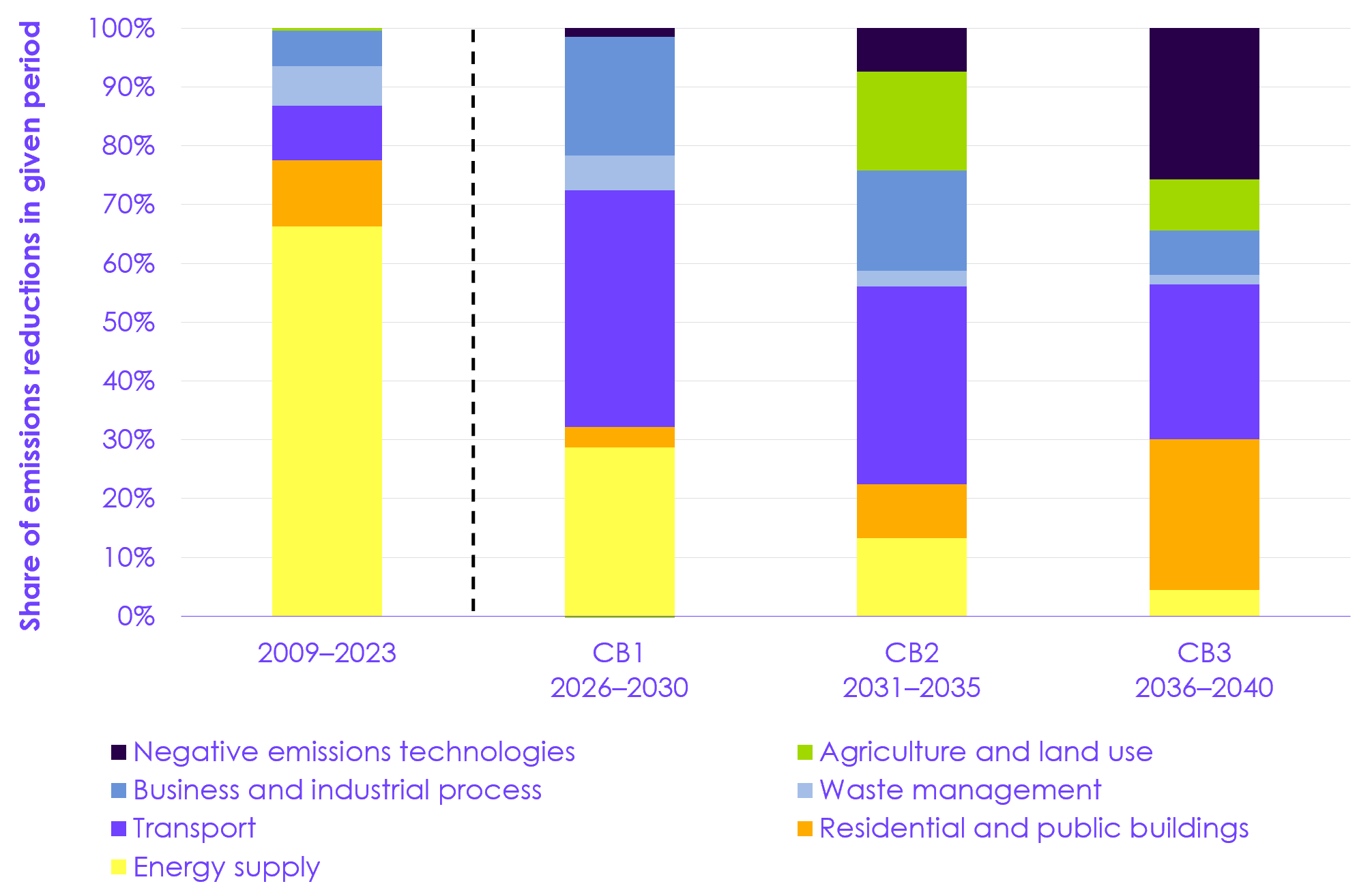

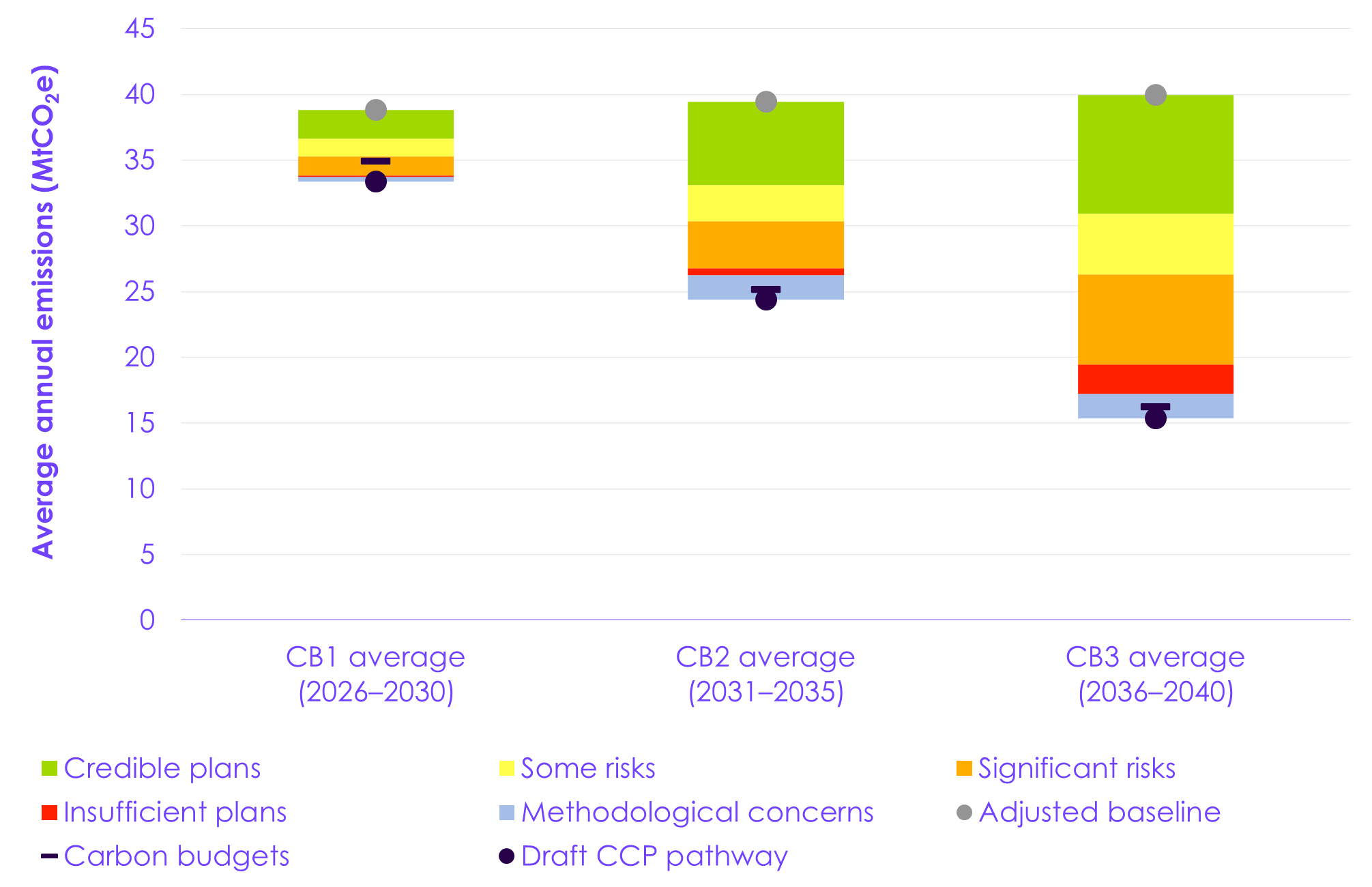

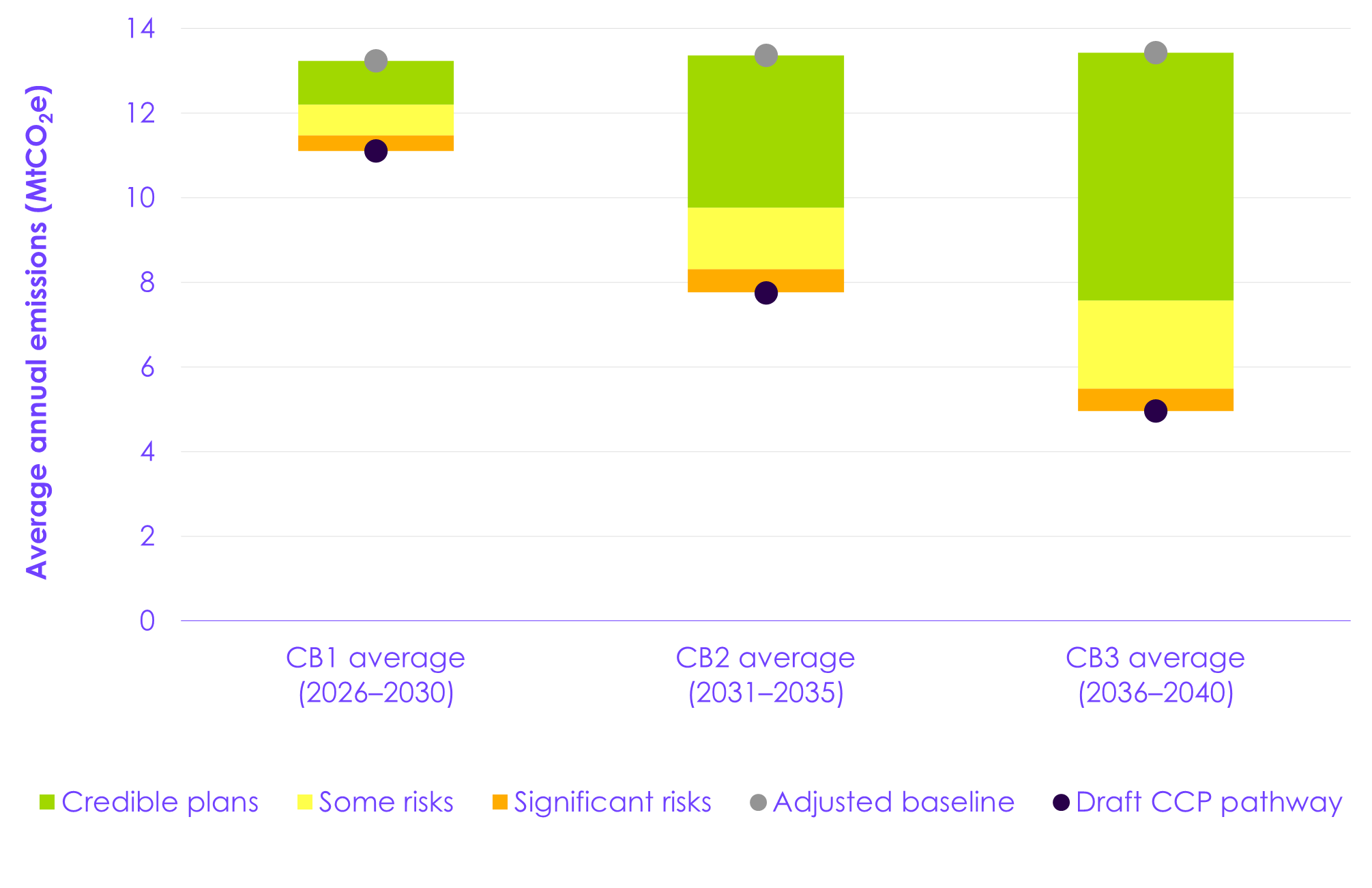

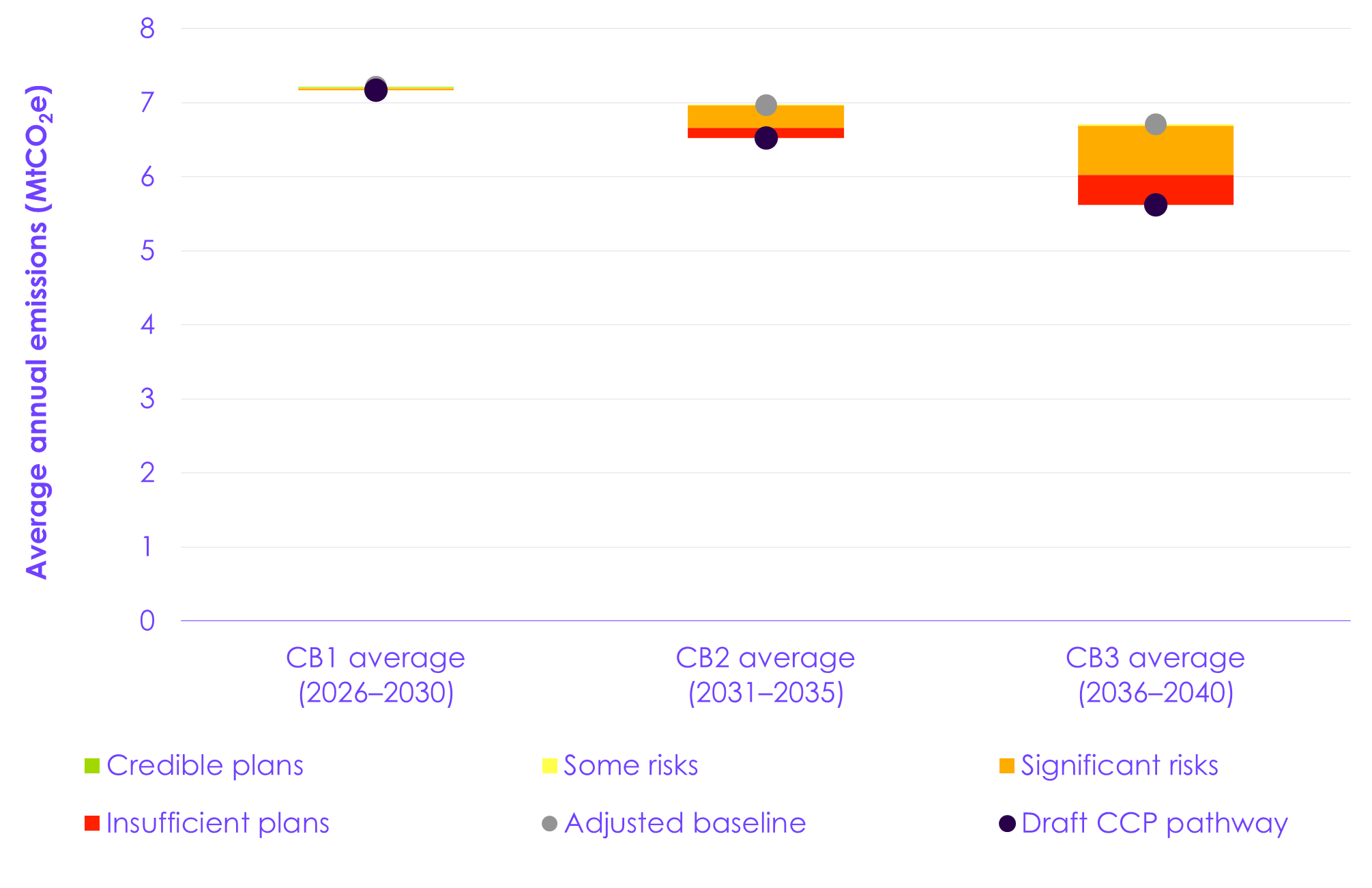

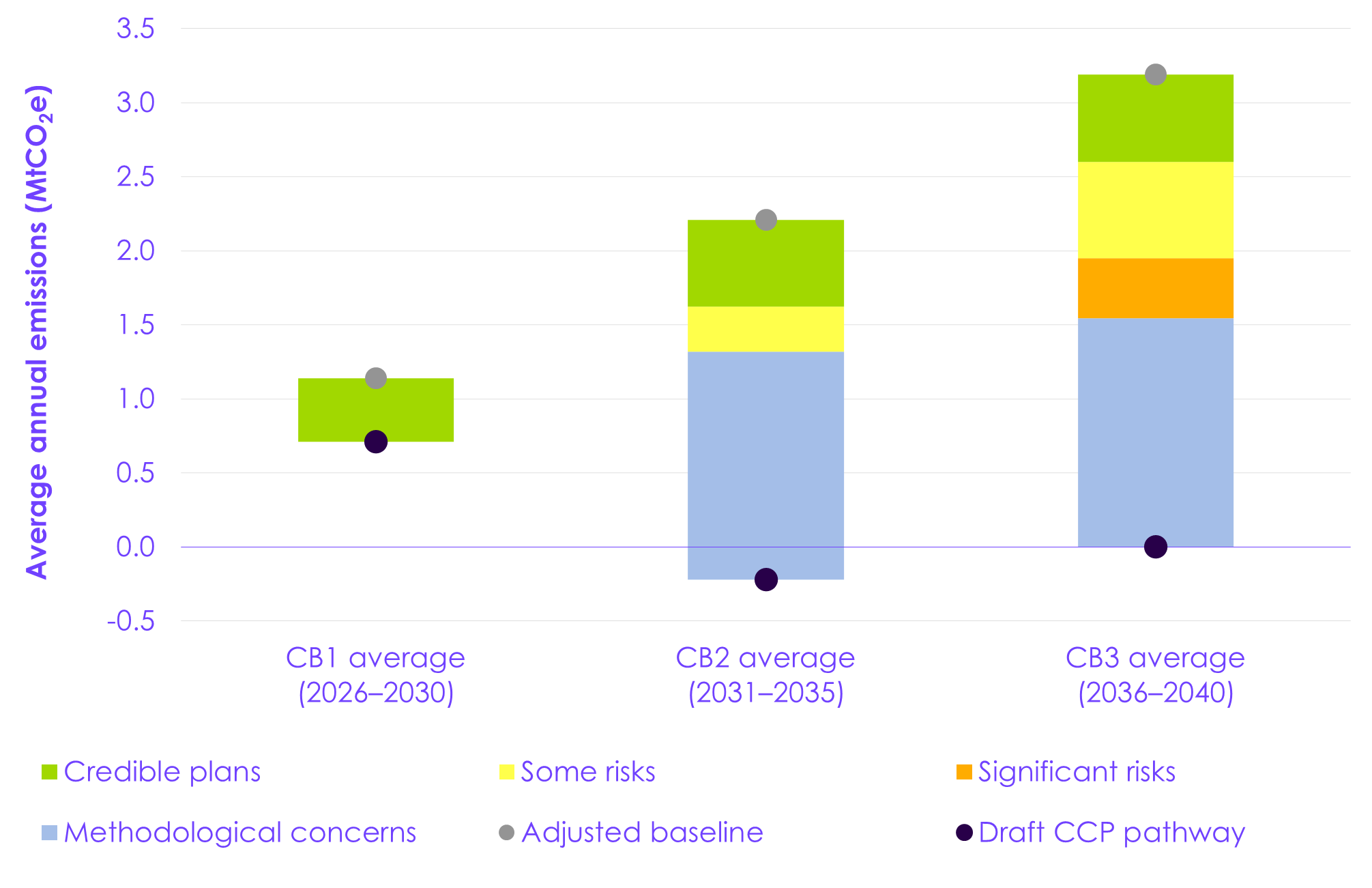

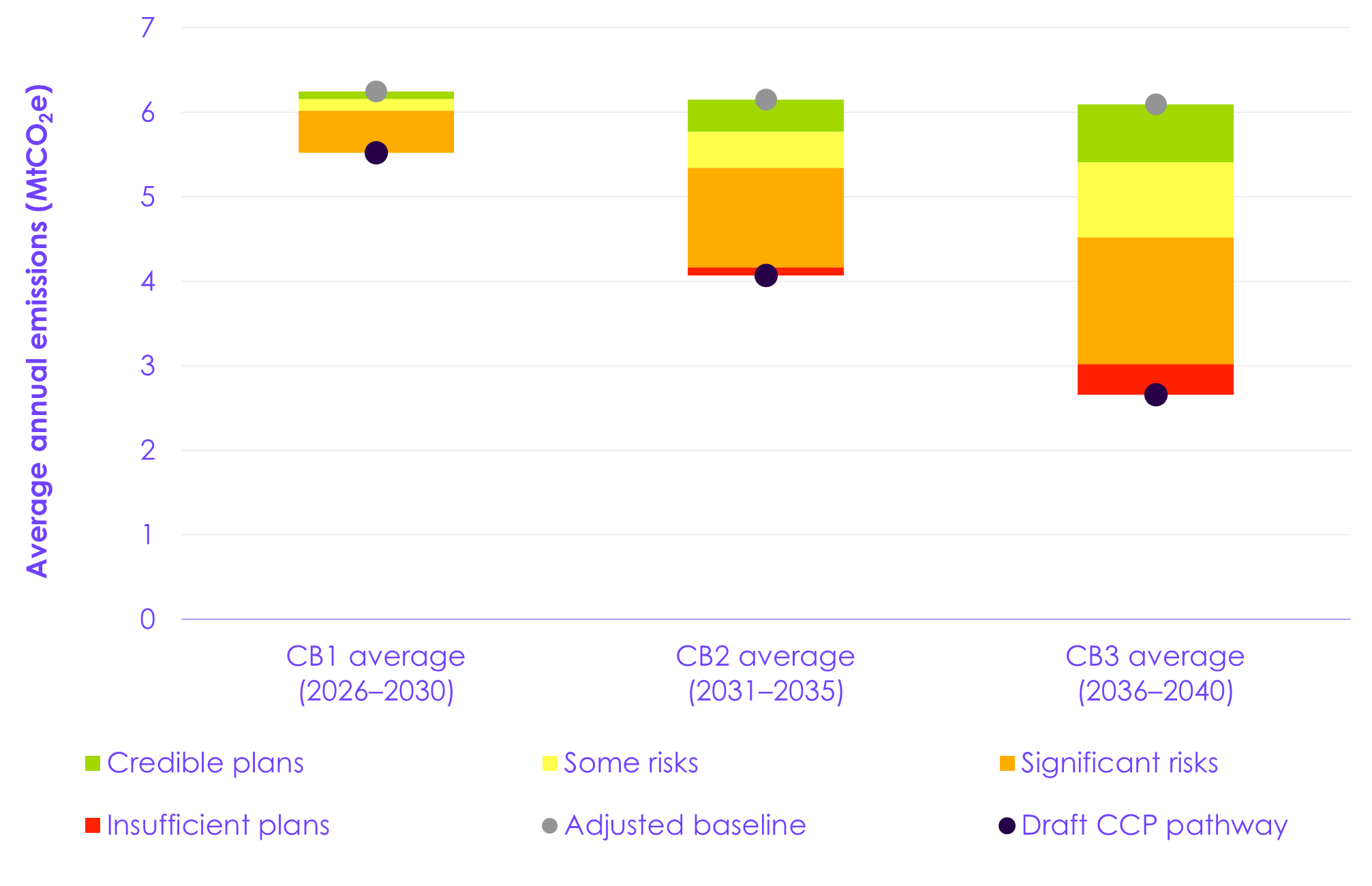

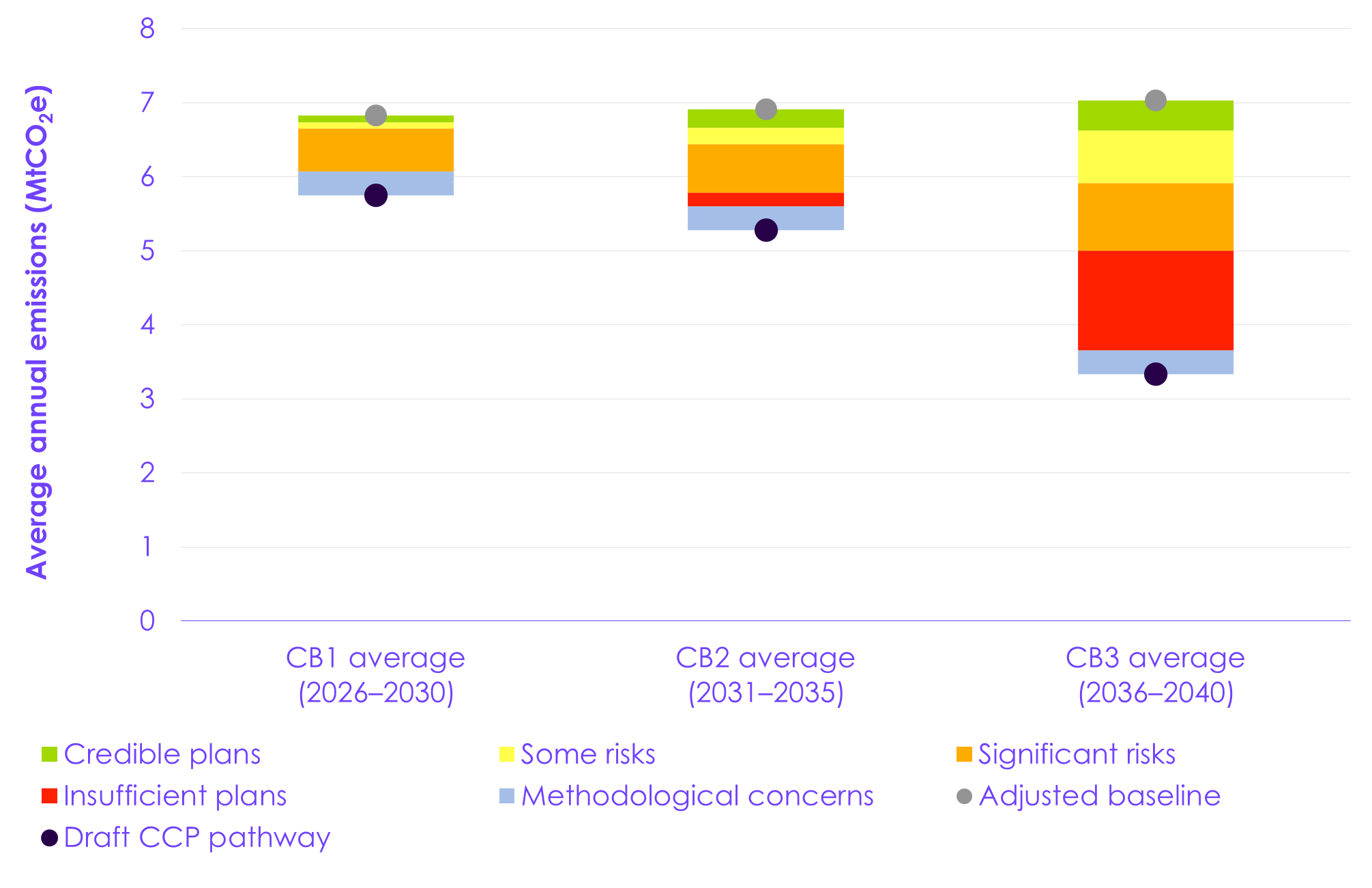

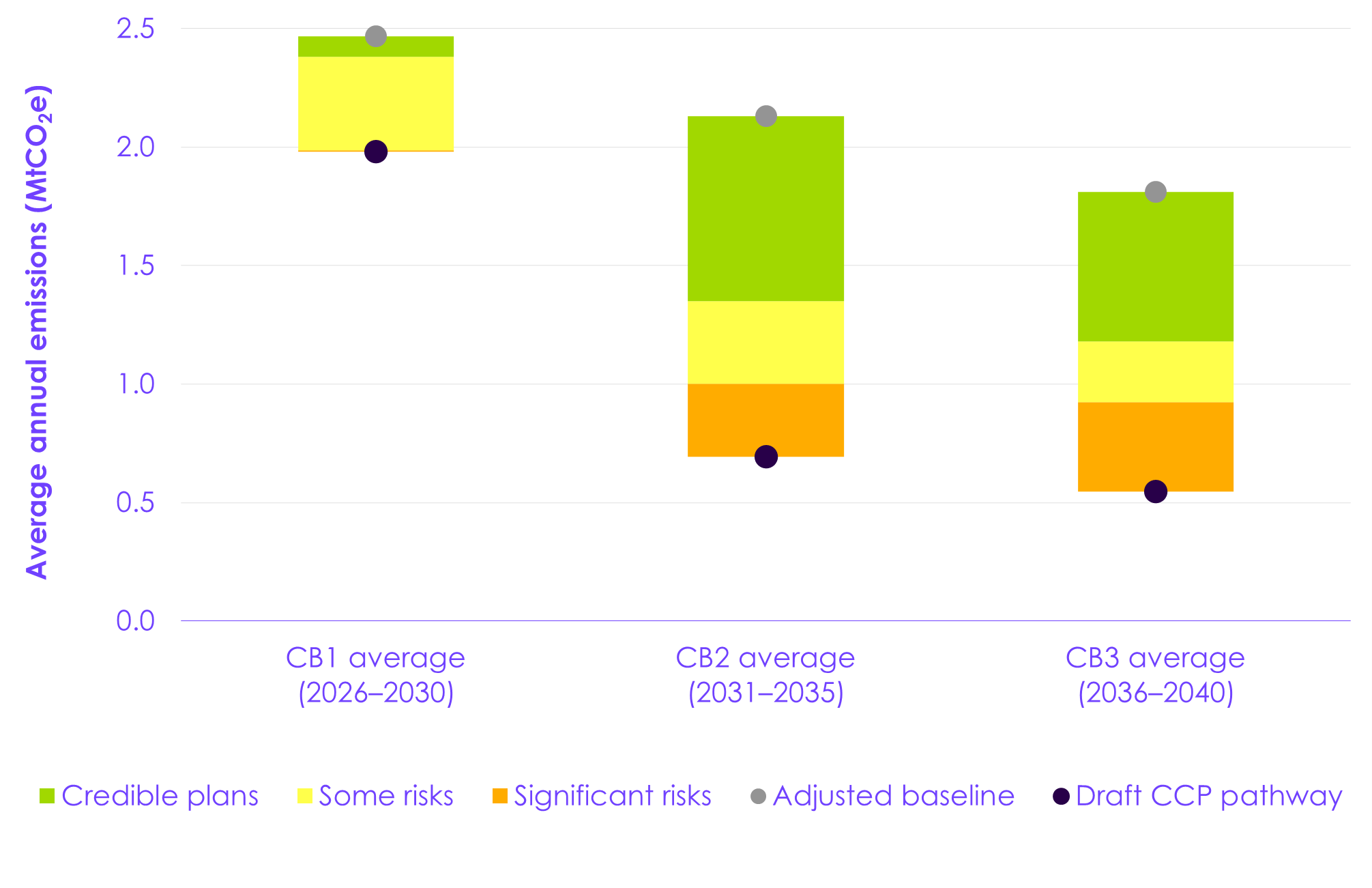

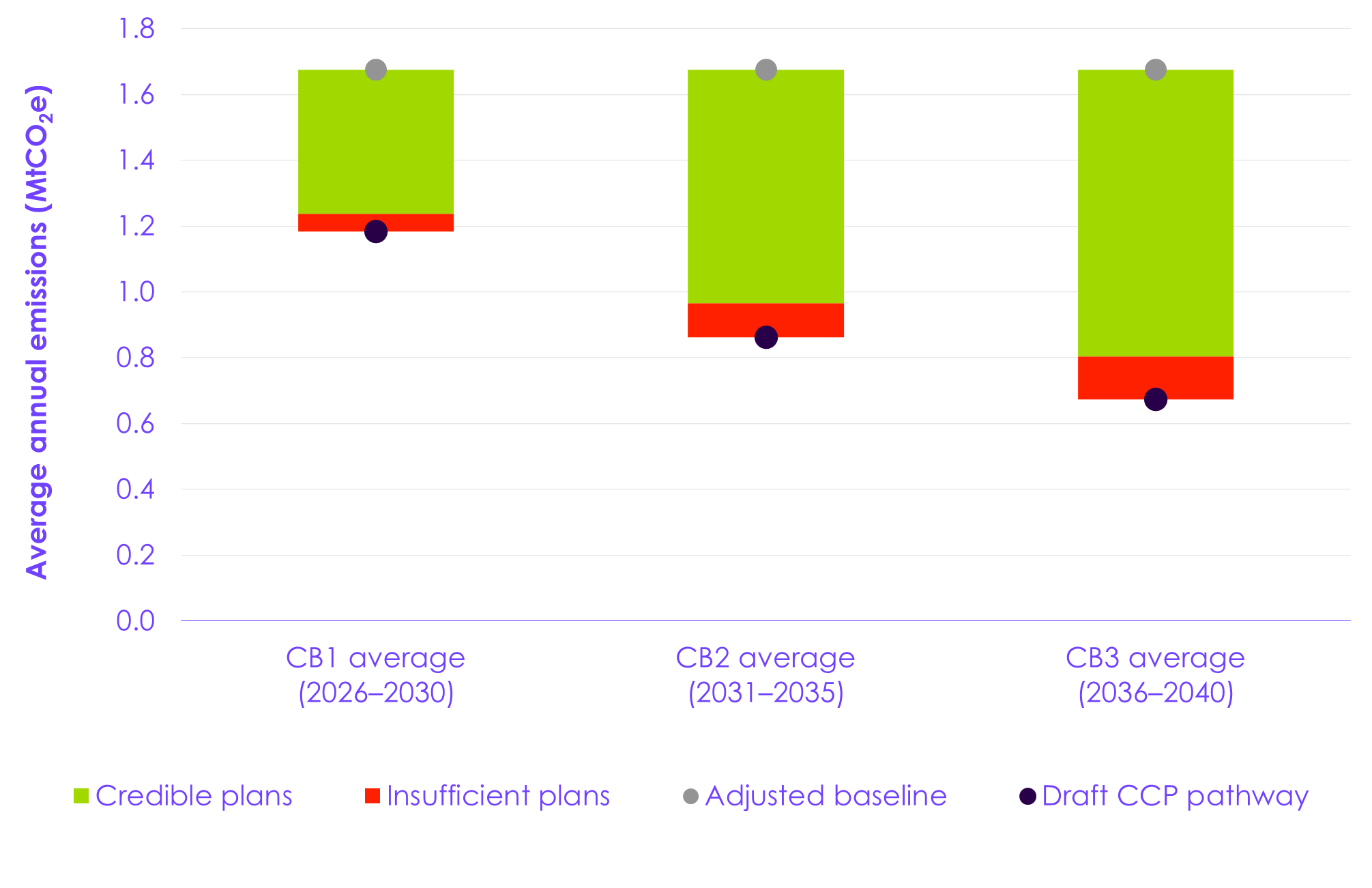

The draft CCP shows that emissions reductions will need to broaden to more sectors, with significant contributions from sectors with policy powers in the Scottish Government’s hands (Figure 2). We have assessed the policies and plans in the draft CCP, determining if they are credible for delivering the required emissions savings in each carbon budget period, whether they carry some or significant risk, or whether plans are currently insufficient (see Annex 3 for our assessment criteria).

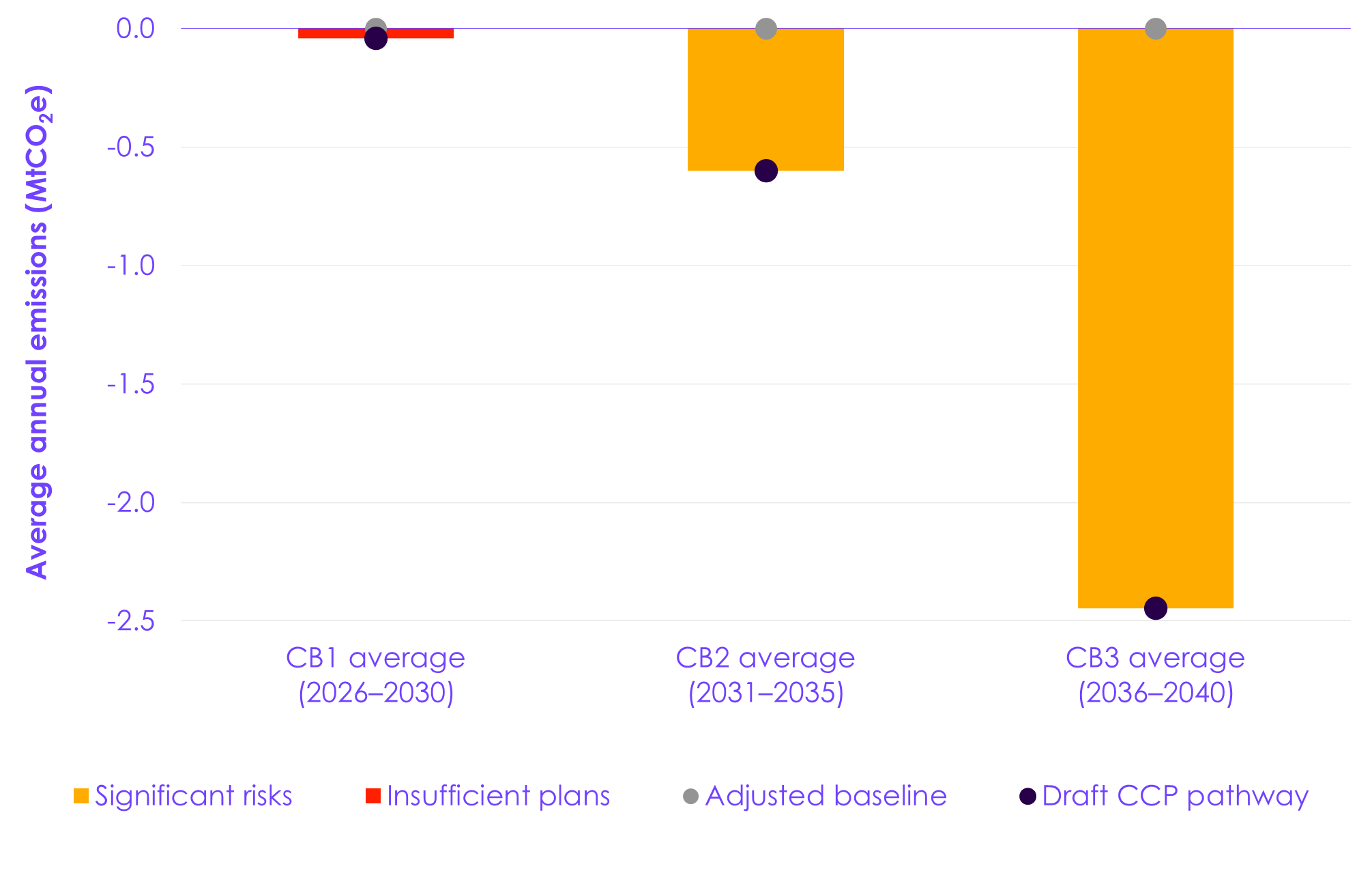

We assess that there are credible plans and plans with only some risks in place for the majority of the emissions reduction needed to achieve Scotland’s First Carbon Budget, with the draft CCP pathway going beyond the level of the budget. This is a prudent approach, allowing for some contingency. However, there are significant risks and gaps in policy for the Second and Third Carbon Budgets (Figure 3). And while the pathway goes slightly beyond the level of these two carbon budgets, the scale of this overperformance is less than the quantified impact of areas in which we have concerns about the assumptions and modelling methodologies employed:

- First Carbon Budget (2026 to 2030): 91% of the emissions reduction required to meet the First Carbon Budget is covered by credible plans or plans which carry only some risk.

- The majority of the required emissions reduction over this period comes from the transport, energy supply, and business and industrial process sectors (Figure 2).

- There are credible plans or only some risks for nearly all the emissions reductions in transport due to strong policy in the ZEV mandate and recent good progress in the roll-out of EVs and charging infrastructure. There are also credible plans for near-term peatland restoration, which has increased significantly in recent years.

- There remain significant risks for 9% of the required emissions savings, mostly related to the assumption that recent energy-saving practices in buildings following high gas prices will be maintained. While some (for example, reducing boiler flow temperatures) could be maintained following reductions in gas prices, others (such as underheating of homes due to affordability concerns) would not be desirable to continue.

- Second and Third Carbon Budgets (2031 to 2040): The proportion of required emissions reductions covered by credible plans, or carrying only some risk, reduces over time to 64% for the Second Carbon Budget and 58% for the Third Carbon Budget. The Scottish Government is therefore relying on areas with significant risks or insufficient plans in place, and highly uncertain wider factors that are not supported by policy levers, to deliver 36% of the required emissions savings for the Second Carbon Budget and 42% for the Third Carbon Budget.

- Emissions reductions need to broaden even further over this period, with buildings, agriculture and land use, and NETs becoming increasingly important (Figure 2). However, many aspects of the emissions reductions required in these sectors carry significant risk or in some cases have insufficient plans.

- The areas with credible plans in place are largely the same as those assessed as credible for the First Carbon Budget.

- Significant risks or insufficient plans are mostly related to decarbonising buildings, a large portion of industrial emissions, and NETs, with important contributions from agriculture.

- There are also some areas where we are concerned that the modelling methodologies employed leave aspects of the draft CCP pathway reliant on emissions savings that depend on highly uncertain wider factors:

- More than half of the expected emissions savings in land use are due to a peatland area inventory change that is assumed to be applied from the start of the Second Carbon Budget. This is based on emerging research indicating that the area of grasslands on peat soils and associated emissions could be substantially lower than currently estimated. It is unclear whether this correction will be incorporated into future emissions accounting and its impact is currently uncertain. Furthermore, the correction may affect the 1990 baseline emissions with respect to which the carbon budgets are defined, which has not been factored into the draft CCP projections.

- Energy demand in buildings is assumed to stay at the low levels seen in 2023 – when winter months were milder than average. While it is reasonable to account for the underlying trend of increasing temperatures lowering heating demand, there are year-to-year fluctuations either side of this trend. It is unlikely that temperatures would remain milder than the average underlying trend, and hence that heating demand would remain low, over a full five-year carbon budget period.

While some level of uncertainty and risk is inevitable for the later carbon budgets, the Second Carbon Budget begins in only five years. Given the significant risks associated with uncertain assumptions, a lack of supporting policy, and heavy reliance on NETs, the Scottish Government should ensure that the proposed monitoring framework is robust. If assumptions are shown to be invalid, adjustments must be made to the pathway to compensate. To enable this, indicative annual emissions and indicator pathways should be included in the final CCP. Effective monitoring and evaluation will be essential to ensure delivery remains on track, together with robust contingency planning to allow the plan to adapt to evolving circumstances.

| Figure 2 Distribution of emissions reduction by sector in the draft Climate Change Plan |

Description: The majority of the emissions reductions seen in Scotland to date have been in the mostly reserved energy supply sector. Emissions savings need to broaden, particularly into the mostly devolved transport, buildings, and agriculture and land use sectors. Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; Scottish Government (2025) Scotland’s Draft Climate Change Plan: 2026-2040; CCC analysis. Notes: See Chapter 3. |

| Figure 3 Assessment of policies and plans |

Description: Plans that are either credible or have only some risks attached are in place covering the majority of emissions reductions required to meet the First Carbon Budget. However, the Scottish Government is relying on emissions reductions where there are significant risks or insufficient plans in place, and on areas in which we have identified methodological concerns, to meet the Second and Third Carbon Budgets. Description: Plans that are either credible or have only some risks attached are in place covering the majority of emissions reductions required to meet the First Carbon Budget. However, the Scottish Government is relying on emissions reductions where there are significant risks or insufficient plans in place, and on areas in which we have identified methodological concerns, to meet the Second and Third Carbon Budgets.Source: Scottish Government (2025) Scotland’s Draft Climate Change Plan: 2026-2040; CCC analysis. Notes: See Chapter 5. |

Progress by sector

Transport

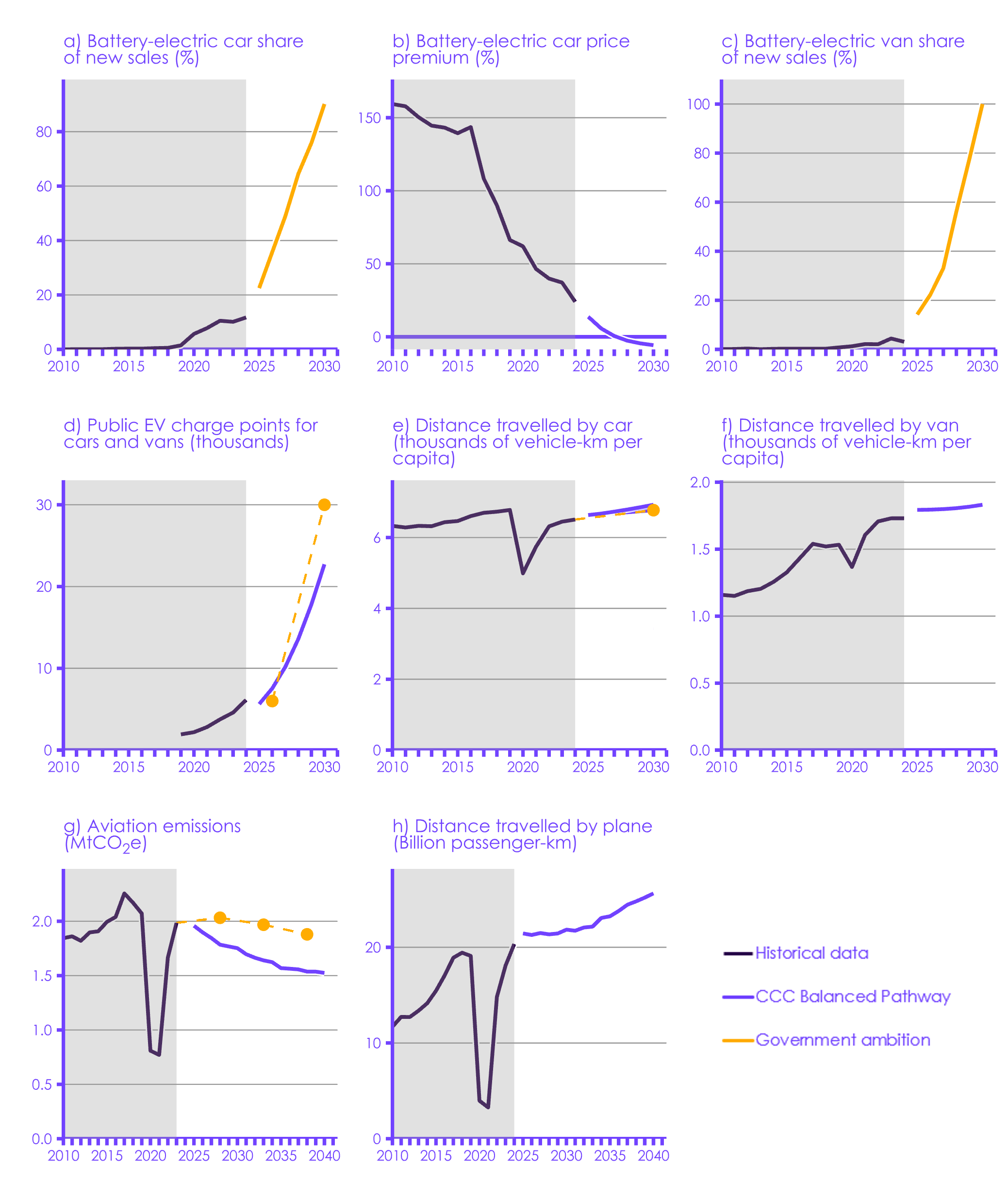

Transport is currently Scotland’s highest-emitting sector, responsible for around a third of emissions in 2023. In the First Carbon Budget period, 40% of the required emissions reductions are projected to come from transport.

- The number of battery-electric cars on roads in Scotland increased by 38% in the year to September 2025, supported by strong policy in the ZEV mandate and targeted funding. The draft CCP pathway requires EV sales to continue growing rapidly, in line with the Climate Change Committee’s (CCC) Balanced Pathway in our 2025 Scotland’s Carbon Budgets advice. Sales go beyond the mandate, driven by a rapid fall in EV prices together with the already lower running costs. The price premium of a new EV compared to a new petrol car dropped to 19% as of September 2025, from 24% in 2024.

- Public charge points across Scotland are showing impressive growth and increased by approximately 34% to over 6,000 in 2024, meeting the Scottish Government’s target two years early, although the distribution across Scotland varies and satisfaction could be substantially improved. A cross-pavement charging grant pilot worth up to £3,500 per household is available to enable access to the lower costs of home charging.

- Aviation emissions abatement in the draft CCP is heavily reliant on the success of the UK-wide sustainable aviation fuel (SAF) mandate and assumed efficiency improvements. No new aviation policy is committed to in the draft CCP. Significant policy gaps remain UK-wide to ensure the aviation sector takes responsibility for mitigating its emissions and ultimately achieving Net Zero for the sector by 2050. This includes paying for permanent engineered removals to balance out all remaining emissions.

Agriculture and land use

Progress in agriculture and land use has been mixed. While there have been increases in peatland restoration and tree planting, tree planting rates have not been sustained. There are significant risks for agriculture due to the lack of detail in the Agricultural Reform Programme and there is a lack of any policy to decarbonise non-road mobile machinery.[1]

- There has been a significant increase in peatland restoration recently, with rates almost doubling over two years to 14,900 hectares in 2024/25 – the highest rates seen to date. A five-year Peatland ACTION Partnership Plan was published in December 2025 setting out details on the peatland sector’s capacity, skills, and finance in support of reaching future restoration targets.

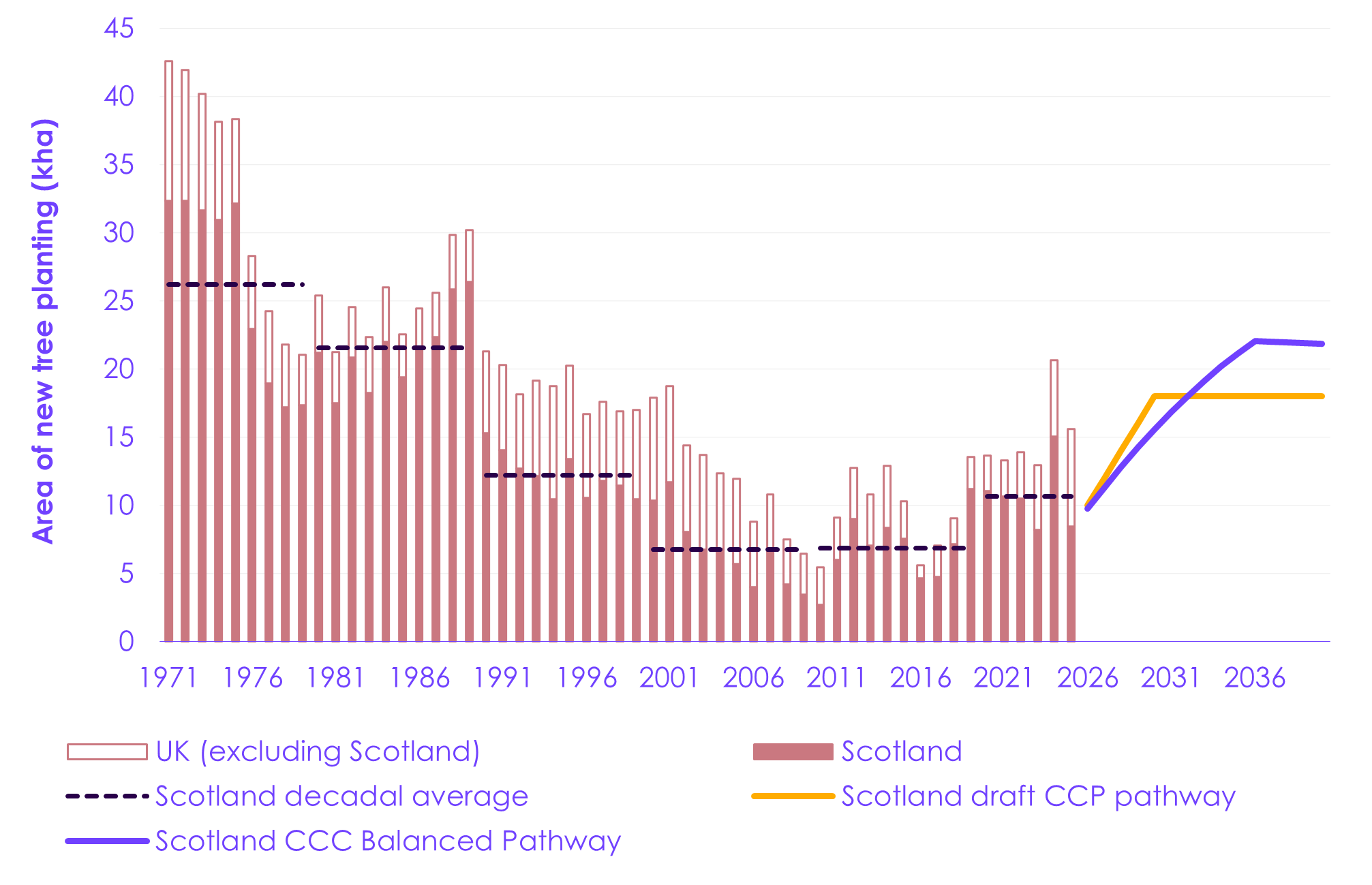

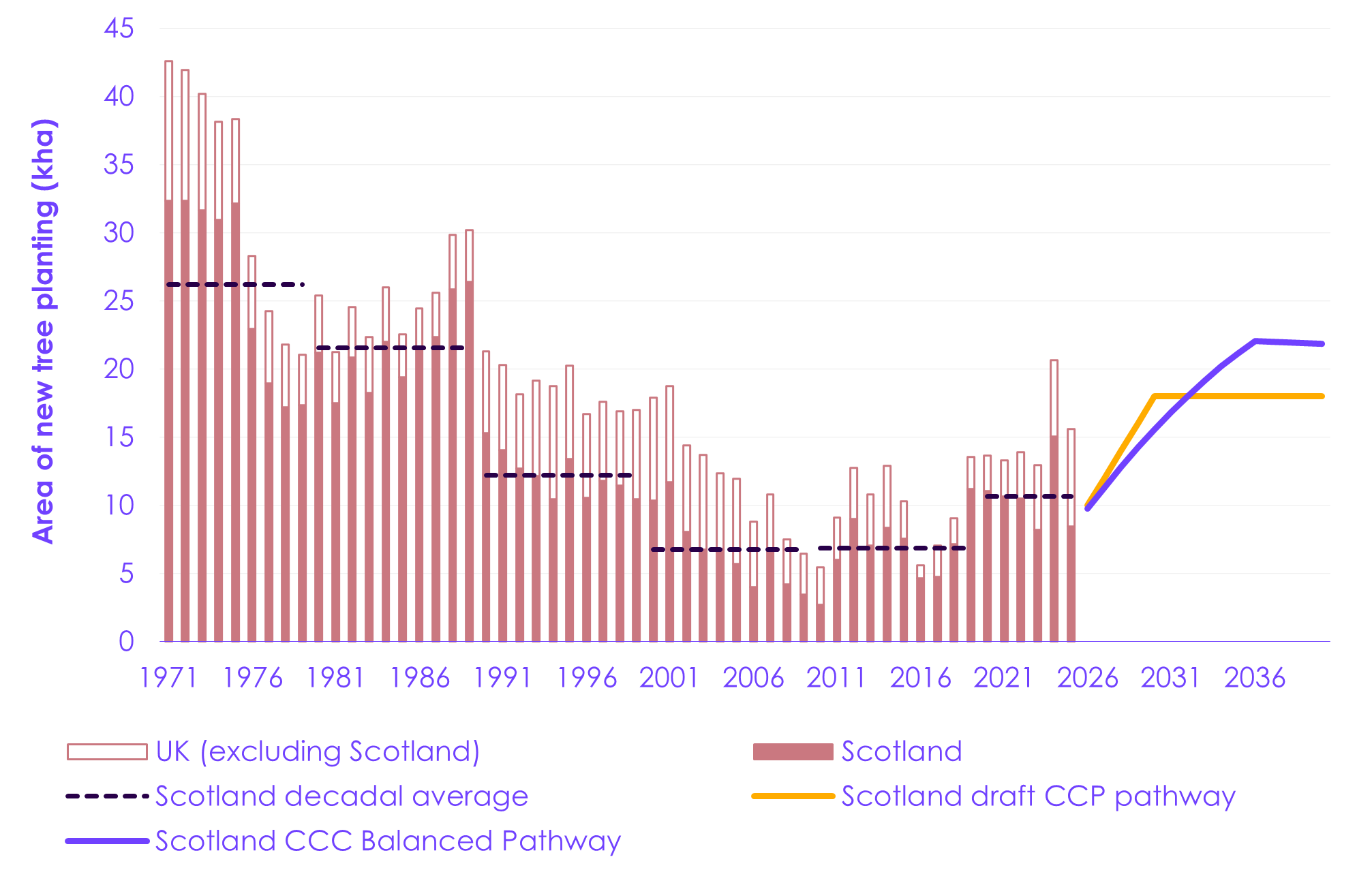

- The trend in tree planting rates has been less sustained. In 2023/24, woodland creation rates in Scotland reached 15,000 hectares – the highest levels seen since 1990 (Figure 4), demonstrating that rapid increases are possible. However, cuts to the Forestry Grant Scheme meant rates almost halved in 2024/25 to 8,500 hectares. With a target to reach, and crucially to maintain, 18,000 hectares of new woodland creation by the end of this decade, consistent progress is urgently needed. Funding has been increased in the 2025/26 and 2026/27 budgets, but remains at levels lower than 2023/24. Stop-start funding leads to uncertainty and damages supply chains.

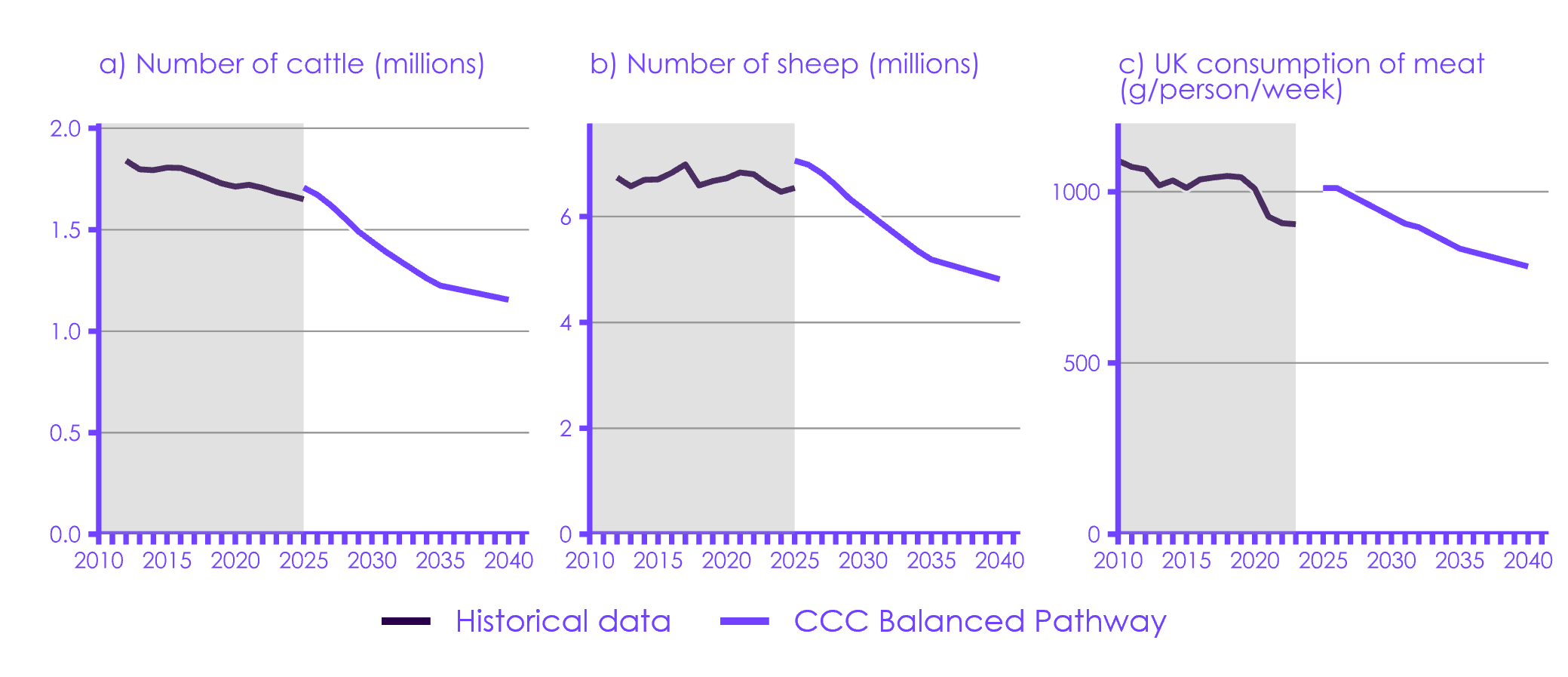

- Livestock numbers have been steadily declining in Scotland, as has UK-wide meat consumption, which is the biggest market for Scottish meat. The draft CCP includes no proactive measures to reduce livestock numbers beyond projections based on these existing long-term trends.

- Scotland’s land use sector will play an important role in reaching both Scotland’s and the UK’s Net Zero ambitions through its high potential for woodland creation and peatland restoration. The draft CCP does not currently set out how this will be delivered, in terms of the scale and type of land required to transition from agriculture.

| Figure 4 Tree planting rates in Scotland and the UK |

Description: Scotland has consistently delivered the highest planting rates in the UK. Though woodland creation rates have started to rise in the 2020s, they remain far below the rates achieved in the 1970s and 1980s. Description: Scotland has consistently delivered the highest planting rates in the UK. Though woodland creation rates have started to rise in the 2020s, they remain far below the rates achieved in the 1970s and 1980s.Source: Forest Research (2025) Time Series; CCC analysis. Notes: See Chapter 4. |

Buildings

The Scottish Government has a target to decarbonise heating systems in all buildings where ‘reasonable and practicable to do so’ by 2045. However, policies and plans to deliver the scale-up in low-carbon heating installations required to meet this target are currently missing.

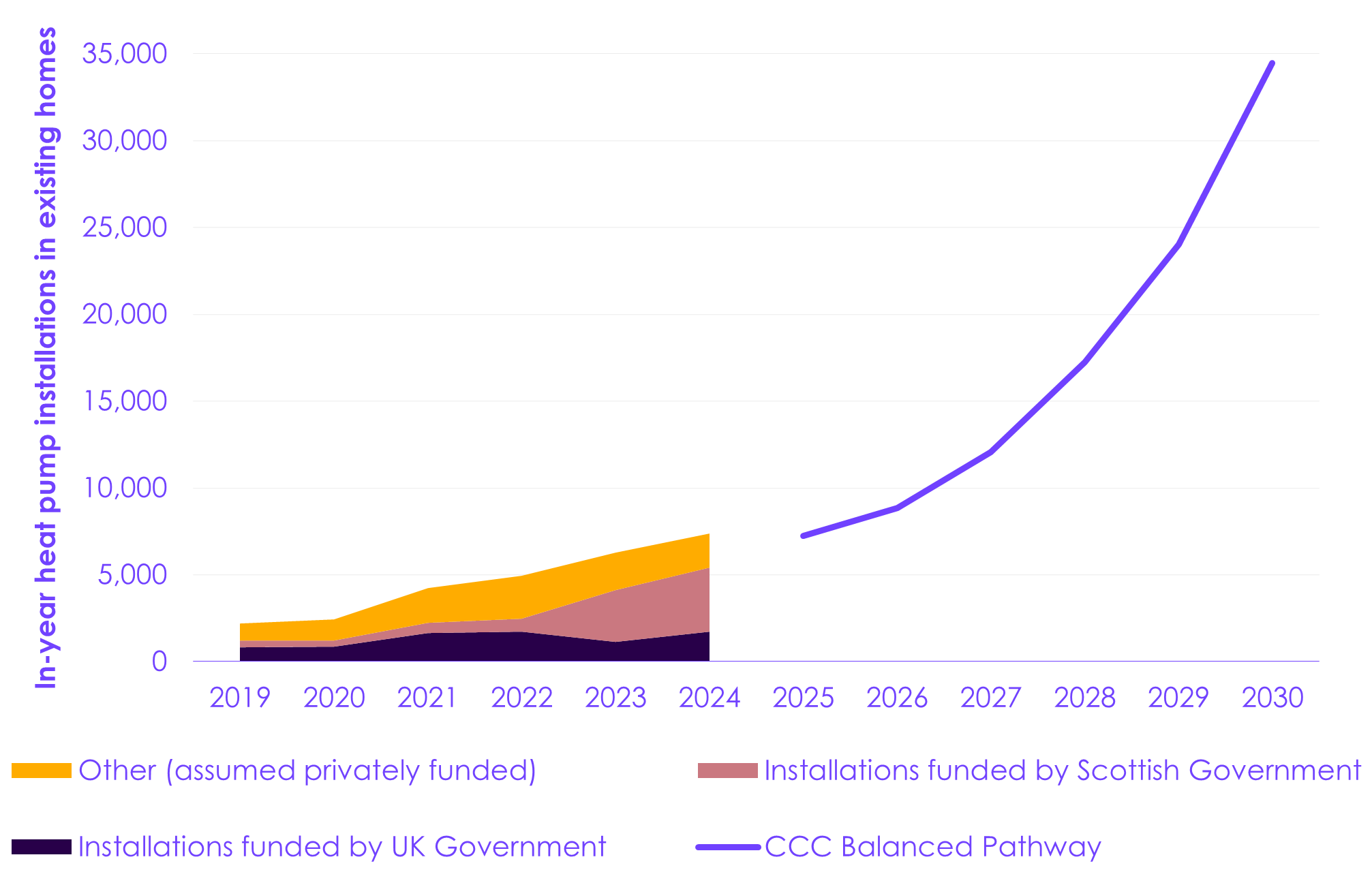

Emissions reductions proposed over the next decade are unambitious – with emissions falling by an average of only 0.1 MtCO2e per year over the first two carbon budgets, then accelerating extremely rapidly to 0.4 MtCO2e per year in the late 2030s, over the third carbon budget period. This ‘delay and catch-up’ approach carries significant risk. A more credible approach would be to build on, and accelerate, the recent steady increase in heat pump installations, allowing supply chains to grow and costs to reduce.

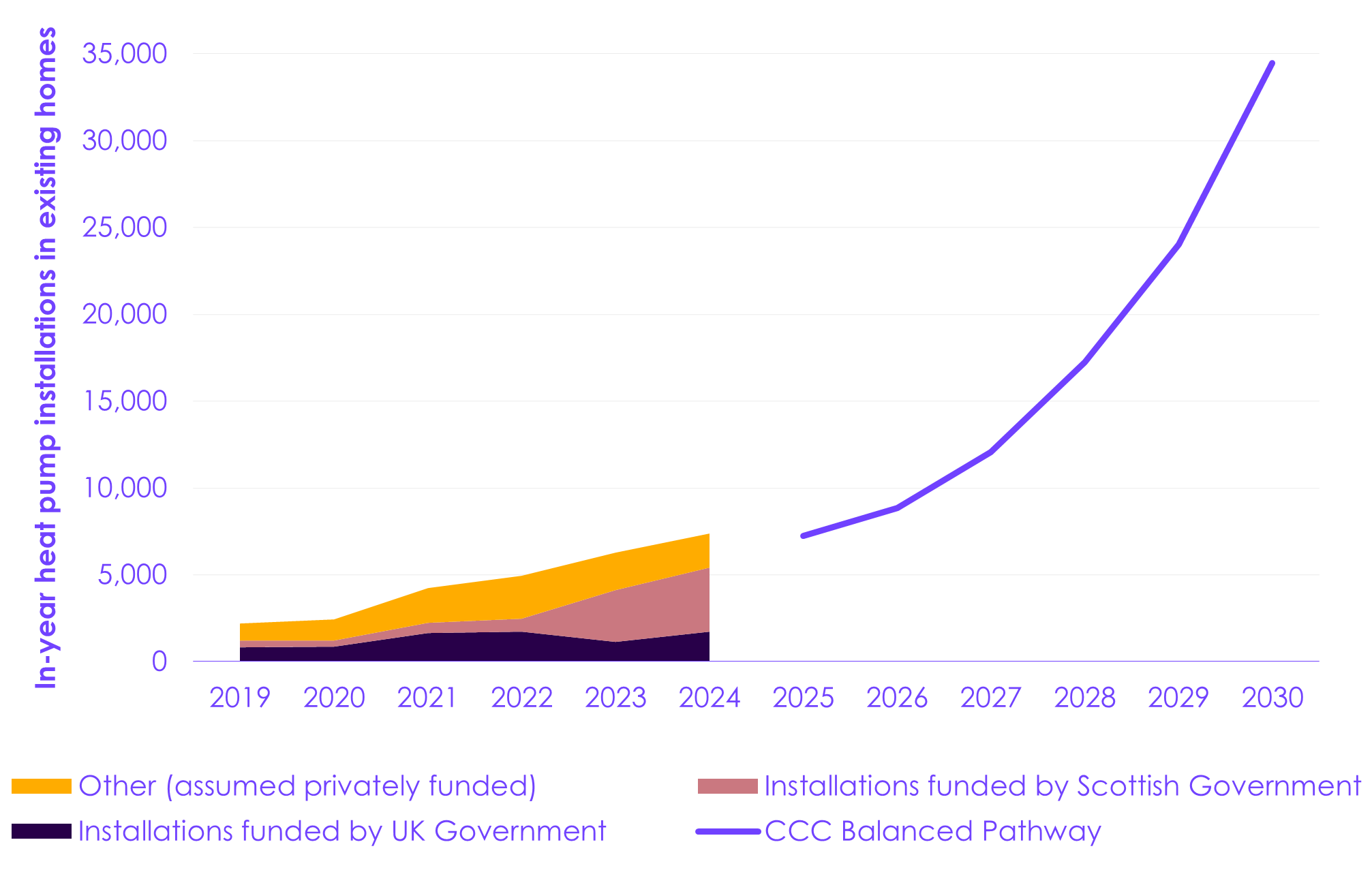

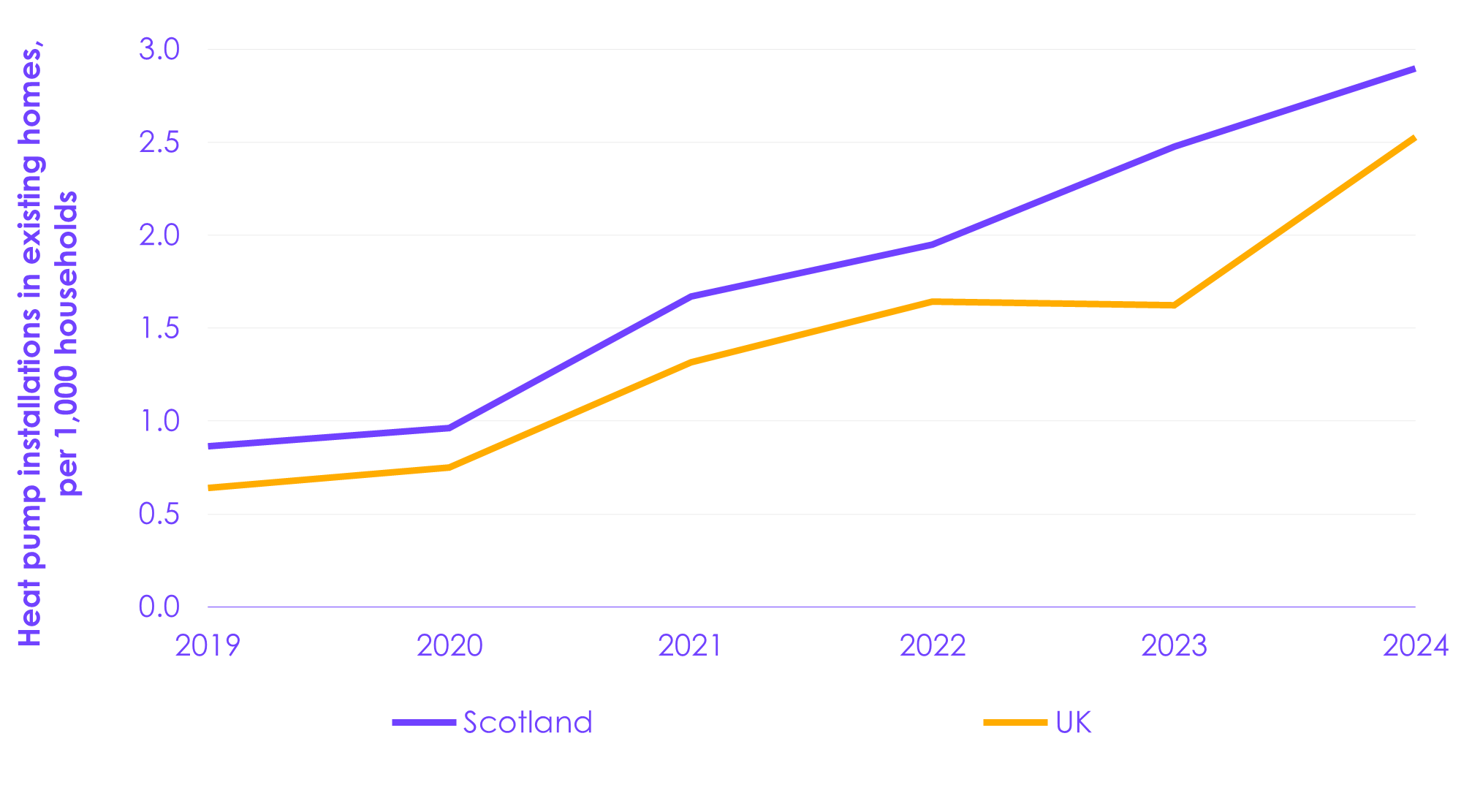

- Heat pump installations in Scotland have been steadily growing over the 2020s, with an 18% increase between 2023 and 2024, driven by an increase in installations under the Home Energy Scotland and Warmer Homes Scotland schemes (Figure 5). A higher proportion of Scottish homes have a heat pump compared to the UK as a whole.

- The CCC Balanced Pathway sees a rapid increase in heat pump installation rates, in line with those seen in similar European countries like the Netherlands and Ireland, reaching a maximum growth rate of 42% by 2028.

- The expected roll-out of heat pumps is not given in the draft CCP and should be included in the final CCP to ensure progress can be effectively tracked in the monitoring and evaluation framework.

- The Scottish Government offers generous grants and interest-free loans, providing a good incentive for households. However, they are currently only committed until the end of this financial year. The Scottish Budget 2026-27 confirmed £335 million of funding to extend support for low-carbon heating and energy efficiency into the coming financial year. However, the Scottish Government has yet to confirm that this will be used to continue existing grant schemes and has not yet set out plans for continued funding beyond this. Longer-term certainty is needed.

- It has been two years since the Scottish Government initially consulted on the Heat in Buildings Bill, which the Committee described in our 2023 Progress in reducing emissions in Scotland report as a potential template for other parts of the UK. It is therefore disappointing that there are still no alternative measures to the initial proposals for regulations to upgrade properties at the point of sale.

- The Scottish Government sees a significant role for heat networks in buildings, potentially delivered by requiring certain buildings to connect. However, further plans are needed on how this will be implemented.

- Scotland currently has regulations requiring minimum energy efficiency standards in the social-rented sector, but not in other existing buildings.

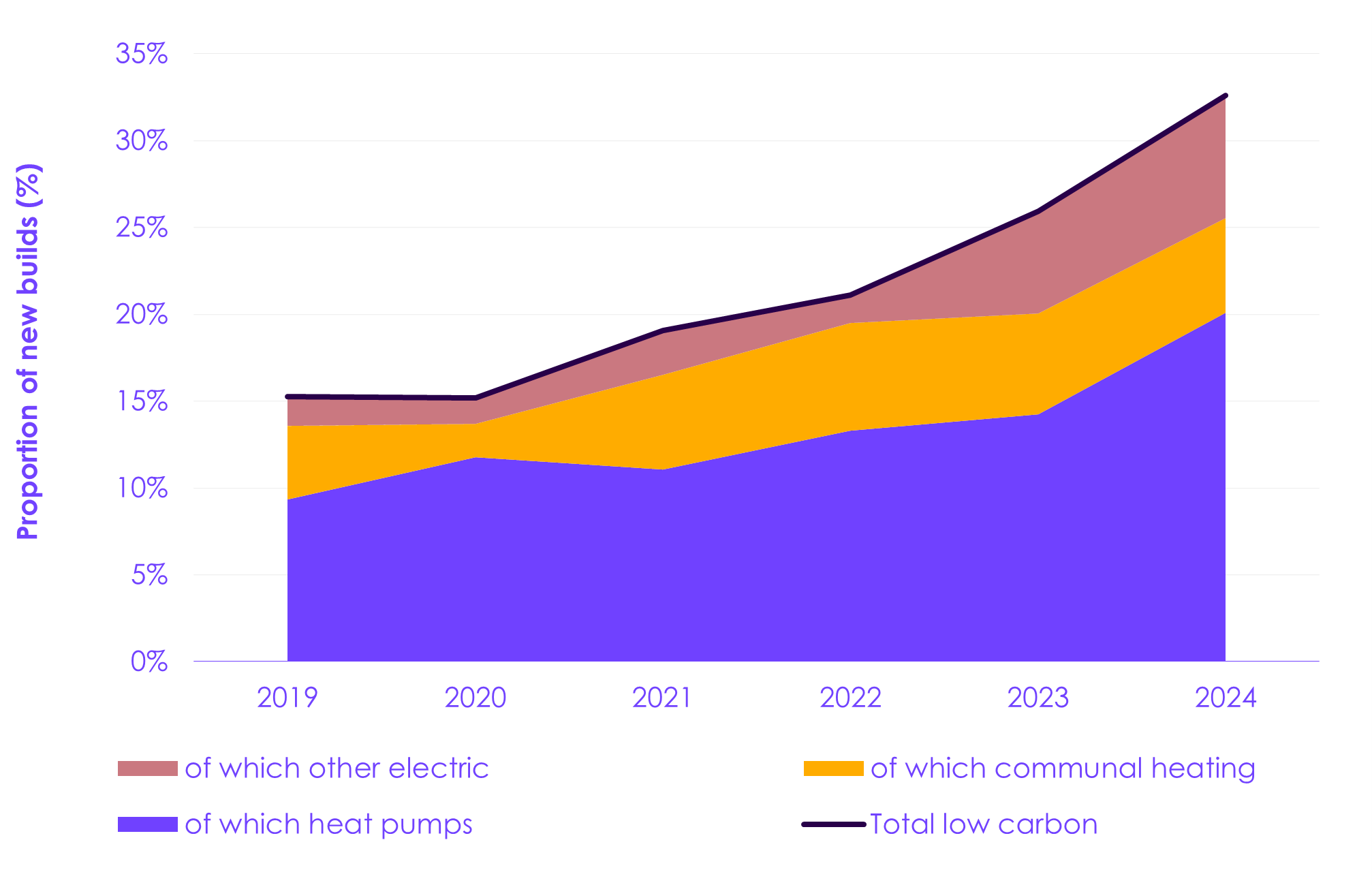

- There has been progress in new buildings, with the New Build Heat Standard requiring that new buildings with warrant applications made from April 2024 be built with a low-carbon heating system. In 2024, around one-third of new homes in Scotland were constructed with a low-carbon heating system, this is expected to increase over the coming years. The majority of these (62%) were heat pumps, with 22% being less efficient direct electric technologies. The rest were communal heating systems.

- On 21 January 2026, the UK Government published its Warm Homes Plan. This includes steps announced at the Budget to remove some levies from energy bills. This is a positive step forward. However the ratio of electricity to gas prices remains high, meaning that many properties will not yet be able to see the benefits of reduced running costs from heat pumps, which are a highly efficient technology.

| Figure 5 Historic heat pump deployment in existing homes compared to the CCC’s Balanced Pathway |

Description: Heat pump installations have grown steadily over the last five years in Scotland but need to accelerate rapidly in order to reach rates required for Net Zero. Description: Heat pump installations have grown steadily over the last five years in Scotland but need to accelerate rapidly in order to reach rates required for Net Zero.Source: Energy Savings Trust (2025) Scotland Energy Performance Certificate database; Scottish Government (2025) Heat in Buildings Progress Report 2025; Microgeneration Certification Scheme (2025) Data Dashboard; CCC analysis. Notes: See Chapter 4. |

Waste management

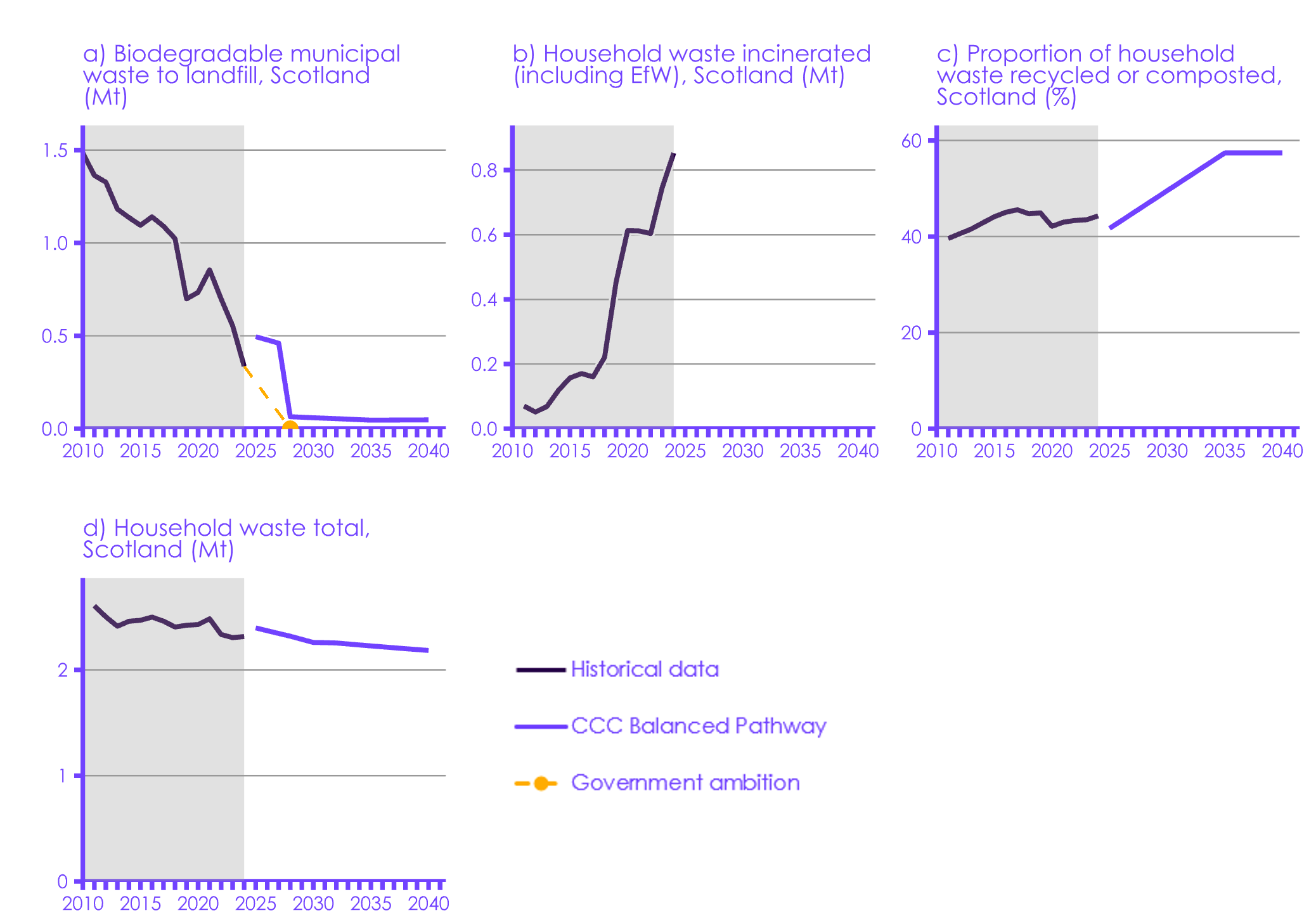

There has been little progress in reducing emissions from waste over the past decade. Although there have been small reductions in the total volume of waste produced by households, household recycling rates have not improved notably for many years, which risks the delivery of emissions reduction without further action. While Scotland has significantly reduced the volumes of waste sent to landfill in recent years, there has been a corresponding growth in emissions from waste incinerated via energy from waste.[2]

Sectors with most policy powers reserved to the UK Government

To date the majority of emissions reductions have been achieved in energy supply via action led by the UK Government. Going forwards this will need to broaden to sectors with many policy powers devolved to the Scottish Government. However, there are also important contributions from sectors with significant powers reserved to the UK Government. In particular, the Scottish Government has chosen a pathway that has significant dependencies on NETs, which are responsible for around a quarter of the required emissions reduction in the Third Carbon Budget (Figure 2). A co-ordinated approach will be essential.

- Business and industrial process: the draft CCP relies on three main policies: the UK Emissions Trading Scheme (ETS); the proposed industrial decarbonisation programme; and industrial carbon capture and storage (CCS). There are significant risks to achieving the required emissions reductions in the latter two.

- We welcome the proposed launch of the industrial decarbonisation programme in 2026. Where electrification is the economically rational choice, the Scottish and UK Governments should work together to ensure that businesses and industries are incentivised to adopt electric technologies.

- Following the end of operations of some potential industrial CCS customers, the Scottish Government will need to work with the UK Government to ensure that the Acorn project is financially viable. The UK Government should provide greater clarity on timelines for the Scottish cluster.

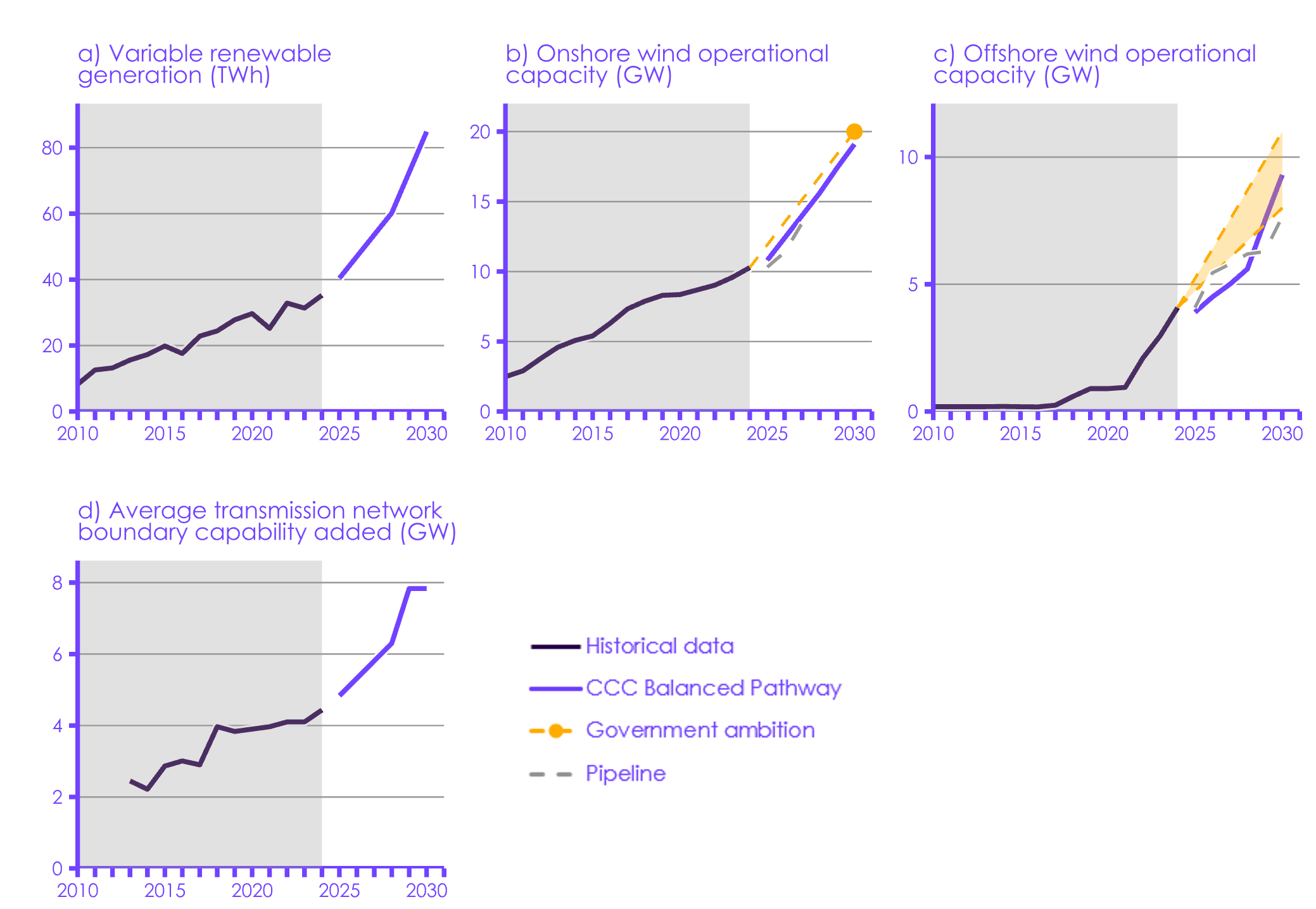

- Energy supply: deployment of variable renewable electricity generation is continuing to increase in Scotland, with 1.1 GW of offshore and 1.3 GW of onshore wind capacity deployed in 2024.

- Remaining emissions in electricity generation come predominantly from the Peterhead gas-fired power station. Reducing emissions further relies on the continued roll-out of wind and solar generation and of network capacity to accommodate it. The draft CCP sets out plans to replace Peterhead with a CCS-enabled gas plant.

- For the oil and gas sector, the plan sets out an intention to manage the transition via skills programmes and targeted investment, including in Grangemouth and North East Scotland. However, further detail is needed on how these measures translate into secure, high-quality employment opportunities in affected regions, particularly where the pace of job creation in growing sectors remains uncertain.

- NETs: the Scottish Government has chosen a pathway with a high dependence on NETs, but it is not clear how the Scottish Government’s plans for a significant ramp up in NETs in the late 2030s, over the Third Carbon Budget period, align with UK-wide plans for where they will be geographically placed. What is more, UK-wide plans currently lack certainty and funding. This is an area of significant risk for achieving the Third Carbon Budget.

Priority actions

As set out in the Act, the Scottish Government must now produce a final Climate Change Plan, which will set out how Scotland will meet its emissions targets over the next 15 years. Beyond this, the Scottish Government will publish important new strategies and plans in a number of crucial areas over the coming months, including the Heat in Buildings Strategy and Delivery Plan and the Fourth Land Use Strategy. These new documents should be used to move forward with implementing the key measures set out in the plan at pace.

We have 18 priority recommendations for the Scottish Government to achieve this – within these, there are six core themes which require particular focus over the coming year:

- Produce an effective and credible final Climate Change Plan: the Committee’s assessment of the draft CCP, set out in this report, has identified a number of improvements that should be included in the final CCP. These include addressing the risk from the methodological concerns around the assumed inventory change for peatlands and the underlying temperature assumptions for buildings. The final CCP should also make clear how energy-saving practices seen when gas prices were high will be maintained without adverse effects such as underheating of homes. Further key actions to reduce delivery risk in achieving the carbon budgets are given in the following core themes. As part of the final CCP, the Scottish Government should also set out its finalised monitoring and evaluation framework, including indicative annual pathways for sectoral emissions and all key indicators of progress. An explicit inclusion of contingency options should also be included to make up for any potential shortfalls in the pathway (R2026-001, R2026-002, and R2026-003).

- Implement a clear delivery plan for decarbonising home heating: the Scottish Government has an opportunity to lead the way in the UK for buildings decarbonisation, with significant policy powers within its gift. However, the draft CCP lacks policy to deliver this (R2025-100, R2025-101, and R2026-006).

- The Scottish Government should confirm that funding announced in the Scottish Budget 2026-27 will be used to continue existing grants and top-up loans to support households with heat pump installations. Furthermore, it should set out plans for the continuation of funding beyond the next financial year.

- The upcoming Heat in Buildings Strategy and Delivery Plan should be published as soon as possible this year and ensure conditions are in place to deliver the required scale-up in low-carbon heat and energy efficiency measures. This could be via a combination of continued financial support, regulation, support for skills, public engagement on the benefit of heat pumps, and leading by example and helping to build supply chains in public sector buildings.

- There are homes that would already benefit from lower heating bills by installing a heat pump. The UK Government’s Warm Homes Plan includes steps announced at the Budget to remove some levies from energy bills and provide funding for fuel poor homes across the UK, following the forthcoming closure of the Energy Company Obligation scheme. The Scottish Government should develop plans accordingly, considering the homes that will see reduced running costs, to ensure that progress in heat pump deployment continues. Delays to decision-making are postponing opportunities for emissions reductions and putting targets for decarbonisation of buildings at risk.

- In addition, the delivery plan should include details of plans to ensure buildings connect to heat networks where appropriate.

- The delivery plan should also include proposals for improving energy efficiency in existing buildings, including a commitment to implement minimum energy efficiency standards for privately rented homes, and revised standards for social housing.

- Around 25% of homes in Scotland are within tenement buildings, with nearly a third of these built pre-1919. Meeting the Scottish Government’s targets will require an effective approach to decarbonising these buildings, which can be challenging due to traditional construction and the need to coordinate works with multiple owners. The delivery plan needs to address these challenges, including through developing appropriate governance frameworks to enable the installation of communal low-carbon heating systems where appropriate.

- Produce a clear strategy for delivering the required land use changes: Scotland leads the UK on planting new woodlands and restoring peatlands. These two actions will contribute significantly to both Scotland’s and the UK’s emissions targets. The upcoming Fourth Land Use Strategy needs to be clear on the types and locations of land that will be needed for each action, taking a joined-up approach with agriculture. Regulation and long-term public funding should also ensure that farmers are able to take up low-regret measures to reduce emissions from managing crops and livestock. Funding for woodland creation and peatland restoration should be sustained and sufficient to ensure delivery in line with the Government’s ambition (R2025-095, R2025-096, and R2025-097).

- Enable the rapid transition to electric transport: the draft CCP pathway sees a rapid acceleration in EV sales. We expect this to be possible, driven by falling prices and a stable UK-wide policy landscape, but the Scottish Government will need to continue to support the roll-out of public charge points across Scotland in all regions and through positive public engagement on the benefit of EVs to help grow demand. This should be complemented by improvements to public transport across Scotland (R2025-093 and R2025-094).

- Enhance confidence in the delivery of negative emissions technologies: the Scottish Government has chosen a draft CCP pathway that includes a significant level of reliance on NETs. The Scottish Government should publish a delivery plan setting out the expected role of each technology and the actions required to deliver them. A co-ordinated approach with the UK Government and plans for UK-wide NETs will be needed to ensure successful delivery, and the Scottish Government should set out how they intend to make Scotland an attractive location for NETs, such as through efficient planning, permitting, and consenting processes (R2026-004).

- Continue to strengthen public and business engagement with a focus on impactful low-carbon choices and proactive transition plans: the draft CCP reiterates the Scottish Government’s strong commitment to public engagement. However, current approaches need to have an increased emphasis on the most impactful low-carbon household choices. In addition, the Scottish Government needs to build upon positive steps in the draft CCP and the Green Industrial Strategy to ensure that proactive transition plans are agreed with communities, workers, and businesses likely to be affected by the Net Zero transition and the reduced production and use of fossil fuels (R2025-091 and R2025-092).

The Scottish Government has devolved powers to deliver in each of these key areas. But it is also vital that the Scottish and UK Governments work together effectively to achieve progress on areas critical to their shared objectives. To deliver its contribution to UK-wide targets, including the 2030 Nationally Determined Contribution, Scotland will need to continue its strong progress in rolling out renewable electricity generation and ensure development of electricity networks can keep pace. The Scottish Government should act to accelerate planning and consenting for transmission infrastructure to achieve this (R2026-005). Significantly ramping up rates of tree planting and peatland restoration in Scotland will also represent a strong contribution to UK-wide decarbonisation. Rapid and effective action to make electricity cheaper – building on the positive steps taken in the Budget 2025 – and a final investment decision for the Acorn project are two critical enabling actions that the UK Government can take to support decarbonisation in Scotland.

Now that the Scottish Government has adopted its new system of carbon budgets and has developed a draft plan to deliver them, it is essential to make strong progress on delivery. The key lesson from the previous system of annual targets was that ambition alone is not enough – this needs to be backed up by timely, effective policy and implementation. Effective monitoring and evaluation will also be essential to ensure delivery remains on track, together with robust contingency planning to allow the plan to adapt to evolving circumstances. The coming year presents a critical opportunity for the Scottish Government to demonstrate commitment to its ambition by ensuring that policy is well set up to support markets to continue to grow, costs to continue to fall, and emissions to continue to reduce.

Chapter 1: Scotland’s emissions reduction targets

This chapter summarises the legislative framework in place to reduce greenhouse gas (GHG) emissions in Scotland.

Our key messages are:

- Under the Climate Change (Scotland) Act 2009 (the Act), Scotland has a target to reach Net Zero emissions by 2045. In 2024, the Act was amended to replace interim decadal and annual emissions reduction targets with a framework of carbon budgets.

- The Scottish Government has since made rapid progress in legislating the level of the carbon budgets.

- Now that the new framework is in place and the Scottish Government has published Scotland’s Draft Climate Change Plan: 2026-2040 (the draft CCP) for consultation, the Scottish Government should move fast to deliver on its ambitious targets.[3]

1.1 The Climate Change (Scotland) Act

The Act sets the framework for the Scottish Government to address climate change.[4] Emissions in Scotland are covered by both Scotland’s targets, set under the Act, and UK-wide targets, set under the UK Climate Change Act (2008) and as part of the United Nations Framework Convention on Climate Change (UNFCCC) process.[5]

- Scotland’s Act was amended in 2019 to include a target to reach Net Zero GHG emissions by 2045 and interim decadal emissions targets for 2020, 2030, and 2040.[6]

- Scotland’s target to achieve Net Zero by 2045 represents a fair contribution towards UK and global efforts under the Paris Agreement to limit global average temperatures. It is appropriate that Scotland’s target is earlier than the UK-wide target to reach Net Zero by 2050, because Scotland has proportionally more land suitable for tree planting and strong potential for engineered GHG removals.

- The Act was amended in 2024 to repeal the interim targets and introduce five-yearly carbon budgets aligned with the 2045 Net Zero target.[7] This is our first progress report since the Committee offered advice to the Scottish Government on a carbon budget system, and since new targets were legislated.

- Emissions from international aviation and shipping are included in Scotland’s carbon budgets and Net Zero target.

1.2 Scotland’s carbon budgets

In June 2025, the Scottish Government laid the Climate Change (Scotland) Act 2009 (Scottish Carbon Budgets) Amendment Regulations 2025 in the Scottish Parliament.[8]

- The regulations proposed setting Scotland’s carbon budgets, including Scotland’s share of international aviation and shipping emissions, at annual average levels of emissions that will be:

- 57% lower than 1990 levels for the First Carbon Budget (2026 to 2030), implying a 12% reduction from levels in 2023.

- 69% lower than 1990 levels for the Second Carbon Budget (2031 to 2035), implying a 36% reduction from levels in 2023.

- 80% lower than 1990 levels for the Third Carbon Budget (2036 to 2040), implying a 59% reduction from levels in 2023.

- 94% lower than 1990 levels for the Fourth Carbon Budget (2041 to 2045), implying an 88% reduction from levels in 2023.

- These carbon budgets are given as five-year average percentage reductions from the 1990 baseline.[9] They are consistent with the Committee’s 2025 Scotland’s Carbon Budgets advice and with reaching Net Zero by 2045.

- In October 2025, the Scottish Parliament approved the proposed regulations, voting to set Scotland’s carbon budgets in line with the Committee’s recommendations.

It is positive that the Scottish Government has taken swift action to set the levels of the carbon budgets. This provides a firm basis for timely development of policy to deliver the carbon budgets and will, in turn, give confidence to businesses and households on the emissions reduction actions that will be required. Now that the new framework is in place, the Scottish Government needs to deliver against its ambitious targets.

1.3 Progress towards Scotland’s emissions reduction targets

In the following chapters, we assess Scotland’s progress in reducing emissions since our last progress report:

- In Chapter 2, we consider progress in the emissions data for Scotland that has been published since our last progress report, covering emissions in 2022 and 2023.

- In Chapter 3, we review the draft CCP published in November 2025, considering the overall approach and discussing the Scottish Government’s intended emissions reduction pathway as set out in the plan.

- In Chapter 4, we assess progress on a range of delivery indicators, based on the latest robust data available (which varies between 2022 and 2025 depending on the indicator), and compare these against the changes that are needed to meet the draft CCP pathway.

- In Chapter 5, we provide our assessment of policy developments over the period since our last progress report, between March 2024 and 21 January 2026, that are relevant to meeting Scotland’s emissions targets. This includes our assessment of the credibility of the policies and plans set out to meet Scotland’s carbon budgets in the draft CCP.

Chapter 2: Progress in reducing Scotland’s emissions

In this chapter, we review trends in the latest emissions data in total and by sector, with a focus on changes since our last progress report.[10] This covers the period 2021 to 2023, with 2023 being the latest available data. We focus on territorial emissions, that is, emissions within Scotland’s territorial borders and including Scotland’s share of international aviation and shipping (IAS). This is the basis on which Scotland’s legally binding targets are set. However, we also track imported emissions.

Our key messages are:

- Scotland’s territorial greenhouse gas emissions were 39.6 MtCO2e in 2023.[11]

- Emissions were 51.3% lower than in 1990. Relative to emissions in 1990, Scotland is now more than halfway to Net Zero emissions. This milestone was achieved in Scotland two years earlier than the UK as a whole, which provisionally halved its emissions against the 1990 baseline in 2024.

- Reductions since 1990 have been mainly driven by the energy supply sector, with smaller contributions from the business and industrial process; land use, land use change and forestry (land use); and waste management sectors.

- Between 2021 and 2023, emissions fell by 1.1 MtCO2e (2.6%), with emissions falling year-on-year in both 2022 and 2023 following a slight increase in emissions in 2021.

- The emissions reduction between 2021 and 2023 was largely driven by the residential and public buildings (buildings) and energy supply sectors. Emissions from transport and land use increased over this period.

- The pace of emissions reductions will need to slightly increase to meet Scotland’s carbon budgets. This will increasingly require focus on the mostly devolved transport, buildings, and agriculture and land use sectors.

- Emissions from imports outside the UK have been relatively steady since 2009, following a drop after the financial crisis.

2.1 Scotland’s territorial emissions

2.1.1 Overall Scottish emissions

Scotland is now more than halfway to Net Zero emissions by 2045, with emissions having steadily fallen since the start of the century (Figure 2.1). Including its share of emissions from IAS, Scotland has achieved a 51.3% reduction in emissions when compared to 1990 levels (Table 2.1). This milestone was achieved in Scotland two years earlier than the UK as a whole, which provisionally halved its emissions against the 1990 baseline in 2024. This is because electricity supply emissions have decreased faster than in the UK as a whole.

- More than half of total reductions against the 1990 baseline have been achieved since the introduction of the Climate Change (Scotland) Act 2009 (the Act).

- Emissions fell in both 2022 and 2023. The pace of emissions reduction will need to slightly increase to meet Scotland’s carbon budgets.

- The average annual emissions reduction between the introduction of the Act in 2009 and 2023 was 1.6 MtCO2e per year. This will need to increase to an average annual reduction of 1.8 MtCO2e per year between 2023 and 2045 to meet Scotland’s emissions targets.

Description: Scotland is more than halfway to Net Zero emissions.

Description: Scotland is more than halfway to Net Zero emissions.| Table 2.1 Scotland’s territorial emissions and emissions changes for selected periods |

||

| Period | Value | |

| Emissions (MtCO2e) | 1990 | 81.2 |

| 2009 | 61.7 | |

| 2021 | 40.6 | |

| 2022 | 40.3 | |

| 2023 | 39.6 | |

| % change in emissions | 1990–2022 | -50.3% |

| 1990–2023 | -51.3% | |

| 2021–2022 | -0.7% | |

| 2022–2023 | -1.9% | |

| Annual average change (MtCO2e) | 1990–2023 | -1.3 |

| 2009–2023 | -1.6 | |

| Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; CCC analysis. Notes: 1990 numbers refer to the 1990 baseline. The baseline year is 1990 for CO2, methane, and nitrous oxide, and 1995 for F-gases. |

||

Emissions changes between 2021 and 2023

Between 2021 and 2023, emissions fell by 1.1 MtCO2e (2.6%), with emissions falling year-on-year in both 2022 and 2023 following a slight increase in 2021 as emissions rebounded from the COVID-19 pandemic.

- 2022 emissions were 40.3 MtCO2e, which is 50.3% below 1990 levels. This is a 0.3 MtCO2e (0.7%) reduction from 2021.

- 2023 emissions were 39.6 MtCO2e, which is 51.3% below 1990 levels. This is a 0.8 MtCO2e (1.9%) reduction from 2022.

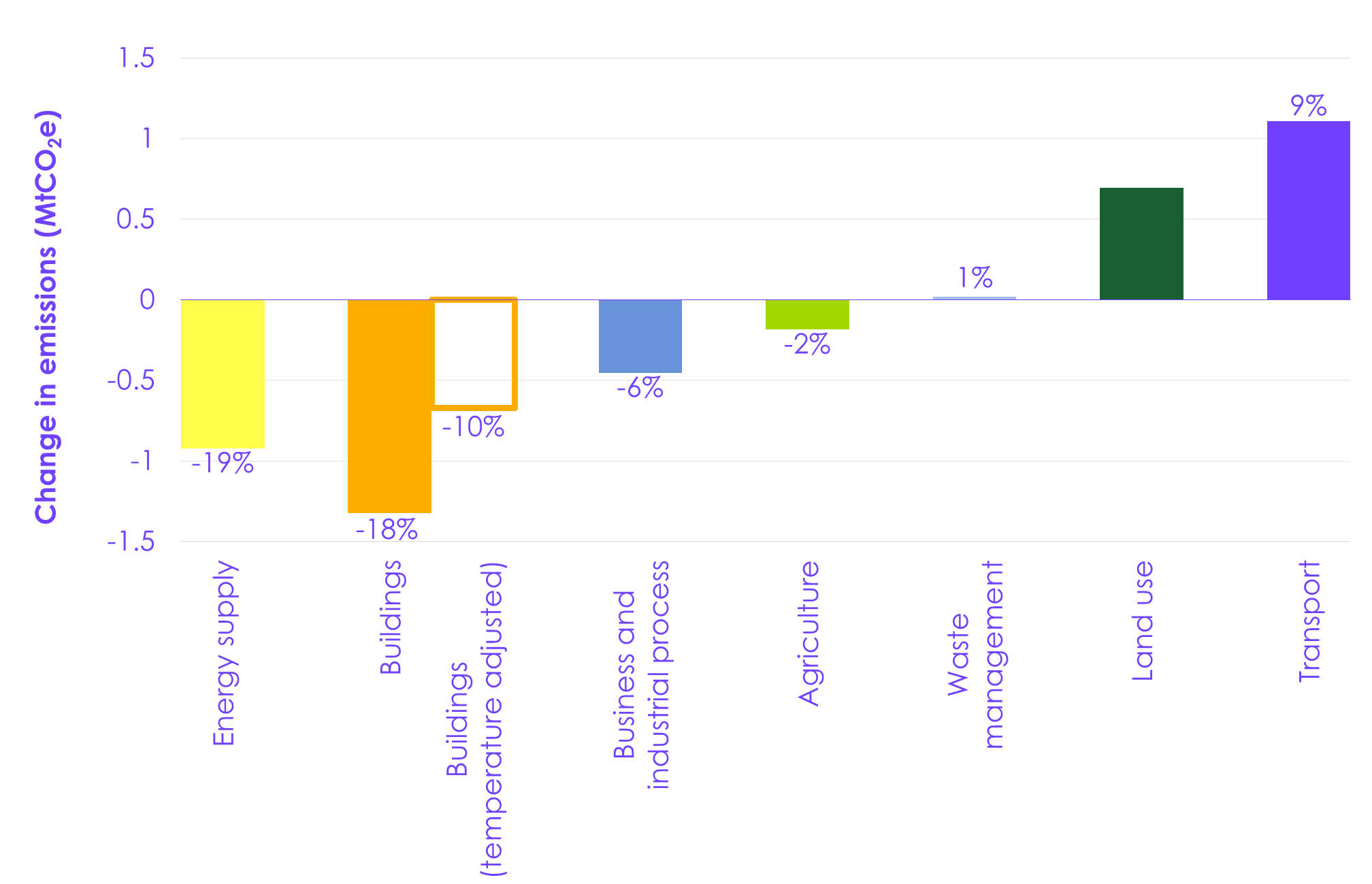

The emissions reductions between 2021 and 2023 were largely driven by the buildings and energy supply sectors. Emissions from transport and land use increased over this period (Figure 2.2).

- Emissions from buildings showed the largest sectoral decrease, falling by 1.3 MtCO2e, which is an 18% reduction for the sector. Emissions in this sector fell by 1.3 MtCO2e in 2022 and 0.1 MtCO2e in 2023.[12]

- Around half of the overall reduction was due to milder-than-average winter months in 2022 and 2023. Emissions vary considerably year-to-year due to annual variations in temperature. After adjusting for the effect of these short-term fluctuations in temperature on heating requirements, emissions in this sector fell by 0.7 MtCO2e, a 10% reduction.[13] This is likely to be driven by a behavioural response to record-high gas prices.

- Energy supply emissions fell by 0.9 MtCO2e between 2021 and 2023. Emissions in this sector increased by 0.3 MtCO2e in 2022 before falling by 1.2 MtCO2e in 2023.

- Around two-thirds of the overall reduction relates to a reduction in unabated gas generation in power stations. Around one-third of the reduction is due to reductions in emissions from oil refining and fuel use in oil and gas extraction.

- Transport emissions increased by 1.1 MtCO2e (9%) between 2021 and 2023. In 2022, emissions increased by 1.0 MtCO2e, with a further increase of 0.1 MtCO2e in 2023.

- This increase is largely due to aviation emissions continuing to rebound following the COVID-19 pandemic.

- Emissions from the land use sector increased by 0.7 MtCO2e between 2021 and 2023. Emissions increased by 0.1 MtCO2e in 2022 and 0.6 MtCO2e in 2023.

- This was largely due to a legacy of lower tree planting rates during the previous two decades, leading to a decline in the forestry carbon sink, as well as the removal of trees from peatlands under restoration management, leading to a net loss of carbon sequestration in the near-term.

The driving factors behind these sectoral changes are discussed further in Section 2.1.2 below.

| Figure 2.2 Change in Scotland’s emissions by sector (2021–2023) |

Description: The main reductions in emissions in between 2021 and 2023 were in energy supply (by 19%) and buildings (by 18%), while emissions from transport increased by 9%. Description: The main reductions in emissions in between 2021 and 2023 were in energy supply (by 19%) and buildings (by 18%), while emissions from transport increased by 9%.Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; CCC analysis. Notes: (1) Temperature-adjusted emissions are displayed to better represent the change in activities without the interannual fluctuations in temperature. (2) The year-on-year percentage change for land use has not been displayed due to this sector being comprised of a mixture of sources and sinks, making relative changes appear very dramatic. |

2.1.2 Emissions trends by sector

In this section, we discuss recent and longer-term trends in emissions, and the main factors driving these, within each sector.

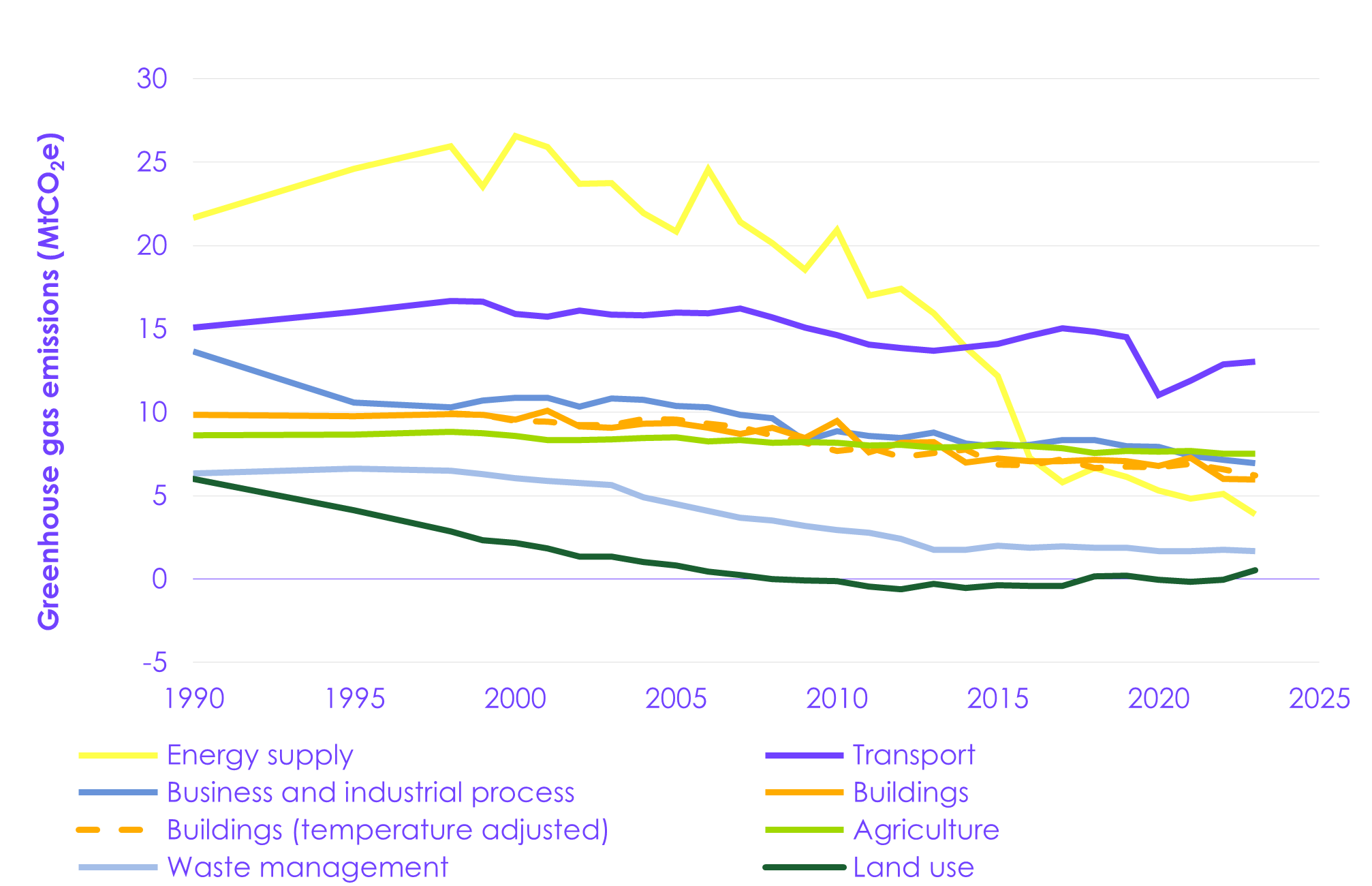

- Transport (comprising road, rail, aviation, and maritime transport) is currently Scotland’s largest source of emissions, followed by agriculture and business and industrial process (Table 2.2).

- The biggest driver of emissions reduction since 1990 has been energy supply. There have also been substantial reductions in the business and industrial process, waste management, and land use sectors (Figure 2.3).

| Table 2.2 Emissions by sector in 2023 |

|||

| Sector | Emissions (MtCO2e) | Sector | Emissions (MtCO2e) |

| Transport | 13.0 | Energy supply | 3.9 |

| Agriculture | 7.5 | Waste management | 1.7 |

| Business and industrial process | 7.0 | Land use | 0.5 |

| Buildings actual (temperature adjusted) | 6.0 (6.2) | ||

| Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; CCC analysis. Notes: Temperature-adjusted buildings emissions are displayed to better represent emissions without the interannual fluctuations in temperature. |

|||

| Figure 2.3 Scottish emissions by sector (1990–2023) |

Description: Large reductions in emissions have been observed since 1990 in the energy supply, business and industrial process, waste, and land use sectors (dominated by energy supply), with smaller changes across other activities. Description: Large reductions in emissions have been observed since 1990 in the energy supply, business and industrial process, waste, and land use sectors (dominated by energy supply), with smaller changes across other activities.Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; CCC analysis. Notes: (1) Temperature-adjustment is performed for buildings sectors where the impact of interannual variability in temperature has a noticeable impact on emissions. (2) The land use sector is a combination of positive sources of emissions and negative sinks of emissions. (3) ‘Buildings’ refers to residential and public buildings. |

Transport

Transport has been the highest-emitting sector in Scotland since 2014. Emissions have fallen by 14% since 1990, but most of this reduction has been the result of structural shifts in transport patterns following the pandemic.

- Surface transport: emissions from surface transport were 9.2 MtCO2e in 2023, 0.1 MtCO2e (1%) higher than in 2021. Emissions are now 3% lower than 1990 levels.

- In 2019, before the COVID-19 pandemic, emissions from surface transport were 6% higher than in 1990.[14] This was due to a 38% rise in vehicle-kilometres, driven in part by a 6% population increase since 1990 and an additional one million cars on the roads since 1994.[15];[16];[17] There has also been a shift towards larger petrol vehicles. These changes have partially offset efficiency improvements that reduce emissions.

- The pandemic caused a 19% drop in emissions during 2020, which rebounded to 9.3 MtCO2e in 2022 (7% below 2019 pre-pandemic levels). In 2023, year-on-year emissions reduced slightly to 9.2 MtCO2e. The sustained reduction compared to 2019 reflects a structural shift in transport patterns following the pandemic.

- Progress in this area is key to delivering economy-wide emissions reductions over the next decade. We expect that the transition to electric vehicles (EVs) will follow an

‘S-shaped’ adoption curve, starting slowly but accelerating rapidly, with purchase price parity being a key tipping point in the next few years (see Figure 4.1b). Despite overall car-kilometres increasing by 14% between 2021 and 2023, car emissions have increased by only 4%.[18] This could provide early evidence of EVs beginning to have a measurable impact on emissions in Scotland as well as continued improvements in efficiencies for petrol cars.

- Aviation: emissions from aviation were 2.0 MtCO2e in 2023, 1.2 MtCO2e (157%) higher than in 2021. Emissions are now 41% higher than 1990 levels.

- Aviation emissions increased by 48% between 1990 and 2019 (pre-COVID-19 levels).

- In 2023, emissions almost rebounded to pre-COVID-19 levels at 4% below 2019 levels, which has been a key factor in the increase in overall transport sector emissions in the past two years.

- Shipping: emissions from shipping were 1.8 MtCO2e in 2023, 0.2 MtCO2e (8%) lower than in 2021. Emissions are now 56% lower than 1990 levels.

- Shipping emissions have fallen every year since 2019 and are now 23% below 2019 pre-pandemic levels. Most of the absolute emissions reductions are in domestic shipping, particularly coastal domestic shipping, but international shipping emissions have fallen by a proportionally greater amount.

Agriculture and land use

Agriculture

Agriculture is currently the second highest-emitting sector in Scotland. Emissions fell by 0.2 MtCO2e (2%) to 7.5 MtCO2e between 2021 and 2023 and are now 13% lower than in 1990.

- Livestock emissions from enteric fermentation (the digestive process of cattle and sheep) and waste and manure management have declined by 19% since 1990 to 5.2 MtCO2e in 2023. This is due to a decline in cattle and sheep numbers.

- Soil emissions have decreased by 16% since 1990 to 1.6 MtCO2e in 2023. Soil emissions associated with nitrogen fertilisers have fallen by 57% due to increased efficiency in application and the amount used on agricultural land.[19] This decrease is offset by increases in emissions from other soil activities such as liming (an action to improve soil pH). Emissions from agriculture will receive increasing focus as other sectors continue to decarbonise. Agriculture is expected to become the highest-emitting sector in Scotland during the Third Carbon Budget period in Scotland’s Draft Climate Change Plan: 2026-2040 (the draft CCP).[20]

Land use

Emissions from land use have fallen by 5.5 MtCO2e since 1990. Between 1990 and the late 2000s, land use emissions steadily declined, with the sector becoming a small net sink of emissions between 2009 and 2017. In the last two years emissions have risen, due to a smaller forest sink and the removal of trees on peat soils undergoing restoration, and land use is now a net source of emissions, at 0.5 MtCO2e in 2023.

- The shift from source to sink is largely driven by the forestry sector, which is currently a sink of -8.6 MtCO2e. The forestry sink in Scotland has decreased from a peak of around -10 MtCO2e, which was maintained over the late 1990s through to 2013.

- This is the result of lower planting rates since the 1990s (see Chapter 4).

- Grasslands on mineral soils are also a significant sink in Scotland, at -3.6 MtCO2e in 2023. This sink has increased since 1990 by around 1.0 MtCO2e and is attributed to existing, established grasslands sequestering CO2.

- The largest source of land use emissions is peatlands, at 6.1 MtCO2e in 2023. However, this has decreased by 2.3 MtCO2e since 1990, driven by the expansion of peat restoration activity.

- Drainage of peatland and its management as grassland remains a key driver of emissions from peatland in Scotland at 1.9 MtCO2e in 2023, contributing 31% of the total emissions from peat.

- Croplands on mineral soils are also a significant source of emissions at 4.8 MtCO2e in 2023. However, this has fallen by 1.7 MtCO2e since 1990, indicating a decrease in the transition of grasslands to cropland systems, as well as a decrease in soil carbon emissions over time following the initial land use transition.

- Restoring and growing the land use sink will be critical to meeting Scotland’s carbon budgets and especially for reaching Net Zero by 2045. The reduction in the forestry sink in recent years, because of lower planting rates over recent decades, demonstrates the long-term effects of tree planting on land use emissions – planting rates will need to increase quickly over the coming years to deliver the contribution required to Net Zero (see Chapters 4 and 5).

Business and industrial process

Business and industrial process (which covers industry and commercial buildings) is the third highest-emitting sector in Scotland. Emissions were 7.0 MtCO2e in 2023, 0.5 MtCO2e (6%) lower than in 2021. These have fallen substantially over time and are now 49% lower than 1990 levels.

- Industry: emissions from industry were 5.0 MtCO2e in 2023, 0.3 MtCO2e (6%) lower than in 2021.

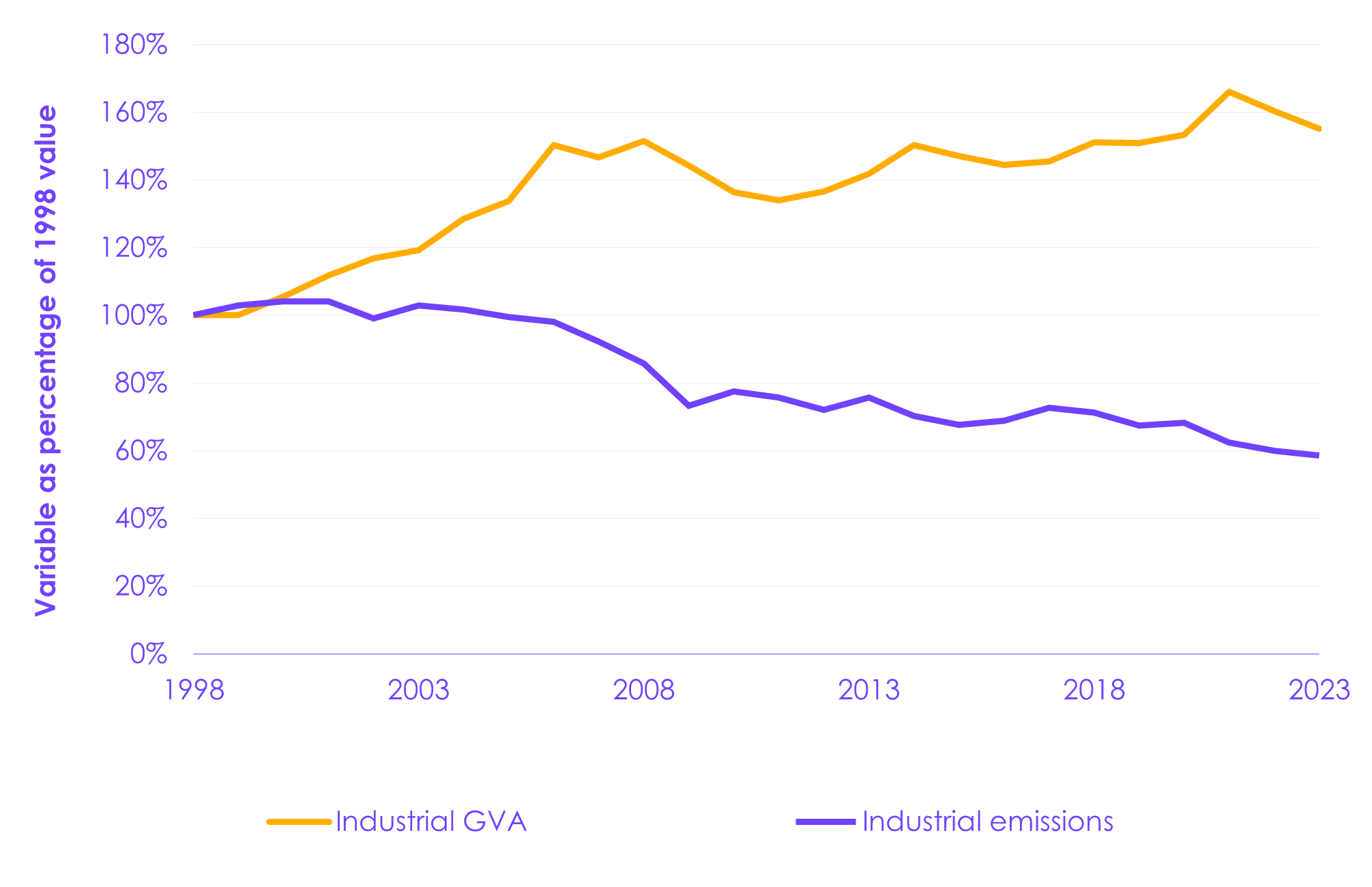

- There has been a structural shift since the 1990s towards less energy-intensive, higher-value industrial output. The gross value added (GVA) of Scottish manufacturing increased by 55% between 1998 and 2023 (Figure 2.4). Over 40% of this growth came from the drinks industry.[21] The emissions intensity (tCO2e/£GVA) of Scottish industry has improved dramatically, falling by more than half since 1998.[22]

- Emissions from industry fell rapidly between 1990 and 1995, mostly driven by the closure of the Ravenscraig steelworks in 1992, but have been falling more slowly since then. Since 2009, industrial emissions have fallen by around 0.1 MtCO2e per year on average.

- By moving to higher value, low carbon production, Scotland’s industries can attract investment and carve out a more competitive footing. Achieving this requires policy to create a viable investment case and a carbon border adjustment mechanism to level the playing field.

- Commercial buildings: emissions from commercial buildings were 1.3 MtCO2e in 2023, 0.1 MtCO2e (4%) lower than in 2021.

- In the longer term, growth in the commercial sector has more than offset decarbonisation actions.[23] Emissions from commercial buildings are now 11% higher than 1990 levels.

| Figure 2.4 Change in emissions and gross value added (GVA) in Scotland’s industry sector since 1998 |

Description: Emissions in the industry sector have declined since 1998, despite an increase in sectoral GVA over the same period. Description: Emissions in the industry sector have declined since 1998, despite an increase in sectoral GVA over the same period.Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; Office for National Statistics (2025) Regional gross value added (balanced) by industry: all ITL regions (April 2025); CCC analysis. Notes: (1) Emissions are shown using the CCC’s industry sector classification (see Annex 1). (3) GVA is calculated in real 2022 prices for the ‘Manufacturing’ sector under Standard Industrial Classifications in chained volume measures. |

Buildings

The buildings sector is currently the fourth highest-emitting sector in Scotland. Emissions have fallen by 1.3 MtCO2e (18%) between 2021 and 2023 to 6.0 MtCO2e, which is 40% below 1990 levels.

- Residential buildings: emissions from residential buildings were 5.0 MtCO2e in 2023, 1.2 MtCO2e (19%) lower than in 2021. Emissions are now 38% lower than 1990 levels.

- Most of the emissions reductions have been delivered since 2009. Policies have helped to improve the efficiency of heating technologies and deliver investments in building fabric efficiency.[24];[25] Prior to the COVID-19 pandemic and recent gas price spike, from 1990 to 2019, emissions in residential buildings in Scotland had fallen by slightly more than across the UK as a whole.

- 2023 was warmer than 2021, reducing energy demand for heating homes. After applying a temperature adjustment to account for this effect, the reduction in emissions from 2021 to 2023 was 0.6 MtCO2e (10%). This suggests that half the fall in emissions was weather-related and half was driven by other factors, likely including behavioural responses to high energy prices.

- Public buildings: emissions from public buildings were 1.0 MtCO2e in 2023, 0.1 MtCO2e (13%) lower than in 2021. Emissions are now 50% lower than 1990 levels.

- Most of the emissions reductions in public buildings occurred between 1990 and 2009. Significant emissions reductions have been made across a range of public bodies including the NHS, Scottish Government core estate, and local authorities.

- Although Scotland’s public bodies have had a duty under the Climate Change (Scotland) Act 2009 to act in the way best calculated to contribute to the delivery of emissions reduction targets while exercising their functions since 2011, emissions in 2023 were only 6% below 2011 levels.[26]

- Residential, public, and commercial buildings are expected to be central to delivering emissions reductions throughout the 2030s. This means that falling behind on buildings decarbonisation would have severe implications for longer-term decarbonisation.

Energy supply

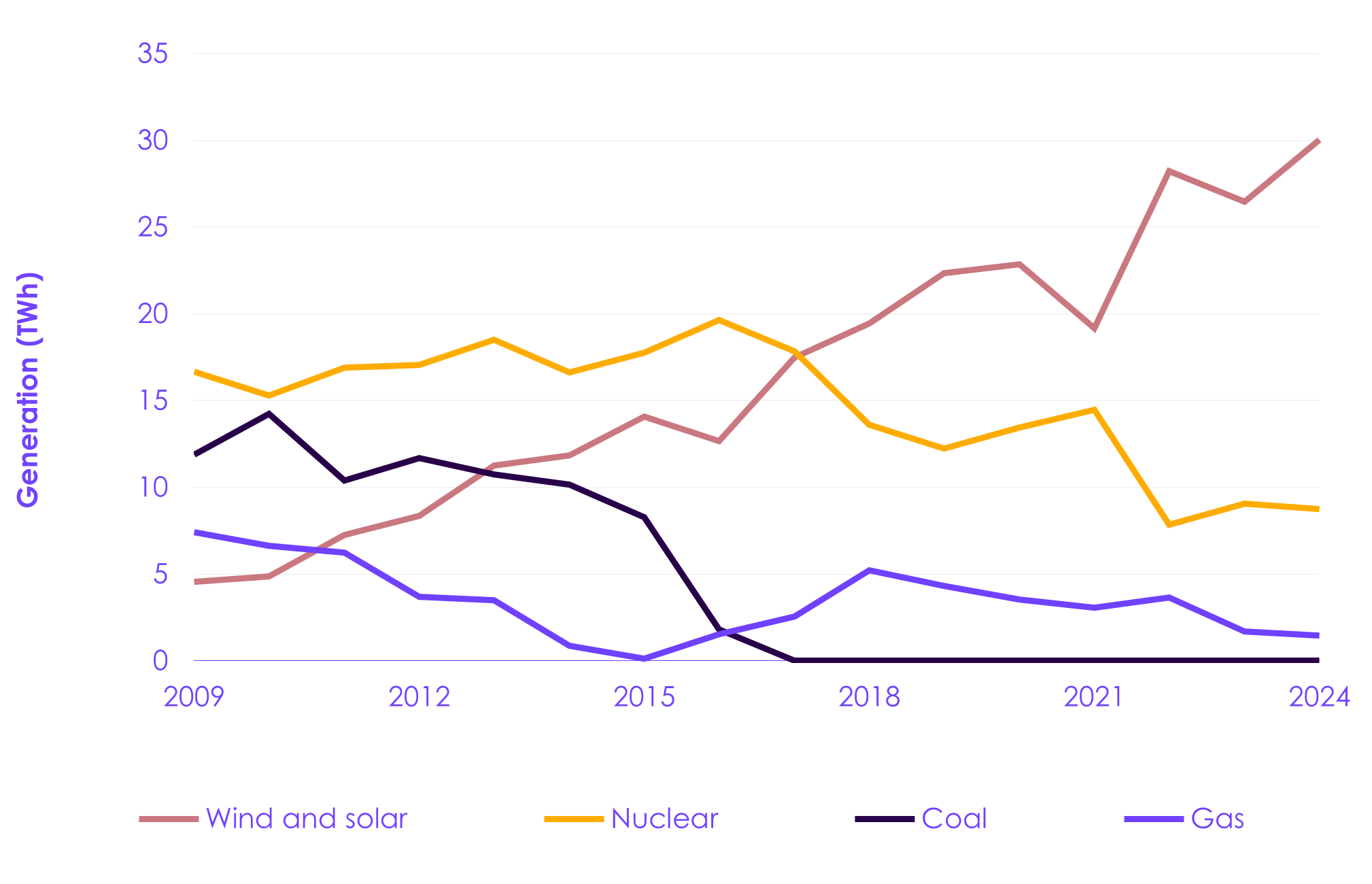

The energy supply sector has been the key driver of Scotland’s emissions reductions. It was Scotland’s highest-emitting sector until 2013 but has since dropped to fifth. Emissions have fallen by 0.9 MtCO2e (19%) between 2021 and 2023 to 3.9 MtCO2e, 82% lower than in 1990.

- Electricity supply (excluding energy from waste): electricity generation in Scotland is almost completely decarbonised. Electricity supply emissions were 0.7 MtCO2e in 2023, 0.6 MtCO2e lower than in 2021. Emissions are now 95% lower than 1990 levels.

- Emissions fell rapidly between 2010 and 2017 as coal was phased out of the generation mix and largely replaced with wind and solar (Figure 2.5). The last remaining coal-fired power station in Scotland, Longannet, closed in 2016, leaving unabated gas generation, which also declined significantly in this period, as the main source of emissions.

- Between 2017 and 2023, emissions reduced at a slower rate as continued deployment of wind and solar largely displaced retiring nuclear capacity. During this period, the share of generation from unabated gas remained around 10% up to 2022, until a fall to 7% in 2023. Remaining emissions are dominated by Peterhead power station, which in 2023 accounted for more than 90% of electricity supply emissions.

- Demand for electricity in Scotland has been falling by an average of 2% per year since 2005, but this is expected to grow again as a result of the roll-out of low-carbon electric technologies.

- For the GB-wide electricity market, the continued roll-out of renewable generation capacity should continue to displace fossil generation, leading to further reductions in electricity supply emissions.

- Fuel supply: emissions from fuel supply were 2.9 MtCO2e in 2023, 0.3 MtCO2e (10%) lower than in 2021. Emissions are now 56% lower than 1990 levels.

- Oil refineries: oil refining contributed 40% of fuel supply emissions, emitting 1.2 MtCO2e in 2023. These emissions have fallen by 59% since 1990, as output from Grangemouth, Scotland’s main oil refinery, has reduced.

- The Grangemouth oil refinery, part of the wider industrial complex, ranked as Scotland’s largest point source of emissions. In November 2023, the owner, Petroineos, announced that it would close the refinery, and the company completed the closure in 2025. Reported fuel supply emissions are therefore expected to fall substantially because of the closure.

- Oil and gas processing terminals: emissions from oil and gas processing terminals together contributed around 33% of fuel supply emissions, emitting 1.0 MtCO2e in 2023. These emissions have fallen by 35% since 1990.

- Gas distribution: gas distribution contributed around 14% of fuel supply emissions (0.4 MtCO2e) in 2023. These emissions have fallen by 59% since 1990.

- Energy from waste (EfW): emissions from EfW increased rapidly between 2013 and 2019. Since 2019, EfW emissions have been reported at around 0.3 MtCO2e, although emissions in 2022 and 2023 are underestimated as one EfW site was missed from the emissions data. Between 2019 and 2023, the amount of household waste incinerated in Scotland increased by 64%.[27]

- In 2024, Scotland had eight operating EfW sites with a total permit capacity of 1.4 Mt of waste per year. No new energy from waste sites have been granted planning permissions since 2023, when new restrictions were introduced. However, four additional sites are in the commissioning or construction phase, which, if fully delivered, would provide an additional 0.9 Mt of permitted capacity per year, significantly increasing Scotland’s EfW capacity and emissions.[28]

| Figure 2.5 Electricity generation from wind and solar, coal, gas, and nuclear (2009–2024) |

Description: Coal was phased out of the electricity generation mix in Scotland by 2017, while wind and solar have been providing a growing share of the generation mix. Description: Coal was phased out of the electricity generation mix in Scotland by 2017, while wind and solar have been providing a growing share of the generation mix.Source: Department for Energy Security and Net Zero (2025) Electricity generation and supply in Scotland, Wales, Northern Ireland and England, 2019 to 2024; CCC analysis. Notes: Generation for coal, gas, and nuclear refers to generation by ‘Major Power Producers’, which excludes autogeneration where electricity is produced as part of industrial or commercial activities as a by-product. |

Waste management

Emissions from waste management, excluding energy from waste, fell by 0.02 MtCO2e (1%) between 2021 and 2023 to 1.7 MtCO2e. Emissions are now 73% lower than 1990 levels, but have not changed significantly since 2013.

- The main cause of the fall in emissions since 1990 has been a decrease in waste sent to landfill, driven by the Landfill Tax, which helped drive a reduction in waste generated and an increase in recycling rates.

- Waste emissions have fallen by only 0.1 MtCO2e since 2013. Emissions reductions from reducing waste sent to landfill have slowed, while recycling rates have plateaued.

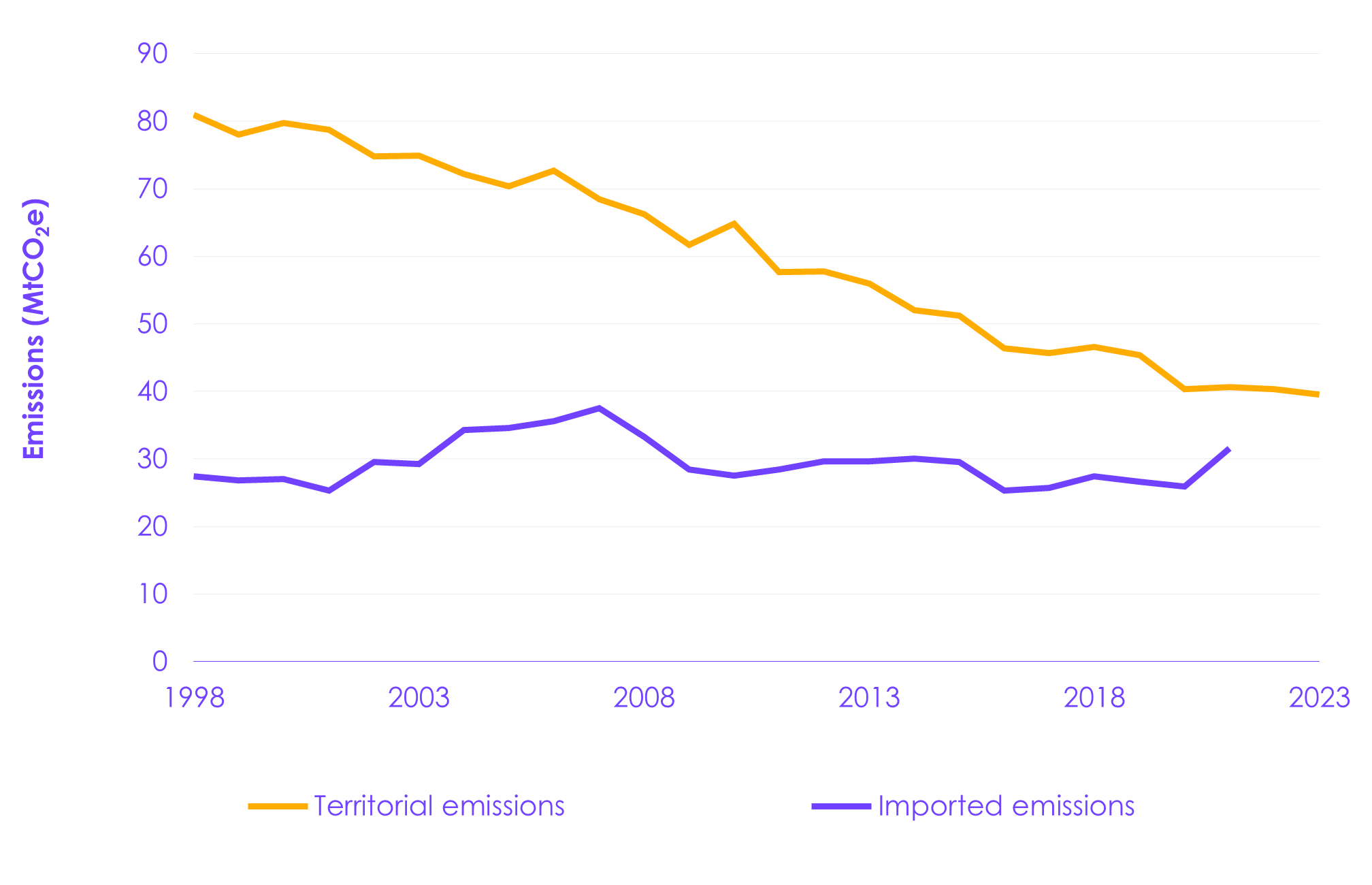

2.2 Emissions from imports

Scotland’s legally binding targets are set on the basis of territorial emissions (that is, emissions within Scotland’s territorial borders). However, it is important to also consider emissions associated with Scottish imports. The latest published imported emissions data are for 2021.

Emissions from imports have been relatively steady since 2009, even as territorial emissions have fallen considerably over the same period (Figure 2.6).

- Between 1998 (the first year of available data) and 2021, imported emissions increased by 15% from 27.4 MtCO2e to 31.6 MtCO2e. Imported emissions peaked in 2007 before falling sharply in 2008 following the global financial crisis.

- Year-on-year, imported emissions decreased by 3% in 2020 and increased by 22% in 2021. This increase is due to greater imports from non-EU countries following the end of the Brexit transition period in 2021, as indicated by Office for Budget Responsibility trade analysis.[29] However, the imported emissions data are highly variable, and subject to revisions.

- In the equivalent publication for the UK, a similar 2021 peak was subsequently revised down to below 2019 levels, but imported emissions increased further in 2022. This downward revision was due to methodological changes in the statistics from the University of Leeds.[30]

Minimising potential future carbon leakage, through addressing emissions from imports and ensuring the competitiveness of Scottish industry, would prevent reductions in Scotland’s territorial emissions from being undermined by slower progress elsewhere.

- In our UK-wide Seventh Carbon Budget advice (2025), we highlighted that the risk of carbon leakage, though limited, remains, particularly in energy-intensive sectors and in agriculture.

- The report also set out a hierarchy of available policy levers and proposed that the UK Government set a non-legally binding benchmark against which to track imported emissions.

| Figure 2.6 Comparison of imported and territorial emissions |

Description: Scottish territorial emissions have fallen since 1990 while emissions from imports outside the UK have been relatively steady since 2009, following a drop after the financial crisis. Description: Scottish territorial emissions have fallen since 1990 while emissions from imports outside the UK have been relatively steady since 2009, following a drop after the financial crisis.Source: National Atmospheric Emissions Inventory (2025) Greenhouse Gas Inventories for England, Scotland, Wales and Northern Ireland: 1990-2023; Scottish Government (2025) Scotland’s Carbon Footprint 1998-2021; CCC analysis. Notes: Imported emissions refer to emissions associated with imports from outside the UK. The latest available data point is 2021 due to the lag in producing the statistics. The next release is expected in the first half of 2026. |

Chapter 3: The draft Climate Change Plan

In November 2025, the Scottish Government published Scotland’s Draft Climate Change Plan: 2026-2040 (the draft CCP). This sets out an emissions reduction pathway to meet the first three carbon budgets, including emissions savings from specific policies and proposals.[31] In this chapter, we consider the overall approach taken in the draft CCP and discuss this pathway. Our assessment of the policies and plans required to deliver it can be found in Chapter 5.

Our key messages are:

- We welcome the quantification of abatement associated with specified policy outcomes. This makes clear what needs to be delivered to meet Scotland’s carbon budgets.

- Urgent work is now needed to develop delivery plans and implement policies to achieve these outcomes.

- It is positive to see the planned approach to monitoring and evaluation (M&E), which includes just transition indicators for the first time. The final CCP should include a finalised M&E framework, including annual pathways for sectoral emissions and key indicators of progress.

- The pathway set out in the draft CCP sees emissions fall across all sectors.

- To deliver the pathway, emissions reductions will need to broaden, particularly into the transport; residential and public buildings (buildings); agriculture; and land use, land use change and forestry (land use) sectors. The Scottish Government has substantial powers to reduce emissions in these areas.

- In the First Carbon Budget, mostly devolved sectors provide 48% of the required emissions reductions. This increases to 62% for the Second and Third Carbon Budgets.

- Some of the choices in the draft CCP pathway could increase delivery risk. The final CCP should consider appropriate contingencies or methodological changes to address this.

- The modelling methodologies and assumptions used for some aspects of the buildings and land use pathways rely on emissions savings that depend on highly uncertain wider factors.

- In some key areas, including low-carbon heating, policies are either missing or carry significant risks. We discuss these concerns in Chapter 5.

- The draft CCP pathway has significant dependence on negative emissions technologies (NETs), an area with significant risk and with policy powers largely reserved to the UK Government.

3.1 Overall approach taken in the draft Climate Change Plan

In our 2025 Scotland’s Carbon Budgets advice, we set out key considerations for the draft CCP to address, including:

- Quantification of emissions reductions. Publishing details on the assumptions underpinning the pathway and how the abatement will be achieved by planned policies.

- Roles and responsibilities. Setting out clear roles, responsibilities, and accountability mechanisms for delivering aspects of emissions reduction and climate change adaptation, as well as details of how these will be coordinated.

- Monitoring and evaluation. Developing a monitoring and evaluation plan, including the latest emissions data and underlying indicators of progress, that can be used to identify where there are risks of delivery falling behind the pace of change that is required.

- Contingency planning. A range of credible contingency plans that can be activated if necessary.

In April 2025, the Convenor of the Scottish Parliament’s Net Zero, Energy and Transport Committee wrote to the Acting Cabinet Secretary for Net Zero and Energy to summarise input gathered by his Committee on what would make a good Climate Change Plan.[32] We provided input into this process, as did Audit Scotland, Environmental Standards Scotland, and the Scottish Fiscal Commission. The Convenor’s letter identifies a range of themes that should be addressed within an effective plan. We welcome the Scottish Government’s approach to the draft CCP, which aims to address these considerations.

3.1.1 Quantification of emissions reductions

This is the first comprehensive plan from the Scottish Government that quantifies the policies and proposals that will be needed to achieve Scotland’s emissions reduction targets. This makes clear how the Scottish Government plans to deliver the carbon budgets, as well as the outcomes it will need to achieve to do this. The Scottish Government should now develop detailed delivery plans and implement the required policies to ensure that these outcomes can be achieved. This work needs to be progressed with urgency.

- In a number of areas, the policies that will be needed to achieve these outcomes are not yet in place or carry significant risks. This is particularly the case in the buildings, agriculture, business and industrial processes, and NETs sectors. Our full assessment of policies and plans is set out in Chapter 5.

- We also have concerns about the modelling approach taken to quantify aspects of the emissions reduction pathways for buildings and land use. These are discussed in Section 3.2.

3.1.2 Roles and responsibilities

The draft CCP includes both quantified emissions savings by sector and detailed sectoral annexes setting out the changes that will be needed to achieve these. The annexes include a vision for each sector, which should help clarify the role that each sector will play.

In many cases, the details in the draft CCP (including route map diagrams) set out who will be responsible for delivering key aspects of this vision. However, there is little detail on the actual governance processes to deliver the vision or on the role of local authorities and other bodies.

The Scottish Government should expand on these sectoral visions and implement delivery plans which give clear roles and responsibilities to different levels of government and wider organisations to enable reliable delivery.

3.1.3 Monitoring and evaluation

The draft CCP sets out the Scottish Government’s proposed approach to monitoring emissions reductions, including the use of the latest emissions data and underlying indicators of progress. We welcome the intention to track emissions progress at subsector level and to develop a set of early-warning indicators to allow earlier identification of areas of progress or risk.